Maternity Leave in Ireland 2026: 26 Weeks Paid + €299/Week

Maternity leave in Ireland in 2026 is 26 weeks of paid leave plus 16 weeks of unpaid additional leave (42 weeks total), with State-paid Maternity Benefit at €299/week for those who meet PRSI conditions. This guide covers the full entitlement, Form MB1 application, employer obligations under the Maternity Protection Acts, taxation, premature birth and stillbirth rules, the 2024 Act postponement option, and how Maternity Leave interacts with Paternity, Parent’s, and Parental Leave.

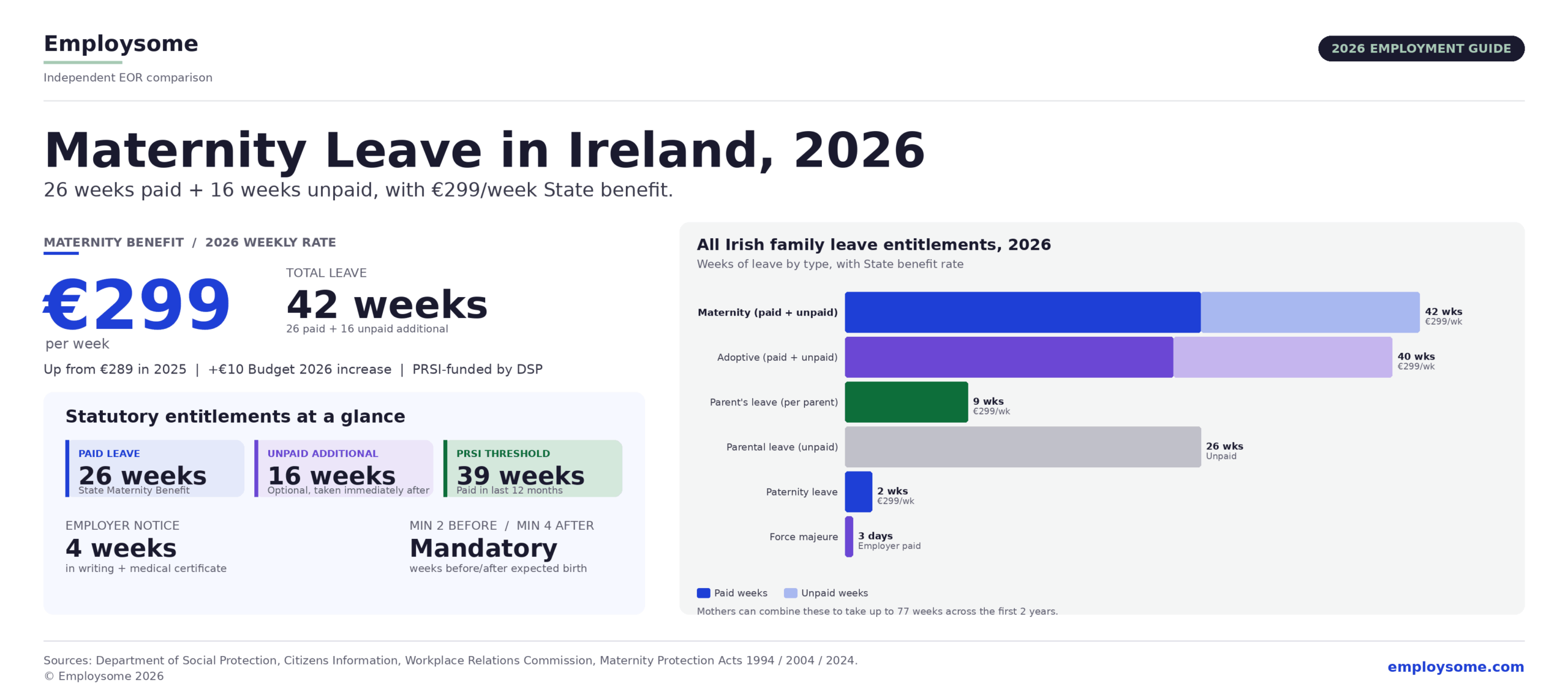

Maternity leave in Ireland in 2026 entitles eligible employees to 26 weeks of paid maternity leave plus 16 weeks of additional unpaid maternity leave, totalling up to 42 weeks of protected time off. The paid portion is funded by the State through Maternity Benefit at a flat rate of €299 per week in 2026 (up from €289 in 2025), paid by the Department of Social Protection (DSP) provided the employee has sufficient Pay Related Social Insurance (PRSI) contributions. Employers are not legally required to top up pay during maternity leave, although many do under company policy or collective agreement.

Maternity leave applies to all pregnant employees regardless of tenure or hours: full-time, part-time, casual, and fixed-term staff are all covered. At least 2 weeks must be taken before the expected birth date, and at least 4 weeks after the birth. Since 3 July 2023, the same rights also apply to transgender men who are pregnant or have given birth and hold a gender recognition certificate. The 2024 Maternity Protection Act introduced the option to postpone maternity leave for serious illness from 20 November 2024, and Budget 2026 increased the Maternity Benefit weekly rate by €10 to €299.

This 2026 guide to maternity leave in Ireland covers the full 42-week entitlement, the Maternity Benefit weekly rate and PRSI contribution requirements, how the leave is scheduled and notified, employer obligations under the Maternity Protection Acts 1994 and 2004, taxation of Maternity Benefit, what happens for premature births and stillbirths, postponement rules for serious illness or infant hospitalisation, the right to return to the same role, antenatal and postnatal medical leave, breastfeeding breaks, and what international employers hiring through an Irish Employer of Record (EOR) need to know.

Maternity Leave in Ireland 2026: The 42-Week Entitlement

Irish maternity leave is governed primarily by the Maternity Protection Act 1994, the Maternity Protection (Amendment) Act 2004, and most recently the Maternity Protection, Employment Equality and Preservation of Certain Records Act 2024. The 2024 Act introduced the right to postpone maternity leave for serious illness, effective from 20 November 2024.

| Entitlement (2026) | Detail |

| Basic maternity leave | 26 weeks of paid statutory leave (156 days) |

| Additional maternity leave | Up to 16 weeks of unpaid leave, taken immediately after basic leave |

| Total potential leave | 42 weeks (26 weeks paid + 16 weeks unpaid) |

| Minimum period before birth | 2 weeks before expected due date |

| Minimum period after birth | 4 weeks after birth |

| Maternity Benefit weekly rate (2026) | €299 per week (up from €289 in 2025) |

| Notice required to employer | At least 4 weeks before maternity leave starts (in writing) |

| Notice for additional 16 weeks | At least 4 weeks before basic leave ends |

| Notice to return to work | At least 4 weeks before return date |

| Coverage | All pregnant employees regardless of tenure, role, or hours |

Why Irish maternity leave is structured this way: The 26-week paid period is designed as the core State-funded protection, intended to cover the immediate post-birth recovery and bonding period. The additional 16 weeks unpaid period gives parents flexibility to extend leave when financially feasible, while the State retains social insurance credits during the unpaid weeks (so employees do not lose pension or other entitlements). The 2-weeks-before / 4-weeks-after split reflects medical guidance on pre-birth rest and post-birth recovery.

Continued accrual during leave: While on maternity leave (both paid and unpaid additional leave), employees are treated as if still at work for the purposes of accruing annual leave and public holiday entitlement. Public holidays falling during maternity leave are credited and added on after the leave period. Length of service continues to accrue, meaning maternity leave does not affect redundancy, pension, or seniority calculations.

💡 Employsome Insight: Employer Top-Ups Are the Real Competitive Lever in Ireland

Many Irish employers (particularly multinationals and large domestic firms) top up Maternity Benefit to full salary for some or all of the 26 weeks under company policy or collective agreement. This is a meaningful retention lever: the gap between full salary and the €299 weekly Maternity Benefit can reach €3,000+ per month for higher earners (see our average salary in Ireland guide for benchmark wage data), so a top-up policy materially improves the offer for senior female hires. International employers benchmarking against the statutory minimum risk losing competitive Irish talent to companies that offer 6 to 26 weeks of full-pay top-up.

Maternity Benefit: 2026 Rate and PRSI Requirements

Maternity Benefit (Sochúntaíocht Mháthartha) is a weekly payment from the Department of Social Protection (DSP) to women on maternity leave. The 2026 weekly rate is €299 (up from €289 in 2025), payable for the full 26 weeks of basic maternity leave provided the employee meets the PRSI contribution conditions.

2026 PRSI contribution requirements: To qualify for Maternity Benefit, an employee must have one of the following:

- At least 39 weeks of PRSI contributions paid in the 12 months immediately before the first day of maternity leave; or

- At least 39 weeks of PRSI contributions paid since starting work, and at least 39 weeks paid or credited in the relevant tax year (the second-last tax year before maternity leave) or the tax year immediately following; or

- At least 26 weeks of PRSI contributions paid in the relevant tax year and at least 26 weeks paid in the tax year immediately before the relevant tax year

For self-employed women, 52 weeks of PRSI contributions paid at Class S in the tax year after the relevant tax year are required. The relevant tax year is the second-last tax year before maternity leave: for a 2026 maternity leave, the relevant tax year is 2024.

How to apply: The application is made directly to the Department of Social Protection using Form MB1, submitted at least 6 weeks before maternity leave starts (12 weeks for self-employed applicants). The form requires a section completed by the doctor confirming the expected due date, and a section completed by the employer confirming employment status and the proposed leave start date. Employees can elect for Maternity Benefit to be paid directly to the employer (where the employer is topping up to full salary) or directly to themselves (where there is no employer top-up).

Half-rate Maternity Benefit: If the employee is already in receipt of certain other social welfare payments (such as One-Parent Family Payment, Carer’s Benefit, Widow’s Pension, or Disability Allowance), they may receive Maternity Benefit at half the standard rate. Employees in this position should seek advice from Citizens Information or a welfare rights officer before applying.

How Maternity Leave Is Scheduled and Notified

Maternity leave is structured around the expected date of confinement (EDC): the medically certified due date. The Maternity Protection Acts require minimum periods both before and after the birth, with flexibility on the remaining weeks.

| Schedule Rule | Detail |

| Earliest start date | 16 weeks before the expected birth (with extra weeks added for premature birth) |

| Latest start date | Monday before the week the baby is due (to ensure 2 weeks pre-birth) |

| Mandatory pre-birth period | Minimum 2 weeks before due date |

| Mandatory post-birth period | Minimum 4 weeks after the birth |

| Total basic leave | 26 weeks (156 days) of paid leave |

| Additional leave option | Up to 16 further weeks unpaid, immediately after the 26 weeks |

| Notice for basic leave | 4 weeks before leave starts, in writing, with medical certificate |

| Notice for additional leave | 4 weeks before basic leave ends, in writing |

| Notice for return to work | 4 weeks before intended return date |

Worked example: If an employee’s due date is Wednesday, 14 January 2026, the latest date she can start maternity leave is Monday, 5 January 2026. She must give written notice no later than 8 December 2025 (4 weeks before). Her 26 weeks of basic leave run to Sunday, 5 July 2026. If she opts for the additional 16 weeks, the unpaid period runs to 25 October 2026, after which she must return to work. Notice of intention to take additional leave must be given by 7 June 2026 (4 weeks before basic leave ends), and notice of return to work by 27 September 2026 (4 weeks before return).

What happens if the baby is born early: If the baby is born before the maternity leave was scheduled to start, the 26 weeks of paid leave begin from the actual date of birth, plus an extra period equal to the gap between the actual birth and the expected leave start date. This effectively means a premature birth never reduces total leave. The employee must notify her employer in writing within 14 days of the birth.

How Maternity Leave Interacts with Paternity, Parent’s, and Adoptive Leave

Maternity leave intersects with several other Irish leave entitlements parents should understand. The combined picture for a new family in 2026 is:

| Leave Type (2026) | Duration | State Benefit Rate | Eligibility |

| Maternity Leave | 26 weeks paid + 16 weeks unpaid | €299/week (paid 26 weeks) | All pregnant employees; PRSI for benefit |

| Paternity Leave | 2 weeks | €299/week | Father / partner of new parent; first 6 months |

| Parent’s Leave | 9 weeks per parent | €299/week | Each parent in first 2 years; non-transferable |

| Parental Leave (unpaid) | Up to 26 weeks per parent per child | None (unpaid) | Each parent until child is 12 |

| Adoptive Leave | 24 weeks paid + 16 weeks unpaid | €299/week (paid 24 weeks) | Adoptive parent, primary carer |

| Force Majeure Leave | Up to 3 days per year (5 in 36 mo) | Paid by employer | Urgent family illness or injury |

| Antenatal / Postnatal Medical Leave | As required (paid) | Paid by employer | Pregnancy-related medical visits |

Combining leave types: A new mother in Ireland can realistically string together a long period away from work by combining: 26 weeks paid maternity leave + 16 weeks unpaid additional maternity leave + 9 weeks Parent’s Leave + up to 26 weeks unpaid Parental Leave = up to 77 weeks (nearly 18 months) of protected leave during the first two years of the child’s life. Father / partner can independently take 2 weeks Paternity Leave + 9 weeks Parent’s Leave = 11 weeks paid State-funded leave, plus their own 26 weeks unpaid Parental Leave.

Employer Q&A on overlap: Maternity, paternity, and parent’s leave run as separate entitlements and can’t be denied because another type was used. Employers may, however, require reasonable notice and documentation for each. Most large Irish employers maintain HR systems that automate tracking of cumulative leave taken across all categories.

Special Situations: Premature Birth, Stillbirth, Hospitalisation, Serious Illness

Several specific scenarios trigger modified rules under the Maternity Protection Acts. Foreign employers managing Irish staff should be familiar with all of them to avoid compliance gaps.

Premature birth (born before maternity leave starts): Maternity leave begins on the actual date of birth and lasts 26 weeks, plus an extra period equal to the gap between the actual birth date and the expected leave start date. The employee must notify her employer in writing within 14 days of the birth.

Stillbirth or miscarriage: Since 16 September 2024, the definition of stillbirth in Ireland is a baby born at or after 23 weeks gestation, or weighing 400 grams or more, with no signs of life. Under Irish law, an employee who experiences a stillbirth (so-defined) is entitled to full 26 weeks paid maternity leave plus 16 weeks unpaid additional leave, identical to a live birth. The Maternity Benefit application requires a letter from the doctor in addition to Form MB1.

Hospitalisation of the baby: If the baby is admitted to hospital after birth, the mother can opt to postpone maternity leave (or additional leave) for up to 6 months, subject to her employer’s agreement and provided at least 14 weeks of leave have already been taken (4 weeks of which were post-birth). Postponed leave resumes when the baby returns home from hospital.

Serious illness of the mother (postponement): From 20 November 2024, the Maternity Protection Act 2024 introduced a new right to postpone maternity leave for ongoing treatment of a serious health condition. This addresses cases where the mother needs cancer treatment or other intensive medical care and prefers to use maternity leave fully when treatment allows. The maximum postponement period is also up to 52 weeks for serious illness, subject to medical evidence and employer agreement.

Death of the mother during childbirth: If the mother dies during or shortly after childbirth, her remaining maternity leave entitlement transfers to the father. The father must start this leave within 7 days of the mother’s death and can take the remaining unused portion of basic and additional leave.

Becoming sick during maternity leave: If an employee becomes ill during basic maternity leave, the leave continues as maternity leave unless she elects otherwise. If she becomes ill during additional (unpaid) maternity leave, she may end the additional leave and switch to certified sick leave instead, provided the conditions of the company’s sick leave scheme are met.

Multiple births: Irish law treats twins, triplets, or higher-order multiples the same as a single birth for maternity leave purposes: still 26 weeks paid + 16 weeks unpaid total. There is no additional leave for multiples, although Parent’s Leave (9 weeks per parent) accrues per parent, not per child.

Taxation of Maternity Benefit in Ireland

Maternity Benefit is taxable income in Ireland but is NOT subject to Universal Social Charge (USC) or PRSI. Revenue collects the income tax due on Maternity Benefit by reducing the employee’s annual tax credits and standard rate band on the Revenue Payroll Notification (RPN) sent to the employer.

How the tax is collected: Once the DSP starts paying Maternity Benefit, it informs Revenue, which adjusts the employee’s tax credits and rate band on a Week 1 basis. If the employer is paying full salary with the Maternity Benefit assigned to the employer (a “top-up arrangement”), the employer sees only the difference between full salary and the €299/week benefit on the payroll, and applies tax credits against that difference. If the Maternity Benefit is paid directly to the employee (no top-up), the employer pays nothing during the leave but Revenue still adjusts the RPN to collect tax due on the benefit.

Worked example, full top-up: An employee earns €700 per week (well above Ireland’s statutory minimum wage). Her employer tops up Maternity Benefit to full salary, with the €299 benefit assigned directly to the employer. On her payroll, the employer pays €401 per week (the difference between €700 full salary and €299 Maternity Benefit). Income tax, USC, and PRSI are calculated on the €401 employer-paid portion in the usual way; income tax (only) on the €299 benefit is collected via reduced tax credits and rate band on the revised RPN.

Worked example, no top-up: An employee earns €700 per week. Her employer does not pay her wages while on maternity leave. She receives the €299 Maternity Benefit directly from the DSP. Revenue reduces her annual tax credits and rate band to account for the benefit, and the income tax is collected when she returns to work in the second half of the year. No USC or PRSI is charged on the €299 benefit.

Tax years spanning maternity leave: When maternity leave spans two tax years (for example, November to April), Maternity Benefit received in the second tax year is taxed by reducing the employee’s tax credits and rate band on a cumulative basis from 1 January. If the employee’s own tax credits are insufficient, the balance can be collected by reducing her spouse’s tax credits and rate band where they are jointly assessed.

Employer Obligations During Maternity Leave

Beyond the leave entitlement itself, Irish employers carry several specific legal duties under the Maternity Protection Acts and related employment legislation:

- Pregnancy risk assessment: Once an employee informs her employer of her pregnancy, the employer must conduct a pregnancy-specific health and safety risk assessment. If risks cannot be removed, the employer must provide suitable alternative work or place the employee on health and safety leave (first 3 weeks paid by employer, thereafter Health and Safety Benefit from DSP).

- Right to attend antenatal appointments: Employees are entitled to paid time off to attend medical appointments related to pregnancy, for as long as needed including travel time. Two weeks’ notice is required for non-urgent appointments. The right extends to postnatal medical visits for up to 14 weeks after the birth.

- Right to attend antenatal classes: Employees are entitled to paid time off to attend one set of antenatal classes per pregnancy (excluding the last 3 classes of the set, which the employee attends in her own time). Fathers can also take paid time off to attend the last 2 classes in the set.

- Breastfeeding breaks: For 26 weeks after the birth, employees who are breastfeeding are entitled to 1 hour per day of paid breaks while at work (taken as one continuous hour or split into shorter periods). Where suitable workplace facilities are not available, the employer may instead reduce the employee’s working hours by 1 hour per day without loss of pay.

- Right to return to the same job: An employee returning from maternity leave is legally entitled to return to the same job, with the same terms. Where the same job is not “reasonably practicable” (for example, genuine restructuring), the employer must offer suitable alternative work on no less favourable terms.

- Pay rises and improvements during leave: If pay rises or improved working conditions are introduced during maternity leave, the returning employee is entitled to those improvements on her return. Maternity leave cannot be used to disadvantage an employee’s career.

- Protection from dismissal: Dismissal during pregnancy or maternity leave is automatically unfair under the Unfair Dismissals Act, with no minimum service requirement. Penalties for unfair dismissal in this context can reach up to 2 years’ remuneration plus reinstatement.

- Continuation of contractual benefits: Health insurance, pension contributions, share schemes, and other contractual benefits should generally continue during maternity leave unless the employment contract clearly states otherwise. Most multinational employers maintain full benefits during the entire 42-week period.

What Foreign Employers Need to Know

Maternity leave in Ireland is 26 weeks paid + 16 weeks unpaid (42 weeks total)

All pregnant employees are entitled to 26 weeks paid maternity leave plus an optional 16 weeks of additional unpaid leave taken immediately after, totalling 42 weeks. At least 2 weeks must be taken before the expected birth and at least 4 weeks after. There is no minimum service requirement.

Maternity Benefit is €299 per week in 2026

The 2026 Maternity Benefit weekly rate is €299 (up from €289 in 2025), paid by the Department of Social Protection for the 26 weeks of basic maternity leave provided the employee meets PRSI contribution conditions (typically 39 weeks paid in the 12 months before maternity leave). Maternity Benefit does not cover the additional 16 weeks of unpaid leave.

Many Irish employers top up to full salary as a retention lever

Although employers are not legally required to pay during maternity leave, multinationals and many large domestic employers top up Maternity Benefit to full salary for some or all of the 26 weeks. This is a meaningful competitive advantage in attracting senior female talent, particularly in tech, finance, and professional services.

Application is made via Form MB1 at least 6 weeks before leave starts

Employees apply for Maternity Benefit directly to the Department of Social Protection using Form MB1, completed at least 6 weeks before maternity leave starts (12 weeks for self-employed). The form requires a doctor’s certificate confirming the due date and an employer section confirming employment. Employees can elect for the benefit to be paid directly to themselves or to the employer (where a top-up arrangement applies).

Maternity Benefit is taxable but not subject to USC or PRSI

Maternity Benefit is subject to income tax, collected by Revenue reducing the employee’s annual tax credits and standard rate band on the Revenue Payroll Notification. Maternity Benefit is exempt from Universal Social Charge (USC) and PRSI. When maternity leave spans two tax years, the second-year tax is collected on a cumulative basis from 1 January.

The 2024 Act introduced postponement for serious illness

From 20 November 2024, employees can postpone maternity leave for up to 52 weeks if they need ongoing treatment for a serious health condition (such as cancer). This new right was introduced by the Maternity Protection, Employment Equality and Preservation of Certain Records Act 2024 and addresses cases where the mother prefers to defer leave to use it more effectively after treatment.

Trans men with gender recognition certificates are covered

Since 3 July 2023, transgender men who are pregnant or have given birth and hold a gender recognition certificate under the Gender Recognition Act 2015 are entitled to the same maternity leave rights as cis women. This was introduced by the Work Life Balance and Miscellaneous Provisions Act 2023.

Consider an EOR for compliant Irish hiring

For international companies without an Irish entity, an Employer of Record (EOR) manages all maternity leave administration: PRSI registration, RPN updates with Revenue, Maternity Benefit applications via Form MB1, payroll calculations during top-up arrangements, statutory leave tracking, return-to-work compliance, and the auto-enrolment pension scheme (MyFutureFund) launched 1 January 2026. See our Best EOR in Ireland guide for verified provider rankings.

Hiring in Ireland?

Irish employment requires Revenue and PRSI registration, monthly Pay Related Social Insurance (PRSI) remittance, statutory maternity leave administration under the Maternity Protection Acts 1994 and 2004, the 2026 Maternity Benefit application via Form MB1, and the new auto-enrolment pension scheme (MyFutureFund) effective 1 January 2026. Compare the top Employer of Record providers for Ireland in 2026 – verified pricing, compliance scores, and expert rankings from Employsome’s independent research team.

Frequently Asked Questions

In Ireland, employees are entitled to 26 weeks of paid maternity leave plus an additional 16 weeks of unpaid maternity leave, totalling up to 42 weeks. The paid portion is funded by the State through Maternity Benefit at €299/week in 2026. At least 2 weeks must be taken before the expected birth and at least 4 weeks after. There is no minimum service requirement, so all pregnant employees qualify regardless of tenure, hours, or contract type.

Maternity Benefit in Ireland is €299 per week in 2026, paid by the Department of Social Protection for the 26 weeks of basic maternity leave (a €10/week increase from the 2025 rate of €289). The benefit is paid only if the employee meets PRSI contribution conditions (typically 39 weeks paid in the 12 months before maternity leave). Many Irish employers top up Maternity Benefit to full salary under company policy or collective agreement, although this is not legally required. Maternity Benefit does not cover the additional 16 weeks of unpaid leave.

No, employers are not legally required to pay during maternity leave. Maternity Benefit is paid by the State (Department of Social Protection) at €299/week in 2026, provided the employee qualifies on PRSI contributions. However, many Irish employers (particularly multinationals and large domestic firms in tech, finance, and pharma) top up Maternity Benefit to full salary for 6 to 26 weeks under company policy or collective agreement. Employees should check their employment contract or staff handbook to see whether a top-up applies.

Apply directly to the Department of Social Protection using Form MB1, submitted at least 6 weeks before maternity leave starts (12 weeks for self-employed applicants). The form requires a doctor’s certificate confirming the expected due date and an employer section confirming your employment status and proposed leave start date. You can elect for Maternity Benefit to be paid directly to you or directly to your employer (where a salary top-up arrangement applies). Applications can be made online or by post.

To qualify for Maternity Benefit, an employee must have one of: (1) at least 39 weeks of PRSI contributions paid in the 12 months immediately before maternity leave starts; (2) at least 39 weeks paid since starting work and 39 weeks paid or credited in the relevant tax year (the second-last tax year before maternity leave); or (3) at least 26 weeks paid in the relevant tax year and 26 weeks paid in the year before. For self-employed women, 52 weeks of Class S PRSI contributions are required in the tax year after the relevant tax year.

You must give your employer at least 4 weeks’ written notice before maternity leave starts, including a medical certificate confirming your expected due date. If you wish to take the additional 16 weeks of unpaid maternity leave, you must give a further 4 weeks’ written notice before your basic 26-week leave ends. Notice of return to work must also be given at least 4 weeks before your intended return date. Employers may waive notice requirements but cannot extend them.

Yes, Maternity Benefit is subject to income tax in Ireland. However, it is NOT subject to Universal Social Charge (USC) or PRSI. Revenue collects the income tax due on Maternity Benefit by reducing the employee’s annual tax credits and standard rate band on the Revenue Payroll Notification (RPN) sent to the employer. When maternity leave spans two tax years, the second-year tax is collected on a cumulative basis from 1 January.

If your baby is born before maternity leave was scheduled to start, your 26 weeks of paid maternity leave begin from the actual date of birth, plus an extra period equal to the gap between the actual birth and the expected leave start date. This effectively means a premature birth never reduces total leave. You must notify your employer in writing within 14 days of the birth. Maternity Benefit will be paid for 26 weeks from the date of birth plus the extra premature-birth period.

Yes, in two specific circumstances. First, if your baby is hospitalised, you can postpone maternity leave (or additional leave) for up to 6 months, subject to your employer’s agreement, provided at least 14 weeks of leave have been taken (4 of which after the birth). Second, since 20 November 2024, the Maternity Protection Act 2024 allows postponement for ongoing treatment of a serious health condition (such as cancer treatment), with maximum postponement up to 52 weeks subject to medical evidence and employer agreement.

International employers hiring Irish staff must comply with the Maternity Protection Acts 1994 and 2004 (as amended in 2024) regardless of where the company is headquartered. For employers also sponsoring non-EEA workers, our work visa Ireland guide covers the relevant employment permit thresholds. Key obligations include: maintaining the employee’s position throughout 26 weeks paid + 16 weeks unpaid leave; conducting a pregnancy risk assessment when notified of pregnancy; providing paid time off for antenatal medical visits and one set of antenatal classes; supporting the Form MB1 application; and updating Revenue Payroll Notifications. Companies without an Irish entity typically use an Employer of Record to handle all administrative obligations. See our Best EOR in Ireland guide for verified provider rankings.

Copywriter

Christa is a Copywriter at Employsome with 17 years of professional writing experience across global brands, startups, and online publications. A native English-Finnish writer, she brings strong editorial skills and a versatile background in business, SaaS, and finance. At Employsome, Christa focuses on clear, practical content about HR, payroll, and Employer of Record topics.

Our content is created for informational purposes only and is not intended to provide any legal, tax, accounting, or financial advice. Please obtain separate advice from industry-specific professionals who may better understand your business’s needs. Read our Editorial Guidelines for further information on how our content is created.