Minimum Wage in Ireland: The Complete 2026 Guide

The minimum wage in Ireland is €14.15 per hour from 1 January 2026, a 4.8% increase from €13.50 in 2025. Ireland now ranks among the highest minimum wages in Europe and is on a government-backed path toward a statutory living wage set at 60% of median earnings by 2029. This guide covers everything: the 2026 rate, age-based sub-minimum rates, how the minimum wage actually translates to take-home pay after tax, PRSI, and USC, how Ireland compares to other EU countries, sector-specific rates under Employment Regulation Orders, the upcoming auto-enrolment pension, and the full history of minimum wage increases since 2000.

Table of Contents

- The 2026 Rate: €14.15 Per Hour

- Age-Based Rates: What Under-20s Earn

- What a Minimum Wage Worker Actually Takes Home

- What Employers Actually Pay

- How the Minimum Wage in Ireland Has Changed Over Time

- The Living Wage: Where Ireland Is Heading

- Sector-Specific Minimum Rates

- Auto-Enrolment Pension: The New Employer Cost from 2026

- How the Minimum Wage in Ireland Compares in Europe

- Working Hours, Overtime, and Annual Leave

- Enforcement and Employee Rights

- What This Means for International Employers

- FAQs

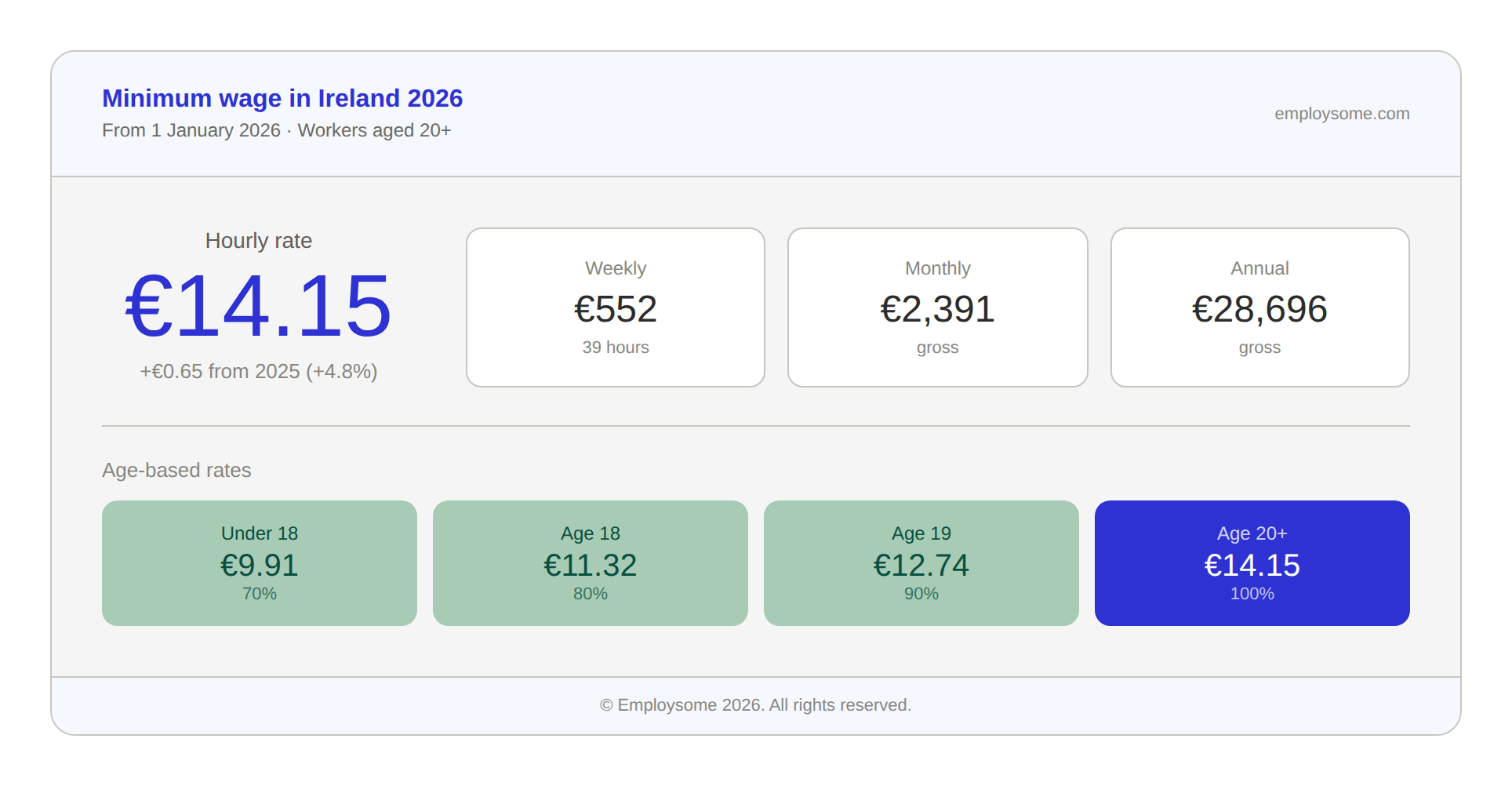

The minimum wage in Ireland increased to €14.15 per hour on 1 January 2026. That is €0.65 more than the 2025 rate of €13.50, a 4.8% increase confirmed in Budget 2026 following the Low Pay Commission’s recommendation. For a full-time worker on a standard 39-hour week, that works out to €551.85 gross per week, or roughly €28,696 gross per year.

But the headline rate only tells part of the story. Ireland’s tax system means a minimum wage worker does not take home €14.15 for every hour worked. Income tax, the Universal Social Charge (USC), and Pay-Related Social Insurance (PRSI) all reduce the net figure. Employers pay additional costs on top of the gross wage through employer PRSI. And Ireland is in the middle of a significant policy shift: the government has committed to transitioning the minimum wage into a statutory living wage pegged to 60% of median earnings, a move now targeted for 2029.

This guide breaks down the minimum wage in Ireland as it actually works in 2026: what you earn, what you take home, what your employer actually pays, how Ireland compares to the rest of Europe, and where the rate is heading next.

The 2026 Rate: €14.15 Per Hour

The minimum wage in Ireland applies to all employees aged 20 and over, regardless of whether they work full-time, part-time, temporary, casual, or seasonal hours. It is set under the National Minimum Wage Act 2000 and reviewed annually by the Low Pay Commission, an independent body that makes recommendations to the Minister for Enterprise, Trade and Employment.

The €14.15 rate is a gross figure, meaning it is the amount before any deductions for tax, USC, or PRSI. It applies to most employees with limited exceptions: close family relatives of a sole trader employer and apprentices under the Industrial Training Act 1967 are excluded.

For minimum wage purposes, gross pay includes basic hourly pay, shift premiums, and service charges distributed through payroll. It does not include overtime premiums, tips paid directly by customers, or non-cash benefits such as health insurance or company cars. Where an employer provides board or lodging, these can be included in the gross pay calculation at fixed statutory rates: €1.27 per hour worked for meals and €33.42 per week (or €4.77 per day) for accommodation.

Age-Based Rates: What Under-20s Earn

The minimum wage in Ireland has a tiered structure for younger workers. Employees under 20 receive a percentage of the full adult rate:

|

Age |

Percentage of Adult Rate |

Hourly Rate (2026) |

|

20 and over |

100% |

€14.15 |

|

19 |

90% |

€12.74 |

|

18 |

80% |

€11.32 |

|

Under 18 |

70% |

€9.91 |

These sub-minimum rates apply based on the employee’s age, not their experience. Once an employee turns 20, they are entitled to the full €14.15 rate regardless of how long they have been working. There is no “training rate” or “first year of employment” reduction in the current system, which is a change from earlier versions of the legislation.

Employers hiring younger workers should be careful to move employees to the next rate band on their birthday, not at the start of the next pay period. Paying the wrong age-based rate, even by a few days, is a compliance breach.

What a Minimum Wage Worker Actually Takes Home

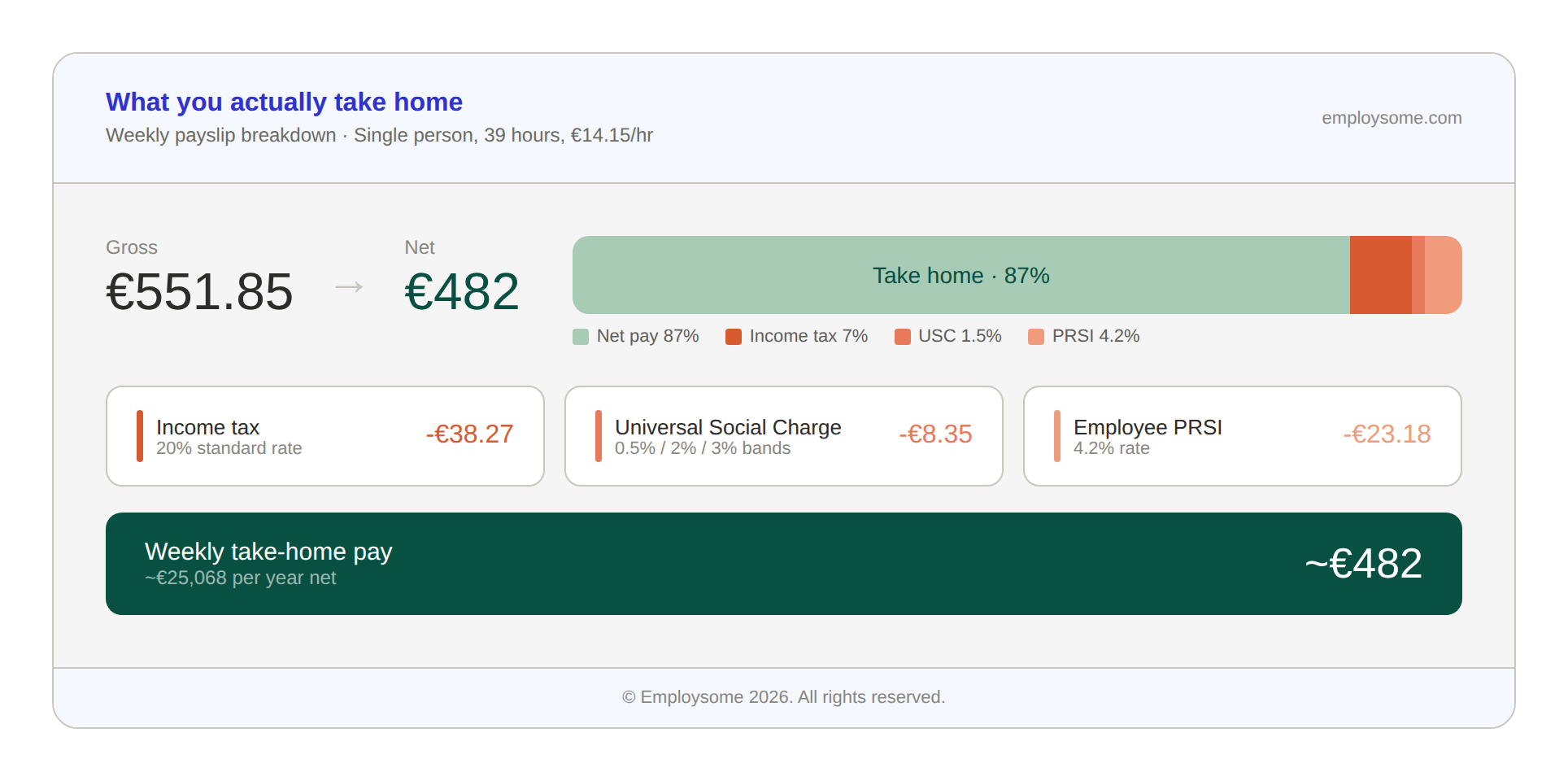

This is where the minimum wage in Ireland gets real. The gross rate of €14.15 is not what lands in the employee’s bank account. Ireland’s tax system has three layers of deductions that reduce take-home pay.

For a single person with no dependents working 39 hours per week on the minimum wage:

- Gross annual pay: approximately €28,696

- Income tax: Ireland has a dual-rate system. The first €44,000 (for a single person in 2026) is taxed at 20%. A minimum wage worker earning €28,696 falls entirely within the standard rate band. After applying the personal tax credit (€1,875) and the employee tax credit (€1,875), the effective income tax bill is approximately €1,989 per year.

- Universal Social Charge (USC): USC is a tax on gross income charged at tiered rates. For 2026, the first €12,012 is charged at 0.5%, the next €13,748 (up to €25,760) at 2%, the next €2,940 (up to €28,700) at 3%, and anything above €28,700 at 4%. The 2% USC band was increased by €1,318 in Budget 2026 specifically so that full-time minimum wage workers remain below the 3% threshold for most of their income. Total USC for a minimum wage worker is approximately €434 per year.

- Employee PRSI: The employee PRSI rate is 4.2% (rising to 4.35% from 1 October 2026). Employees earning €352 or less per week are exempt. A minimum wage worker earning €551.85 per week is above this threshold, so PRSI applies to all earnings. A sliding scale PRSI credit of up to €12 per week applies where weekly income is between €352 and €424, but at €551.85 per week the credit does not apply. Total employee PRSI is approximately €1,205 per year (before the October increase).

- Approximate net annual pay: roughly €25,068, or about €482 per week.

That means a minimum wage worker in Ireland takes home approximately 87% of their gross pay. The effective deduction rate of around 13% is relatively low by European standards, largely because the personal tax credits and USC band design are calibrated to protect low earners.

What Employers Actually Pay

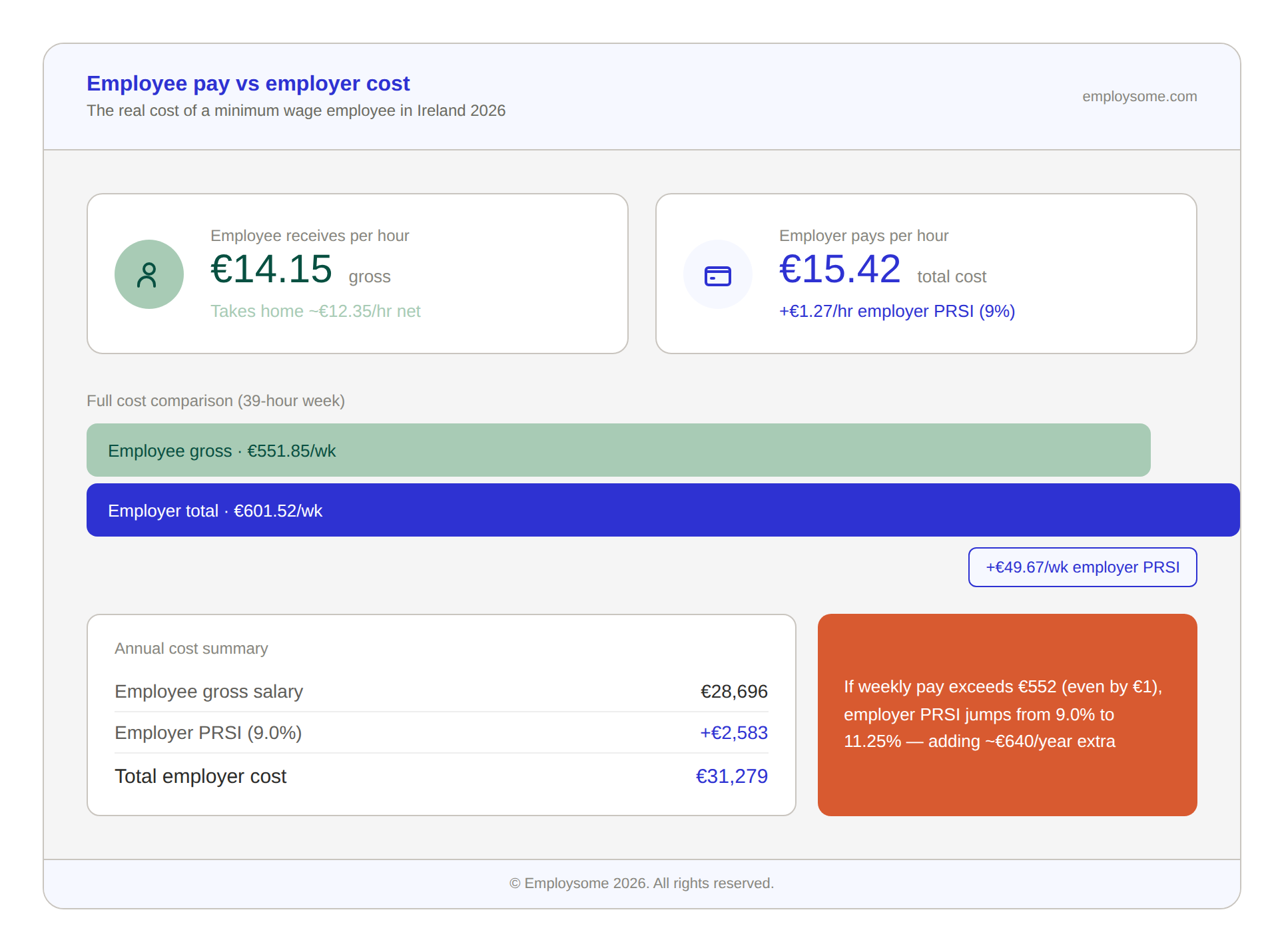

The minimum wage in Ireland is €14.15 per hour from the employee’s perspective. From the employer’s perspective, the cost is higher because of employer PRSI.

Employer PRSI rates (2026):

For employees earning more than €552 per week (which a full-time minimum wage worker does at €551.85, just below the threshold), the employer PRSI rate is 11.25%. For employees earning €552 or less per week, the reduced rate is 9.0%. The threshold was adjusted in Budget 2026 specifically to prevent full-time minimum wage workers from triggering the higher employer PRSI rate.

From 1 October 2026, employer PRSI rates increase by a further 0.15% to 11.40% (standard) and 9.15% (reduced), as part of the government’s PRSI roadmap to fund auto-enrolment pensions and expanded social insurance benefits.

For a full-time minimum wage employee on exactly €551.85 per week (just under the €552 threshold), the employer pays the reduced rate of 9.0%, adding approximately €49.67 per week or €2,583 per year to the employment cost. The total employer cost is therefore approximately €31,279 per year for a minimum wage employee, not €28,696.

If weekly earnings are even slightly above €552 (for example, due to a small amount of overtime or a shift premium), the employer PRSI jumps to 11.25% on all earnings, adding approximately €62.08 per week instead. This threshold effect is one of the most common payroll pitfalls for Irish employers. A single extra hour of work can increase the employer’s PRSI cost by over €640 per year.

How the Minimum Wage in Ireland Has Changed Over Time

Ireland introduced its national minimum wage in 2000 at €5.59 per hour under the National Minimum Wage Act 2000. Since then, it has increased 16 times, with the rate held flat during the financial crisis years (2008-2015). The pace of increases accelerated significantly from 2022 onward as the government moved toward the living wage target.

|

Year |

Rate Per Hour |

Change |

|

2000 |

€5.59 |

Introduced |

|

2007 |

€8.65 |

+€0.35 |

|

2011 |

€7.65 |

-€1.00 (restored to €8.65 later in 2011) |

|

2016 |

€9.15 |

+€0.50 |

|

2018 |

€9.55 |

+€0.30 |

|

2019 |

€9.80 |

+€0.25 |

|

2020 |

€10.10 |

+€0.30 |

|

2022 |

€10.50 |

+€0.40 |

|

2023 |

€11.30 |

+€0.80 |

|

2024 |

€12.70 |

+€1.40 |

|

2025 |

€13.50 |

+€0.80 |

|

2026 |

€14.15 |

+€0.65 |

The rate has increased by 48% in nominal terms since 2018 alone (from €9.55 to €14.15). After adjusting for inflation, real purchasing power gains have been more modest, though the 2026 increase of 4.8% outpaced the 2025 CPI of 2.8%, meaning minimum wage workers gained real purchasing power in 2026.

The Living Wage: Where Ireland Is Heading

The minimum wage in Ireland is not a static policy. The government has committed to transitioning from the national minimum wage to a national living wage, defined as 60% of the median hourly wage. This target was originally set for 2026 but has been pushed to 2029.

The living wage concept differs from the minimum wage in a fundamental way. The minimum wage is a legal floor set by government. The living wage is calculated based on what a single person without dependents actually needs to earn to meet basic living costs including rent, food, transport, and healthcare. The Living Wage Technical Group, an independent research body, currently estimates the living wage at approximately €15.40 per hour, significantly above the 2026 minimum of €14.15.

The government’s approach uses a fixed threshold method (60% of median earnings) rather than the “basket of goods” method used by the Living Wage Technical Group. Once the transition is complete, annual minimum wage reviews will be anchored to median wage data rather than discretionary recommendations. The Low Pay Commission has also indicated that after reaching 60%, the government may consider gradually increasing the target to 66% of median earnings.

For employers, this means the minimum wage in Ireland will continue to rise each year through at least 2029, likely reaching €15 or more per hour. Companies should factor this trajectory into long-term workforce planning and compensation budgets.

For a detailed look at how minimum wage earnings compare to broader pay levels across the Irish economy, see our average salary in Ireland guide.

Sector-Specific Minimum Rates

Some sectors in Ireland have minimum pay rates that are higher than the national minimum wage. These are set through Employment Regulation Orders (EROs) issued by Joint Labour Committees (JLCs) and are legally binding.

The most notable sector-specific rate in 2026 is contract cleaning, where the minimum hourly rate increased to €14.80 per hour from 1 January 2026 (compared to the national minimum of €14.15). The security sector also has its own ERO rates that typically exceed the national minimum.

Where an ERO applies, employers must pay whichever rate is higher: the national minimum wage or the ERO rate. Paying the national minimum when a higher ERO rate applies is a compliance breach enforceable by the Workplace Relations Commission (WRC). Employers should check the WRC website for current EROs in their sector.

Auto-Enrolment Pension: The New Employer Cost from 2026

One of the most significant payroll changes affecting Irish employers alongside the minimum wage increase is the introduction of automatic enrolment (AE) for retirement savings, which launched on 30 September 2025 with employer obligations beginning from 2026.

Under the scheme, employees aged 23 to 60 earning over €20,000 who are not already in a workplace pension will be automatically enrolled. The contribution rates start at 1.5% each from employer and employee in the first three years, rising to 3% each in years four to six, then 4.5% in years seven to nine, and finally 6% each from year ten onward. The government also contributes €1 for every €3 the employee puts in.

For minimum wage employers, this adds a new mandatory cost on top of employer PRSI. In the initial phase, the employer contribution of 1.5% on a minimum wage salary of €28,696 is approximately €430 per year. By the time the scheme matures at 6%, this rises to approximately €1,722 per year, a significant addition to total employment cost.

How the Minimum Wage in Ireland Compares in Europe

Ireland consistently ranks among the top five EU countries for minimum wage levels, though direct comparisons must account for differences in working hours, tax systems, and cost of living.

|

Country |

Minimum Wage (Hourly) |

Approx. Monthly Gross |

Employer SI |

Effective Tax on Min Wage |

|

Luxembourg |

€14.86 |

~€2,571 |

~15% |

Low |

|

Ireland |

€14.15 |

~€2,391 |

~9-11.25% PRSI |

~13% |

|

Netherlands |

€14.06 |

~€2,070 |

~18% |

Low |

|

Germany |

€12.82 |

~€2,162 |

~21% |

Low |

|

France |

€11.88 |

~€1,802 |

~45% |

Very low |

|

Belgium |

€12.30 |

~€1,955 |

~27% |

Moderate |

|

Spain |

€8.45 |

~€1,323 |

~30% |

Low |

|

Poland |

PLN 30.50 (~€7.10) |

~€1,100 |

~20% |

Low |

Ireland ranks second in the EU for hourly minimum wage behind Luxembourg, but Ireland’s relatively lower employer social insurance burden (9-11.25% vs France’s 45% or Belgium’s 27%) means the total cost of employing a minimum wage worker in Ireland is more competitive than the headline rate suggests. However, Ireland’s high cost of living, particularly housing in Dublin, means purchasing power for minimum wage workers is lower than the nominal ranking implies.

Working Hours, Overtime, and Annual Leave

The minimum wage in Ireland applies to all hours worked. Understanding how working time is structured matters for calculating whether an employee is actually receiving the minimum wage on average.

Ireland has no single statutory standard work week, but 39 hours is the most common contractual arrangement. The Organisation of Working Time Act 1997 sets a maximum average of 48 hours per week, calculated over a 4-month reference period (extendable to 6 or 12 months in certain sectors). Employees must receive at least 11 consecutive hours of rest in every 24-hour period, and one full day off per week (or two days in a fortnight).

There is no statutory overtime rate in Ireland. Overtime pay is determined entirely by the employment contract or any applicable collective agreement. This means an employer can legally pay the same hourly rate for overtime as for regular hours, provided the average hourly rate does not fall below the minimum wage when calculated over the pay reference period (which can be a week, fortnight, or month, but not longer than a month).

Employees are entitled to a minimum of 4 working weeks (20 days) of paid annual leave per year under the Organisation of Working Time Act. This is in addition to 9 public holidays (10 in some years). Employers can require employees to take annual leave at specific times with reasonable notice.

Enforcement and Employee Rights

The Workplace Relations Commission (WRC) is responsible for enforcing the minimum wage in Ireland. Employees who believe they are not receiving the correct rate can request a written statement of their average hourly pay for any pay reference period in the previous 12 months. The employer must provide this within 4 weeks.

If the employer fails to pay the minimum wage, the employee can file a complaint with the WRC within 6 months of receiving (or being entitled to receive) the written statement. The WRC can also conduct proactive inspections. Non-compliance can result in orders to pay arrears, fines, and in serious cases, prosecution.

Importantly, employees who are dismissed for asking about or claiming the minimum wage can bring an unfair dismissal claim regardless of their length of service. This protection applies from day one of employment.

What This Means for International Employers

For companies hiring in Ireland without a local entity, an Employer of Record handles payroll registration with Revenue, PAYE and USC withholding, employer and employee PRSI contributions, minimum wage compliance, auto-enrolment pension obligations, and all statutory leave calculations. Ireland’s payroll system is well-regulated and transparent, but the interaction between income tax bands, USC thresholds, PRSI rate tiers, and the new auto-enrolment scheme creates genuine complexity, particularly around the employer PRSI threshold where a few euro in weekly pay can trigger a significantly higher contribution rate. For a broader overview of how Ireland fits into international hiring strategies, see our average salary in Ireland guide for context on where minimum wage sits relative to the broader market.

Frequently Asked Questions

The minimum wage in Ireland is €14.15 per hour from 1 January 2026 for employees aged 20 and over. This was a €0.65 increase from the 2025 rate of €13.50.

Yes. The minimum wage applies to all employees regardless of whether they work full-time, part-time, temporary, casual, or seasonal hours. There is no reduced rate for part-time work.

Employees aged 19 receive 90% of the adult rate (€12.74), employees aged 18 receive 80% (€11.32), and employees under 18 receive 70% (€9.91).

A single person working 39 hours per week on €14.15 per hour earns approximately €28,696 gross per year and takes home approximately €25,068 net after income tax, USC, and PRSI. That is roughly 87% of gross pay.

Employers pay PRSI at 9.0% for employees earning €552 per week or less, and 11.25% for employees earning above that threshold. From October 2026, these rates increase by 0.15%. Employers must also contribute to the new auto-enrolment pension scheme (starting at 1.5% of salary).

Yes. The government has committed to replacing the national minimum wage with a national living wage set at 60% of median hourly earnings, now targeted for 2029. Annual increases will continue in the meantime, meaning the minimum wage in Ireland will rise each year through at least 2029.

Yes. Sectors covered by Employment Regulation Orders (EROs) have their own minimum rates. Contract cleaning has a minimum of €14.80 per hour in 2026, above the national minimum of €14.15. The security sector also has higher ERO rates.

Employees can request a written pay statement and file a complaint with the Workplace Relations Commission within 6 months. The WRC can order arrears, impose fines, and conduct inspections. Employees dismissed for claiming the minimum wage have unfair dismissal protection from day one.

Written by

Dane Cobain is a Copywriter at Employsome and an accomplished author whose work spans fiction, non-fiction, and professional writing. Over the past decade, he has built a strong track record creating straightforward content for the HR, payroll, and corporate sectors. Dane brings a storyteller’s eye to the evolving world of global employment, with a particular focus on Employer of Record and PEO models. His articles explore industry trends and dedicated Best Of Guides when managing an international workforce.

Our content is created for informational purposes only and is not intended to provide any legal, tax, accounting, or financial advice. Please obtain separate advice from industry-specific professionals who may better understand your business’s needs. Read our Editorial Guidelines for further information on how our content is created.

Other posts

Review other blog posts