Employsome Quadrant: EOR Market Leaders (2026)

An independent map of the EOR market, plotting 28 providers across two axes: Operational Depth and Global Reach. Where Deel, Remote, G-P, Pebl, Multiplier and 23 others sit in 2026, and what the picture tells you about the shortlist for your next global hire.

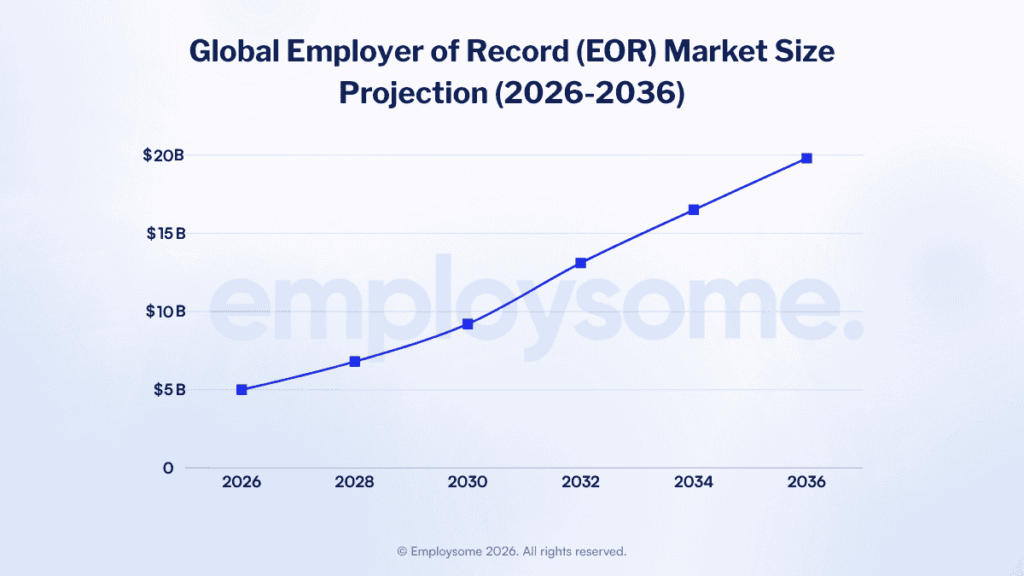

The Employer of Record (EOR) industry has, in five years, gone from a fragmented set of compliance shops to a category dominated by a handful of well-funded platforms, with fintech giants now circling the perimeter. Deel sits at a $17.3 billion valuation. Rippling at $16.8 billion. Velocity Global has rebranded to Pebl. Payoneer has bought two EOR providers in 18 months. Revolut has announced its own EOR with GlobalHire.

Buyers asked to make sense of this market still get the same two things: vendor pages claiming everyone is “the leader,” and analyst reports locked behind $5,000 paywalls. So we built our own.

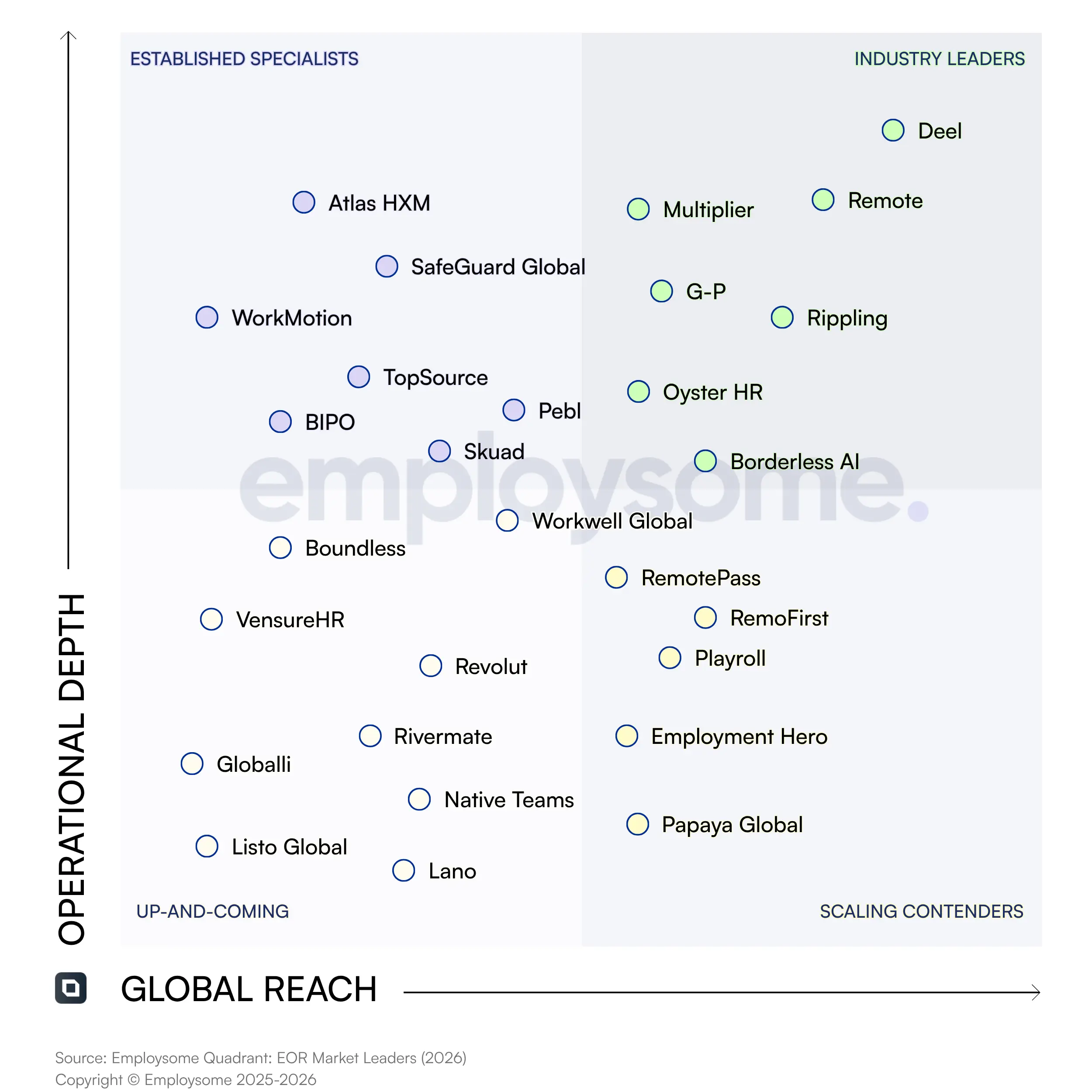

The Employsome EOR Market Quadrant 2026 plots 28 EOR providers across two axes that actually matter when shortlisting: Operational Depth on the y-axis and Global Reach on the x-axis. It is not a satisfaction score. It is not a marketing exercise. It is a structural map of where each provider sits in the market today, and where the gaps and pressures are.

For the macro picture driving this consolidation, see our EOR market size and trends report. For the deals reshaping the field, see the EOR Funding and M&A Report 2026.

The Two Axes: Operational Depth and Global Reach

Most EOR comparisons rank providers on one dimension: country count. That metric flatters partner-network aggregators and punishes platforms that quietly own their entities. We split it.

Operational Depth (y-axis). A composite of four signals: percentage of countries served via owned legal entities versus third-party partners, whether payroll runs in-house or is outsourced, the breadth of in-jurisdiction compliance and benefits coverage, and the maturity of the platform itself (automation, integrations, AI). A provider operating its own entity in Germany controls the contract, the tax filings, the IP transfer, and the termination process. A provider relying on a local partner controls the relationship with that partner, and not much else. The difference shows up the day something goes wrong, which is why this dimension belongs on the y-axis. For the underlying concept, see our explainer on owned entity vs. in-country partner models.

Global Reach (x-axis). Country count weighted by where the provider actually has scale. Owned-entity countries get full weight. Partner-served countries get half. Active employee count, customer base, and live revenue from a given market all matter more than a logo on a coverage map. A provider claiming “180 countries” through partner aggregation does not sit in the same place as a provider with 80 owned entities and tens of thousands of active employees.

The combination is what produces the four quadrants. Both axes high means the provider has invested in the infrastructure to operate at global scale. Both axes low means the opposite, regardless of marketing claims. The diagonal positions matter most: deep but narrow (Established Specialists) vs. wide but thin (Scaling Contenders).

A note on methodology. Placements draw on our review database of 100+ providers, public funding and customer data, our own onboarding tests where we have run them, and ongoing feedback from buyers. Providers can suggest factual corrections; positions are ours.

Industry Leaders: Deel, Remote, Multiplier, G-P, Rippling, Oyster, Borderless AI

The top-right quadrant. Providers here combine deep operational infrastructure with the largest global footprints. They are the names that win most enterprise shortlists, and the gap between them and everyone else is widening.

Deel is the rightmost dot on the chart for a reason. Over $1 billion ARR, around 35,000 customers, 1.5 million workers managed across 150+ countries. The 2025 Series E pushed its valuation to $17.3 billion. The DOJ investigation into the Rippling spying allegations is an open risk worth tracking, but it has not yet dented the operational reality: if you need to hire fast in 80+ countries, Deel is on most shortlists by default.

Remote is the compliance-first counterweight. The owned-entity-only positioning is a real product choice, not just marketing, and it shows up in IP transfer language, contract templates, and termination support. The recent acquisition of Atlas (the AI expense management product, not Atlas HXM) signals Remote wants to bundle financial operations on top of EOR, the same playbook Deel ran first.

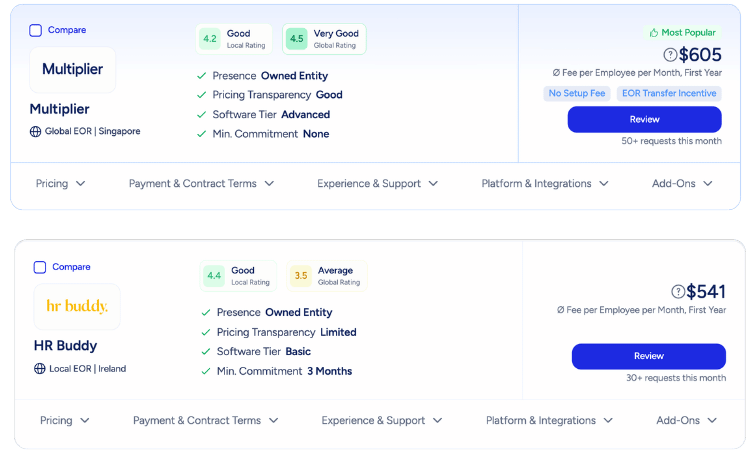

Multiplier sits as the most operationally serious of the second wave. Strong APAC depth from its Singapore origins, fast-improving European coverage, and a pricing posture that undercuts Deel and Remote without resorting to the partner-network model. We have seen it win deals on platform usability where the bigger names lost on bloat

G-P (formerly Globalization Partners) is the original incumbent. Owned entities in every country it covers, the broadest enterprise track record in the category, and a service-led delivery model that suits regulated industries and complex international hires. Pricing is the highest in the market and the sales cycle reflects that.

Rippling reaches Industry Leader territory through breadth, not depth. The EOR is one part of an HRIS, IT management, and finance suite. Buyers who already run Rippling for US payroll often expand into EOR by inertia. The unresolved litigation against Deel keeps the company in the news, but the underlying product trajectory is independent of that.

Oyster HR sits at the lower edge of the Industry Leaders quadrant. Distributed-by-design positioning, strong onboarding UX, and a customer base skewed to mid-market tech. Funding has slowed compared to Deel and Remote, which is reflected in the position. Still firmly above the operational threshold and broad enough in coverage to belong here.

Borderless AI is the newest name in this group and the one most likely to provoke debate. Cohere co-founders on the cap table, $32M raised, an AI-agent-first product positioning, and a faster-than-expected expansion of owned-entity coverage. We have included it in Industry Leaders because the operational depth scoring is closer to the top tier than its valuation suggests, and because the trajectory is steep. Watch this dot move further right over the next 12 months.

Compare 100+ EORs, real-time & for free

See pricing, scoring, and country fit for Employer of Record providers, side by side.

Get started free

Established Specialists: Atlas HXM, WorkMotion, Safeguard, Pebl, TopSource, BIPO, Skuad

The top-left quadrant. Providers with serious operational infrastructure but narrower geographic or segment focus. For many buyers, an Established Specialist is the better answer than an Industry Leader, especially when the hires are concentrated in one region.

Atlas HXM is one of the most under-rated names on the chart. Owned entities in 160+ countries, deep enterprise pedigree, named a Leader in the 2025 Everest Group EoR PEAK Matrix and the 2025 NelsonHall NEAT report. Sits in Established Specialists rather than Industry Leaders because customer scale lags Deel and Remote, but the entity infrastructure is comparable.

WorkMotion is the strongest pure-play European specialist on the chart. Berlin-based, native German-language onboarding, deep DACH compliance know-how, and a foreign-employer registration product (WorkFlex) that handles short-term cross-border work without the EOR overhead. For Mittelstand companies, WorkMotion is often a better fit than any global platform.

Safeguard Global is the most enterprise-tilted name in this quadrant. Two decades of global payroll heritage, owned-entity coverage in 65+ countries, and a service model built for HR teams that already know what they want. Repeatedly named a Leader in NelsonHall’s NEAT analysis. Less hype than Deel, more depth than most of the bottom half.

Pebl (formerly Velocity Global) rebranded in 2025 around an AI-first message and a new assistant called Alfie. The underlying business is one of the broadest entity footprints in the industry and a global mobility team that is among the strongest for immigration-heavy use cases. Whether the new positioning resonates with buyers is the open question; the operational base is solid.

TopSource is the quiet operator. UK-headquartered, owned entities across Europe and APAC, particularly strong in India and the UK. Less marketing presence than the rest of this quadrant, which is part of why buyers who find them tend to stay.

BIPO is the APAC specialist. Singapore-headquartered, 50+ offices across the region, particularly strong in China, Hong Kong, Singapore, Malaysia, and the Philippines. Coverage outside Asia is partner-led, which is why the chart pulls it left rather than right. Inside its core region, it competes with anyone.

Skuad sits in this quadrant post-acquisition by Payoneer. The integration with Payoneer’s payments and FX infrastructure has materially improved the operational scoring; the constraint on Global Reach is partly a transition effect as the rebrand to Payoneer Workforce Management plays out. Worth re-evaluating in six months.

Scaling Contenders: RemoFirst, RemotePass, Playroll, Employment Hero, Papaya Global

The bottom-right quadrant. Wide global coverage, but the operational depth has not caught up with the country count. These providers compete on price, speed, or one specific regional strength. Some will move up. Some will be acquired. A few will not be on the chart in two years.

RemoFirst is the price floor of the global market. Pricing starts at $199 per employee per month, undercutting Deel and Remote by 60-70%. Coverage in 180+ countries is almost entirely partner-network. The trade-off is explicit and works for early-stage companies hiring one or two people in a country, less well for enterprise compliance.

RemotePass is MENA-strong and globally present. Headquartered in Dubai, deep UAE and broader Middle East compliance know-how, and a contractor management product alongside the EOR. The bottom-right placement reflects that the partner network outside MENA does most of the heavy lifting.

Playroll is the Africa and emerging markets specialist with global ambitions. Owned by VAT IT Group, which gives it real entity infrastructure in markets most competitors avoid (South Africa, Nigeria, Kenya, several LATAM markets). Outside that core, Playroll is a partner-network model, hence the placement.

Employment Hero is the Australia-anchored player. Strong domestic SMB market position, AI investment under the HeroForce brand, and a 2025 acquisition by KKR that has accelerated US and UK push. Global EOR coverage is real but uneven outside ANZ, and the operational depth varies sharply by country.

Papaya Global is the most interesting case in this quadrant. Last valued at $3.7B in 2021, raised over $440M, pivoted from EOR toward an integrated workforce payments platform, and reportedly entered sale discussions in early 2026 at a $3.5B-$4.5B valuation. Strong payroll engine, but the EOR coverage relies on partners outside a few core markets. Whichever way the sale resolves, Papaya’s position on the chart will move.

Up-And-Coming: Boundless, VensureHR, Workwell Global, Revolut, Globalli, Rivermate, Native Teams, ListoGlobal, Lano

The bottom-left quadrant. Some of these names are early-stage and climbing. Some are established players with deliberately narrow scope. Some are giants entering EOR from adjacent categories. Lumping them together as “Up-And-Coming” is the only honest label, because their trajectories are radically different.

Boundless sits here mid-transition. Acquired by Payoneer in January 2026, the integration is ongoing, and we expect the position to move once the combined Payoneer Workforce Management story settles. Pre-acquisition, the European compliance work was strong, particularly in Ireland and the UK.

VensureHR is the largest name in the quadrant by client count. PEO-first, with a global EOR offering layered on through a partner-network model. 108+ acquisitions including Listo Global. Sits low on operational depth specifically because the EOR delivery is brokered, not owned.

Workwell Global is the recruitment-and-staffing-tilted player. Strong agency partnerships, an EOR offering built around the contractor and recruiter use case, and a UK-and-Europe operational base. Narrow but defensible.

Revolut is the wildcard on the chart. Announced GlobalHire as an EOR product in 2025, $75B fintech valuation, 39 owned legal entities, 65 million customers. The placement reflects the present, not the potential. Revolut has the infrastructure to vault into Industry Leaders within 18 months if it commits, and the cross-sell economics to compress mid-market EOR pricing meaningfully. See our take on what Revolut GlobalHire means for the market.

Globalli (formerly Helios) and Rivermate (the rebrand consolidating Eos Global Expansion, Serviap Global, and Hightekers’ EOR operations) are both in transition. Rivermate’s owned-entity footprint via the underlying Eos heritage is non-trivial, particularly across LATAM and APAC. Worth watching as the consolidated brand settles.

Native Teams is freelance and creator-economy native. Strong in Eastern Europe, with a product flow optimized for individual contractors converting to employment status. The EOR is real but narrower than the global generalists.

Lano is the German-headquartered global payroll-and-EOR aggregator with a particularly clean platform UX, but the operational delivery leans on partners. Both are real options for buyers with the right country mix; neither is competing for global enterprise mandates.

Listo Global is LATAM-specialized, recently absorbed into VensureHR.

The honest summary of this quadrant: it is the most volatile. We believe that half the names here will look different on the chart this time next year.

Three Forces Reshaping the Quadrant

The Quadrant is a snapshot. The market is in motion. Three forces will determine where the dots sit a year from now.

1. Fintech entry compresses the middle

Payoneer has bought Skuad and Boundless. Revolut has launched GlobalHire. Both companies move money across borders for a living, both have legal entities in 30+ countries already, and both can subsidise EOR pricing with revenue from FX, payments, and lending. The providers most exposed are the ones charging $500-700 per employee per month with no significant differentiation beyond payroll and compliance. Deel and Remote have the scale and product breadth to absorb the pressure. Mid-tier generalists do not. Expect aggregate EOR pricing to drop 15-25% across the mid-market within 18 months of GlobalHire’s full launch. For the underlying numbers, see our EOR cost guide.

2. AI replaces the service layer, not the entity layer

Borderless AI generates compliant employment contracts in seconds and runs payroll across 170+ countries in roughly 20 minutes. Pebl has launched Alfie across 50+ languages. G-P’s Gia was named 2025 Top HR Product of the Year. The pattern is clear: AI is collapsing the human service overhead between the buyer and the compliance infrastructure. What AI cannot replace is the registered legal entity that holds the employment liability. The winners over the next two years will be providers that combine owned entities with AI-powered service delivery. Providers still leaning on large manual ops teams will see margins squeezed.

3. M&A consolidates the long tail

Between 2024 and early 2026 the EOR industry saw more M&A activity than the prior five years combined: Deel acquired Hofy, Assemble, PaySpace and a string of others; Payoneer absorbed Skuad and Boundless; Remote bought Atlas; KKR took Employment Hero private; Rivermate consolidated three EOR brands under one name; Papaya is reportedly in sale talks. The pattern: capital is entering the category through M&A, not venture rounds. The market is bifurcating into a few dominant platforms and a network of regional specialists. The mid-tier generalist EOR, with no clear differentiation, is the segment under most pressure.

How to Use the Quadrant When Choosing an EOR

A 2×2 chart is not a shortlist. It is a starting filter. Used well, the Quadrant should narrow 100+ providers down to a handful you actually evaluate.

Start by asking how concentrated your hiring is. If 80% of your hires are in one region, go straight to the Established Specialists quadrant. WorkMotion for DACH, BIPO for APAC, Atlas HXM for enterprise complexity, TopSource for India and the UK. You will get sharper local expertise than any global platform delivers, often at lower cost.

If hiring is genuinely distributed across 5+ countries, look at Industry Leaders. Deel and Remote are the obvious shortlist. Multiplier and G-P are credible alternatives depending on your priority. Multiplier wins on platform UX and pricing; G-P wins on enterprise pedigree and regulated-industry compliance.

If you are price-led and the hires are simple, the Scaling Contenders quadrant is rational, with caveats. RemoFirst at $199 per employee per month is real, but the partner-network model means escalation paths are longer when something breaks. For early-stage companies with one or two hires per country, this is often the right trade-off. For anything regulated or compliance-sensitive, it is not.

The Up-And-Coming quadrant is for specific use cases. Native Teams for freelance-heavy hiring in Eastern Europe. Lano for German-anchored teams. Rivermate or Globalli once the rebrands stabilise. Revolut, if you already use Revolut Business and the country mix is right.

The most expensive mistake is choosing a provider whose position on the chart does not match your hiring profile. The second most expensive is choosing on price alone in the Up-And-Coming quadrant for hires that need real compliance depth. For more on the cost framework, our EOR definition and how it works piece is the cleanest starting point.

💡 Employsome Insight

The Quadrant is a structural snapshot, not a verdict on which provider is “best.” A buyer hiring 12 engineers in Germany and Spain might also consider looking at Established Specialists before Industry Leaders. A buyer hiring across 25 countries should not. The single most expensive mistake we see is matching the wrong quadrant to the wrong hiring profile, then attributing the resulting problems to the provider rather than the choice.

Frequently Asked Questions

The Employsome EOR Market Quadrant 2026 is an independent map of 28 employer of record providers, plotted on two axes: Operational Depth (entity ownership, in-house payroll, compliance posture) and Global Reach (country count weighted by active employees and customers). It is not a satisfaction score and not a paid ranking. The full methodology is described in the article.

In our 2026 Quadrant, the Industry Leaders are Deel, Remote, Multiplier, G-P, Rippling, Oyster, and Borderless AI. Each combines deep operational infrastructure with broad global coverage. Deel is the rightmost dot on the chart by scale, with over $1B ARR and a $17.3B valuation.

Industry Leaders combine deep operational infrastructure with the widest geographic footprint. Established Specialists have comparable operational depth but narrower geographic or segment focus. For buyers hiring concentrated in one region, an Established Specialist often delivers sharper local expertise than a global platform.

A provider that owns its legal entity in a country controls the contract, the tax filings, the IP transfer, and the termination process directly. A provider relying on a third-party in-country partner controls the relationship with that partner, but not the underlying employment. The difference matters most when something goes wrong, which is why we treat it as a primary axis.

Three forces are in motion. Fintech entrants like Revolut and Payoneer are pressuring mid-market pricing. AI is collapsing the human service overhead inside every provider. M&A is consolidating the long tail. Expect Borderless AI to move further right, Revolut to move up sharply if it commits, several EORs in Up-And-Coming to be acquired, and at least one Scaling Contender to drop off the chart entirely.

No. Placements are independent of any commercial relationship. Some providers are listed on Employsome, some are not. Some are partners, some are not. Providers can suggest factual corrections. Positions are determined by our editorial team. For our full editorial standards, see our Editorial Guidelines.

Courtney Pocock is a Copywriter at Employsome with 15+ years of experience writing for the HR, corporate, and financial sectors. She has a strong interest in global business expansion and Employer of Record / PEO topics, focusing on news that matters to business owners and decision-makers. Courtney covers industry updates, regulatory changes, and practical guides to help leaders navigate international hiring with confidence. Connect with Courtney on LinkedIn.

Our content is created for informational purposes only and is not intended to provide any legal, tax, accounting, or financial advice. Please obtain separate advice from industry-specific professionals who may better understand your business’s needs. Read our Editorial Guidelines for further information on how our content is created.