Health Insurance in Nigeria 2026: Complete Employer Guide

Health insurance in Nigeria became mandatory under the NHIA Act 2022 for any employer with five or more staff, with coverage extending to the employee, spouse, and up to four children. This 2026 guide covers the NHIA Act, the major HMO providers (AXA Mansard, Hygeia, Avon, Leadway, Reliance), 2026 group health insurance pricing tiers, mandatory pension and labour fund contributions, and total employer cost when hiring Nigerian workers.

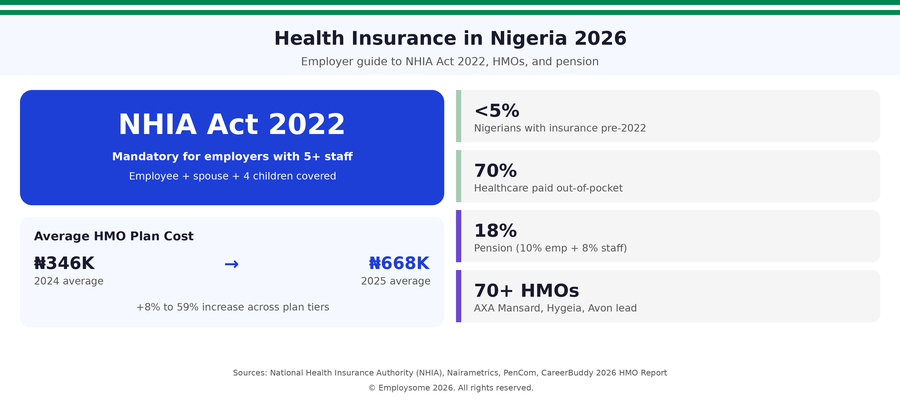

Health insurance in Nigeria entered a new era with the National Health Insurance Authority (NHIA) Act 2022, which made health insurance mandatory for all employers with five or more employees across both the formal and informal sectors. Despite this, fewer than 5% of Nigeria’s 220 million population had any form of health insurance heading into 2026, with over 70% of Nigerians still paying for healthcare out of pocket. The NHIA Act 2022 is the country’s most ambitious push toward Universal Health Coverage (UHC) by 2030, replacing the failed NHIS scheme that achieved less than 10% population coverage in over two decades.

For employers, the NHIA Act 2022 creates clear obligations: enrol all employees in an NHIA-approved health insurance plan covering the worker, one spouse, and up to four biological children under 18. Health insurance premiums in Nigeria rose sharply in 2025, with average annual plans climbing from ₦346,000 in 2024 to approximately ₦668,000 in 2025 driven by drug price inflation and hospital cost increases. Top-tier corporate plans from major HMOs like AXA Mansard and Hygeia now exceed ₦1.9 million per insured employee per year.

This 2026 guide to health insurance in Nigeria covers: the NHIA Act 2022 and its mandatory employer obligations, how the public sector NHIA scheme works alongside private HMOs, group health insurance market rates and pricing tiers, the major HMO providers including AXA Mansard, Hygeia, Avon, Leadway, and Reliance, total employer cost calculations including pension and labour fund contributions, and what international companies hiring need to budget when expanding into Nigeria.

National Health Insurance Authority (NHIA) Act 2022 Explained

Nigeria’s health insurance landscape is governed by the National Health Insurance Authority (NHIA) Act 2022, signed into law on 19 May 2022 by President Muhammadu Buhari. The Act repealed the National Health Insurance Scheme (NHIS) Act of 1999 and established the NHIA as the sole regulatory body overseeing all health insurance matters in Nigeria.

The NHIA Act 2022 is a fundamental shift from voluntary to mandatory enrolment. Sections 3 and 14 of the Act provide for mandatory health insurance for every Nigerian and legal resident. For employers, the practical impact is direct:

- Any employer with 5 or more staff must enrol all employees in an NHIA-approved health insurance plan

- Coverage extends automatically to the employee, one spouse, and up to four biological children under 18

- Applies to both formal and informal sector employers (including SMEs, NGOs, and family businesses)

- Employers must register with an NHIA-accredited Health Maintenance Organisation (HMO) or a State Health Insurance Scheme (SHIS)

- Penalties apply for non-compliance, including fines and exclusion from public sector procurement

In February 2026, President Bola Tinubu issued a service-wide presidential directive further strengthening NHIA enforcement. All Ministries, Departments, and Agencies (MDAs) must now enrol their employees in NHIA-approved plans, and a valid NHIA certificate is now mandatory for procurement eligibility, business licences, and permit renewals across the public sector. The NHIA also launched a digital platform for certificate verification.

The NHIA operates through three main programmes:

| NHIA Programme | Target Audience | How It Works |

| Formal Sector Social Health Insurance | Public and private sector employees | Mandatory enrolment through employer; HMO selection |

| GIFSHIP (Group, Individual and Family Social Health Insurance) | Self-employed, informal sector workers | Voluntary or community-based enrolment |

| Vulnerable Group Coverage | Pregnant women, children, elderly, disabled persons, indigents | Subsidised through Basic Health Care Provision Fund (BHCPF) |

For employers, the relevant programme is the Formal Sector Social Health Insurance scheme. Employers must select an NHIA-accredited HMO, register the company and employees, and remit monthly premium contributions. A valid National Identification Number (NIN) is required for each employee onboarding.

💡 Employsome Insight: Health Insurance Is No Longer Voluntary in Nigeria

Many international companies entering Nigeria assume health insurance is voluntary, as it was under the previous NHIS Act of 1999. This is no longer the case. The NHIA Act 2022 made enrolment mandatory for all employers with 5+ staff. While enforcement has been uneven historically, the February 2026 presidential directive significantly strengthened compliance requirements: a valid NHIA certificate is now mandatory for any business seeking government contracts, licences, or permit renewals. International employers entering Nigeria must factor NHIA enrolment into their budget and compliance roadmap from day one, not as an optional employee benefit.

Major HMO Providers in Nigeria 2026

Most employers in Nigeria meet their NHIA obligations by enrolling employees with a private Health Maintenance Organisation (HMO) rather than relying solely on the public NHIA scheme. HMOs are NHIA-accredited Third Party Administrators (TPAs) that manage employer registrations, employee enrolment, hospital network access, claims processing, and premium administration on behalf of clients.

The 2026 Nigerian HMO market is dense, with over 70 NHIA-accredited HMOs operating nationwide. The major providers include:

- AXA Mansard Health: Part of the global AXA Group; one of Nigeria’s most established HMOs with strong corporate plans, financial backing, and access to over 1,000 healthcare facilities. Six plan tiers ranging from Bronze (₦86,500) to Rhodium (₦1.939 million) per year.

- Hygeia HMO: One of Nigeria’s oldest HMOs with over 30 years of industry experience. Strong network of 2,000+ medical facilities, particularly competitive on maternity, chronic conditions, and specialist care.

- Avon HMO: A subsidiary of Heirs Holdings (Tony Elumelu Group). 2,000+ hospitals, strong wellness focus including health screenings and chronic disease management programmes for corporate clients.

- Leadway Health: Established HMO with strong customer service reputation and broad SME and corporate plan coverage.

- Reliance Health: Tech-forward, app-first HMO that pivoted to corporate-only in 2026. Popular with startups and digital-first companies.

- Bastion Health: Budget-friendly HMO with digital convenience; SME plans from ₦45,080 per employee per year.

- HCI Healthcare: Established HMO popular with corporates and government agencies.

- Novo Health Africa: Mid-market HMO with broad coverage.

- Hallmark HMO: Affordable individual and corporate plans; entry plans from ₦30,000 per year.

- Redcare Health Services: Strong network coverage for SMEs.

- NEM Health: Newer entrant with diaspora-focused options.

- Hallmark, Greenbay, Anchor, United Healthcare International: Mid-market and budget HMOs offering basic to comprehensive plans.

Most large Nigerian employers select a single primary HMO and offer it across the workforce, with senior staff sometimes given access to higher-tier plans. SMEs increasingly use health insurance distributors and brokers (MyCoverGenius, Curacel, Reliance) to compare and enrol with multiple HMOs based on cost and coverage match.

Group Health Insurance Pricing in Nigeria

Nigerian health insurance premiums rose sharply between 2024 and 2025, with increases ranging from 8% on lower-tier plans to 59% on top-tier plans. The main drivers were rising drug prices, surging hospital tariffs, currency devaluation impacting medical imports, and overall medical inflation. The average annual HMO plan price moved from ₦346,000 in 2024 to approximately ₦668,000 in 2025, and additional modest increases are expected through 2026.

Here are 2026 indicative pricing benchmarks for the major HMO plan tiers:

| Plan Tier | Annual Cost per Employee (NGN) | Typical Coverage |

| Entry / EasyCare plans | ₦12,000 to ₦30,000 | Basic outpatient, limited hospitals, no maternity |

| Basic SME plan | ₦45,000 to ₦90,000 | Outpatient, basic inpatient, basic dental, limited network |

| Mid-tier corporate plan | ₦150,000 to ₦400,000 | Comprehensive inpatient/outpatient, maternity, dental, optical, wellness |

| Premium corporate plan (e.g. AXA Silver/Gold) | ₦400,000 to ₦900,000 | Wide hospital network, comprehensive benefits, evacuation |

| Executive / international plan (e.g. AXA Rhodium) | ₦900,000 to ₦1.94 million | Top-tier hospitals, international evacuation, full coverage |

| International plan with overseas treatment | USD 1,500+ per year | Worldwide coverage, evacuation, second opinion services |

A typical Nigerian group HMO plan covers:

- Outpatient care: General practitioner consultations, specialist consultations, prescribed medication (subject to formulary), basic diagnostic tests

- Inpatient care: Hospitalisation, surgery, anaesthetist fees, ICU, hospital miscellaneous charges, ward class restrictions

- Maternity: Antenatal, delivery, postnatal; typically 9-12 month waiting periods; often capped at ₦200,000 to ₦500,000 per pregnancy

- Dental: Basic preventive (cleaning, fillings, extractions); cosmetic and orthodontic typically excluded

- Optical: Eye examinations, frames, and lenses (subject to annual sub-limits)

- Emergency care: Accident and emergency treatment, ambulance services on higher-tier plans

- Wellness: Annual physical examinations, vaccinations, health screenings (particularly strong on Avon plans)

- Mental health: Increasingly covered as standard on mid-tier and above plans

Most Nigerian employers cover 100% of the employee premium, with dependant coverage typically a mix of employer-paid and employee-paid options. Larger employers and multinationals routinely cover dependants fully as part of competitive benefits. SMEs often offer dependant coverage as an optional payroll deduction at preferential group rates.

Other Mandatory Employer Contributions

Beyond mandatory NHIA-aligned health insurance, Nigerian employers must comply with several other statutory contributions. The complete employer cost picture includes pension, employee compensation, industrial training fund, and (for larger employers) the National Housing Fund:

| Mandatory Contribution (2026) | Employer Rate | Employee Rate | Total / Notes |

| Pension (PenCom) | 10% of monthly emolument | 8% of monthly emolument | Total 18%; minimum aggregate 18% |

| Employee Compensation (NSITF) | 1% of total payroll | 0% | Covers occupational injury and disease |

| Industrial Training Fund (ITF) | 1% of total payroll | 0% | For employers with 5+ staff or ₦50M+ turnover |

| National Housing Fund (NHF) | 0% | 2.5% of basic salary | For employees earning ₦3,000+ monthly |

| NHIA-aligned health insurance (HMO) | Plan-dependent | 0% (typically) | ₦150,000 to ₦1.94M per employee per year |

| Group life assurance | Minimum 3x annual basic salary | 0% | Mandatory under PRA 2014 |

Pension Contributions (PenCom): Under the Pension Reform Act 2014, employers and employees must contribute to a Retirement Savings Account (RSA) managed by a licensed Pension Fund Administrator (PFA). Employers contribute 10% of monthly emolument and employees contribute 8%, with a minimum total of 18%. Employers can choose to contribute the full 18% if they wish, but the 10/8 split is most common.

Group Life Assurance: Section 4(5) of the Pension Reform Act 2014 requires every employer to maintain a group life insurance policy for all employees with a minimum coverage of three times annual total emolument. Failure to maintain group life cover is an offence under the Act.

Employee Compensation (NSITF): The Employee Compensation Act 2010 requires employers to contribute 1% of total payroll to the Nigeria Social Insurance Trust Fund (NSITF), which provides benefits for work-related injuries, occupational diseases, and death in the course of employment.

Industrial Training Fund (ITF): Employers with 5 or more staff or with annual turnover above ₦50 million must contribute 1% of total annual payroll to the ITF for workforce training and development.

National Housing Fund (NHF): Employees earning ₦3,000 or more per month must contribute 2.5% of basic salary to the NHF, deducted by the employer and remitted to the Federal Mortgage Bank of Nigeria.

Total Employer Cost in Nigeria 2026

For companies hiring in Nigeria, gross salary is only the starting point. Mandatory pension contributions, NSITF, ITF, group life assurance, and NHIA-aligned health insurance add a meaningful overhead on top of gross. Below is an indicative breakdown for a worker on a ₦1,000,000 monthly gross salary (₦12 million annually), a typical mid-level professional in Lagos:

| Cost Component (2026) | Rate | Annual Cost (NGN) |

| Gross salary | — | 12,000,000 |

| Pension employer contribution (PenCom) | 10% | 1,200,000 |

| Group life assurance (3x annual salary) | ~1% of salary | ~120,000 |

| NHIA-aligned health insurance (mid-tier corporate HMO) | ₦300,000 to ₦700,000 | 300,000 to 700,000 |

| Employee Compensation (NSITF) | 1% of payroll | 120,000 |

| Industrial Training Fund (ITF) | 1% of payroll | 120,000 |

| Total fully-loaded annual cost | ~16% to 19% uplift | ~13.86M to 14.26M |

For a ₦12 million gross annual salary, the true fully-loaded employer cost in 2026 is approximately ₦13.9 million to ₦14.3 million, a 16% to 19% uplift. This excludes additional discretionary costs such as performance bonuses (commonly 1 to 3 months of salary at year-end), 13th month pay (offered by some employers as standard practice), transport allowances, housing allowances, and meal subsidies which are widespread in Lagos and Abuja corporate compensation.

The largest employer cost variable is HMO plan tier. A basic SME plan at ₦90,000 adds roughly 0.75% to total cost; a premium corporate plan at ₦1.94 million adds 16%. For senior hires and roles competing against multinationals, premium plans are essentially required for retention.

Public vs Private Healthcare in Nigeria

Nigeria operates a mixed public-private healthcare system. The public sector is funded by federal, state, and local governments and provides care through tertiary hospitals (Federal Medical Centres, teaching hospitals), state-level secondary hospitals, and primary healthcare centres. The private sector includes leading hospitals like Reddington Hospital and Lagoon Hospitals in Lagos, Cedarcrest in Abuja, and a growing network of private clinics across major cities.

Public hospitals are heavily subsidised but face significant capacity constraints, particularly outside Lagos and Abuja. Common challenges include:

- Long waiting times for non-urgent care, often exceeding several weeks

- Healthcare worker shortages (Nigeria has one of the lowest doctor-to-patient ratios in the world at approximately 1:5,000)

- Limited availability of advanced diagnostic equipment outside major cities

- Out-of-pocket payment frequently still required for medications and consumables

- Periodic disruptions due to industrial actions by medical professional associations

As a result, most working professionals and corporate employees rely on private healthcare through HMO-arranged hospital access. Private hospital costs in Lagos and Abuja are substantial without insurance: a private hospital admission can cost ₦100,000 to ₦500,000 per night for general wards, rising to ₦1 million+ per night in leading private facilities. Specialist consultations cost ₦25,000 to ₦75,000, and surgical procedures range from ₦500,000 for minor surgery to ₦10 million+ for major cardiac or oncological treatment.

For senior executives and high-net-worth professionals, international medical evacuation is increasingly common. Many top corporate plans include evacuation cover to South Africa, Dubai, India, or the UK for serious conditions requiring advanced treatment unavailable in Nigeria.

How International Companies Hire in Nigeria

For international companies hiring in Nigeria without a local entity, there are two practical options: establish a Nigerian limited liability company or use an Employer of Record (EOR).

Option 1: Establish a Nigerian limited liability company

Setting up a Nigerian limited liability company requires incorporation through the Corporate Affairs Commission (CAC), tax registration with the Federal Inland Revenue Service (FIRS) for Company Income Tax and VAT, registration with state Internal Revenue Service for Personal Income Tax (PAYE), pension scheme setup with a licensed Pension Fund Administrator, NSITF and ITF registration, NHIA enrolment with an accredited HMO, and opening a Nigerian corporate bank account. Total timeline is typically 6 to 12 weeks. Ongoing costs include accounting (₦300,000 to ₦1 million per month), audit, statutory filings, and payroll administration.

Option 2: Employer of Record (EOR)

An EOR is a Nigerian-registered entity that formally employs the worker on your behalf. The EOR handles Nigerian employment contracts, monthly PAYE withholding and remittance to relevant State Internal Revenue Services, pension contributions to a licensed PFA, NSITF/ITF/NHF compliance, NHIA-aligned HMO enrolment, group life assurance, and ongoing compliance with the Labour Act and Pension Reform Act 2014. Typical setup: 1 to 3 weeks. Typical cost: USD 400 to USD 700 per employee per month on top of gross salary, mandatory contributions, and HMO premiums.

For hiring one to ten Nigerian employees, or for 6 to 24 month projects, an EOR is almost always the faster and lower-risk option. For longer-term operations with 10+ Nigerian employees, incorporating a local entity eventually becomes more cost-effective. Most EOR providers in Nigeria offer at least one tier of HMO coverage as a standard add-on, with premium options available for senior hires.

What International Employers Need to Know

Health insurance is mandatory under the NHIA Act 2022

Any employer with 5 or more staff is legally required to enrol all employees in an NHIA-approved health insurance plan. Coverage extends to the employee, one spouse, and up to four biological children under 18. The 2026 presidential directive further requires a valid NHIA certificate for procurement, licences, and permit renewals.

Budget for ₦150,000 to ₦1.9 million per employee per year for health insurance

2026 HMO premium ranges are wide. Basic SME plans cost ₦45,000 to ₦90,000 per year. Mid-tier corporate plans cost ₦150,000 to ₦400,000. Premium and executive plans cost ₦900,000 to ₦1.94 million. Plan inflation has been significant: 8-59% increases between 2024 and 2025, with continued upward pressure expected through 2026.

Account for the full mandatory contribution stack

Beyond HMO, Nigerian employers must contribute to: PenCom pension (10% employer + 8% employee), NSITF (1% of payroll), ITF (1% of payroll, 5+ staff), group life assurance (minimum 3x annual salary), and NHF (2.5% employee deduction for those earning ₦3,000+ monthly). Total employer overhead is typically 16-19% on top of gross salary.

Choose an HMO based on hospital network and digital experience

The major HMOs (AXA Mansard, Hygeia, Avon, Leadway, Reliance) differ primarily on hospital network reach, claims processing speed, and digital platform quality. Hygeia and Avon lead on network breadth (2,000+ hospitals each); Reliance and Bastion lead on digital experience; AXA Mansard leads on financial stability and complex corporate plans.

NIN is required for every employee enrolment

A valid National Identification Number (NIN) is a hard requirement for NHIA and HMO enrolment. International employers should incorporate NIN verification into onboarding workflows to avoid delays in activating health coverage.

Consider an EOR for compliant Nigerian hiring

For international companies without a Nigerian entity, an Employer of Record handles HMO enrolment, PenCom pension setup, NSITF/ITF/NHF compliance, group life assurance, and PAYE administration automatically. See our Best EOR in Nigeria guide for verified provider rankings.

Hiring in Nigeria?

Nigerian employment law requires NHIA-aligned health insurance for any employer with 5+ staff, plus mandatory PenCom pension, NSITF, ITF, NHF, and group life assurance contributions. Navigating HMO selection, NIN-based employee enrolment, and the 2026 presidential directive on NHIA certification requires local expertise. Compare the top Employer of Record providers for Nigeria in 2026 – verified pricing, compliance scores, and expert rankings from Employsome’s independent research team.

Frequently Asked Questions

Yes. The National Health Insurance Authority (NHIA) Act 2022 made health insurance mandatory for all Nigerians and legal residents, including a specific obligation for any employer with five or more staff to enrol all employees in an NHIA-approved health insurance plan. Coverage automatically extends to the employee, one spouse, and up to four biological children under 18. A February 2026 presidential directive further requires a valid NHIA certificate for procurement, licence, and permit eligibility, significantly strengthening enforcement.

The National Health Insurance Authority (NHIA) Act 2022 was signed into law on 19 May 2022, replacing the National Health Insurance Scheme (NHIS) Act of 1999. The Act establishes the NHIA as Nigeria’s sole regulatory body for all health insurance matters, transitioning the country from voluntary to mandatory health insurance enrolment. The goal is Universal Health Coverage (UHC) by 2030. Sections 3 and 14 of the Act provide for mandatory enrolment of all Nigerians and legal residents through formal sector schemes, GIFSHIP for the informal sector, or vulnerable group programmes.

Nigerian HMO pricing varies widely by plan tier. Entry plans like AXA EasyCare cost ₦12,000 for six months. Basic SME plans cost ₦45,000 to ₦90,000 per employee per year. Mid-tier corporate plans cost ₦150,000 to ₦400,000. Premium and executive plans range from ₦400,000 to ₦1.94 million per year. The average corporate HMO plan jumped from ₦346,000 in 2024 to approximately ₦668,000 in 2025 due to drug price inflation and hospital cost increases of 8% to 59% across plan categories.

There is no single “best” HMO in Nigeria; the right choice depends on company size, employee mix, and priorities. AXA Mansard leads on financial stability and complex corporate plans (six tiers from ₦86,500 to ₦1.94 million). Hygeia HMO leads on hospital network breadth (2,000+ facilities) and 30+ years of experience. Avon HMO leads on wellness programmes for corporate clients. Reliance Health is corporate-only in 2026 with a strong digital-first platform. Bastion Health is the budget-friendly digital choice for SMEs.

Under the NHIA Act 2022, employer-provided health insurance covers the employee, one spouse, and up to four biological children under 18 as standard. Additional dependants, including extra children, parents, or other relatives, can be enrolled at extra cost. Coverage is automatic from the start of employment for the formal sector scheme. Self-employed individuals and informal sector workers can enrol through the GIFSHIP programme. Vulnerable groups (pregnant women, children, elderly, disabled persons) are covered through the Basic Health Care Provision Fund (BHCPF).

Beyond NHIA-aligned health insurance, Nigerian employers must contribute to: PenCom pension (10% employer + 8% employee, total 18%), NSITF Employee Compensation (1% of total payroll), Industrial Training Fund (1% of payroll for employers with 5+ staff or ₦50M+ turnover), and group life assurance (minimum 3x annual basic salary, mandatory under the Pension Reform Act 2014). Employees earning ₦3,000+ monthly also contribute 2.5% to the National Housing Fund. Total employer overhead is typically 16-19% on top of gross salary.

Health Maintenance Organisations (HMOs) are NHIA-accredited Third Party Administrators (TPAs) that handle employer registrations, employee enrolment, hospital network access, claims processing, and premium administration on behalf of clients. Under the NHIA Act 2022, HMOs no longer have direct fund management authority (which sits with State Health Insurance Schemes). HMOs may collect premiums on behalf of SHIS where appointed, but pooled funds must be remitted to the SHIS for management and investment through the NHIA. There are over 70 NHIA-accredited HMOs operating nationwide.

In most Nigerian employer-provided HMO arrangements, the employer covers 100% of the employee premium. Dependant coverage is often a mix: many large employers and multinationals cover dependants fully as part of competitive benefits, while SMEs may offer dependant coverage as an optional payroll deduction at preferential group rates. This contrasts with many other countries where employees co-pay a percentage of premiums. The NHIA scheme itself was historically funded entirely by employers (mainly the federal government for public sector), with no counterpart contribution from employees.

Nigerian HMO premiums rose 8% to 59% between 2024 and 2025 due to several converging factors: rising drug prices driven by import cost inflation following naira devaluation, surging hospital tariffs as private facilities passed cost increases through to HMOs, soaring costs of medical consumables and equipment, energy and operational cost increases at hospitals, and a deteriorating macroeconomic environment generally. Industry experts expect continued upward pressure through 2026. International employers should build 10-15% annual HMO premium inflation into multi-year compensation budgets.

An Employer of Record (EOR) handles all Nigerian employer insurance and benefits compliance on behalf of international clients. The EOR registers the company with the NHIA, enrols employees with an accredited HMO, manages PenCom pension contributions to a licensed Pension Fund Administrator, handles NSITF/ITF/NHF compliance, maintains group life assurance, and ensures monthly PAYE remittance. For companies hiring 1-10 Nigerian employees without a local entity, an EOR is almost always faster and more cost-effective than incorporating a Nigerian company. See our Best EOR in Nigeria guide for provider rankings.

Copywriter

Christa is a Copywriter at Employsome with 17 years of professional writing experience across global brands, startups, and online publications. A native English-Finnish writer, she brings strong editorial skills and a versatile background in business, SaaS, and finance. At Employsome, Christa focuses on clear, practical content about HR, payroll, and Employer of Record topics.

Our content is created for informational purposes only and is not intended to provide any legal, tax, accounting, or financial advice. Please obtain separate advice from industry-specific professionals who may better understand your business’s needs. Read our Editorial Guidelines for further information on how our content is created.