CPF Singapore: How It Works & What Changed in 2026

Singapore’s Central Provident Fund requires employers to contribute 17% of wages on top of salary for employees under 55, with a combined employer-employee rate of 37%. From January 2026, the Ordinary Wage ceiling rose to S$8,000/month and contribution rates for workers aged 55 to 65 increased by 1.5 percentage points. This guide covers how the three CPF accounts work (OA, SA, MediSave), the full 2026 rate table by age bracket, the wage ceiling calculations with worked examples, why foreign employees pay zero CPF (but may trigger the Foreign Worker Levy), and what companies hiring through an EOR in Singapore need to verify in their payroll.

The Central Provident Fund is the thing that makes hiring in Singapore more expensive than the salary number suggests. If you are a foreign company hiring Singaporean citizens or permanent residents, CPF is not optional. It is a mandatory savings scheme that requires the employer to contribute 17% of the employee’s wages on top of salary, while the employee contributes 20% from their pay. That is a combined 37% of wages going into CPF accounts every month for workers under 55.

For international companies used to employer social security rates of 13-15% in many markets, Singapore’s 17% employer rate is not the highest in the world, but it is higher than people expect from a jurisdiction with no capital gains tax, no inheritance tax, and a top personal income tax rate of just 24%. The CPF is effectively Singapore’s entire social safety net rolled into one system: retirement savings, healthcare, housing, and insurance, all funded through payroll.

This guide explains what CPF is, how the three accounts work, the current contribution rates (including the January 2026 changes for older workers), the wage ceilings, what happens with foreign employees, and what international companies hiring through an EOR in Singapore need to get right.

What Is CPF?

The Central Provident Fund is a compulsory savings and pension scheme for all working Singaporean citizens and permanent residents. It was established in 1955 and has been expanded multiple times since then. Today it covers retirement income, healthcare expenses, housing purchases, insurance, and education. The 2025 Mercer Global Pension Index ranked Singapore’s CPF system 5th in the world and gave it an A grade for the first time, the highest in Asia.

CPF is not a tax. The money goes into individual accounts belonging to the employee, not into a government revenue pool. Employees can see their balances, track their contributions, and eventually withdraw their savings (subject to age and minimum balance requirements). From the employer’s perspective, though, it functions exactly like a payroll tax: you calculate it, deduct the employee’s share from their pay, add your own share, and remit the total to the CPF Board by the last day of each month.

CPF applies only to Singapore Citizens and Permanent Residents. It does not apply to foreigners on Employment Passes, S Passes, or Work Permits. This is a critical distinction for international companies: if you hire a Singaporean, CPF adds 17% to your employment cost. If you hire a foreigner on an EP, it adds zero (though you may owe the Foreign Worker Levy or Skills Development Levy instead, depending on the pass type).

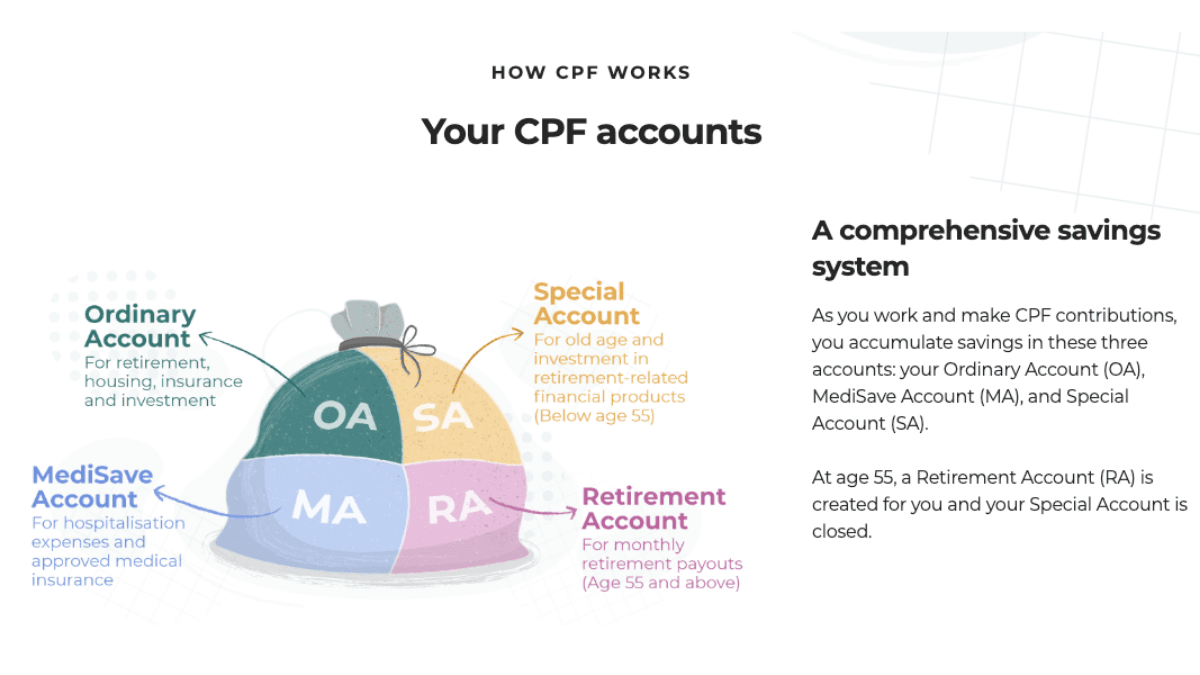

The Three CPF Accounts

Every CPF member has three accounts, and the contributions are split between them according to the member’s age. Understanding the split matters because it affects what the employee can use the money for:

|

Account |

Purpose |

Interest Rate |

|

Ordinary Account (OA) |

Housing (HDB flat purchases, mortgage payments), CPF-approved investments, education, insurance premiums |

2.5% per annum (floor rate) |

|

Special Account (SA) |

Retirement savings and retirement-related investments only. Closed at age 55, balance transferred to RA. |

4% per annum (floor rate) |

|

MediSave Account (MA) |

Healthcare expenses, hospitalisation, MediShield Life premiums, approved medical insurance |

4% per annum (floor rate) |

At age 55, a fourth account is created: the Retirement Account (RA). The Special Account is closed, and its balance (plus any OA savings the member chooses to transfer) goes into the RA. The RA is the source of the member’s retirement income through CPF LIFE, which is Singapore’s national annuity scheme.

For employers, the account split does not change your contribution calculation. You pay a flat percentage based on the employee’s age and wages. The CPF Board handles the allocation across accounts automatically.

CPF Contribution Rates (2026)

The rates below apply from 1 January 2026 for Singapore Citizens and Permanent Residents (from their third year of PR status onward) earning more than S$750 per month:

|

Employee Age |

Employer Rate |

Employee Rate |

Total |

|

55 and below |

17% |

20% |

37% |

|

Above 55 to 60 |

16% (+0.5%) |

18% (+1%) |

34% (+1.5%) |

|

Above 60 to 65 |

12.5% (+0.5%) |

12.5% (+1%) |

25% (+1.5%) |

|

Above 65 to 70 |

9% |

7.5% |

16.5% |

|

Above 70 |

7.5% |

5% |

12.5% |

The figures in brackets show the increases from 2025 to 2026. The key change is that workers aged 55 to 65 now contribute more, with the extra contributions going entirely into the Retirement Account to strengthen retirement adequacy. For employers, this means a 0.5 percentage point increase in employer cost for employees in these age brackets.

For employees earning between S$500 and S$750 per month, the employee contribution rates are phased in gradually while the employer rate remains the same. Below S$500, no CPF contributions are required.

First and second year Permanent Residents have graduated rates that are lower than the full rates. The employer and employee can jointly apply to contribute at the full rates if they choose.

The Wage Ceiling: S$8,000 from 2026

CPF contributions are not calculated on unlimited earnings. There are two ceilings that cap the amount of wages subject to CPF:

|

Ceiling |

Amount (2026) |

|

Ordinary Wage (OW) ceiling |

S$8,000/month (up from S$7,400 in 2025) |

|

Additional Wage (AW) ceiling |

S$102,000/year (unchanged) |

The OW ceiling is the monthly cap. If an employee earns S$12,000 per month, CPF is calculated only on the first S$8,000. The employer pays 17% of S$8,000 = S$1,360, not 17% of S$12,000. This cap means that for high earners, CPF is a decreasing percentage of total compensation.

The AW ceiling covers bonuses, commissions, and other non-monthly payments. The formula is: AW ceiling = S$102,000 minus total ordinary wages for the year. If an employee earns S$8,000/month (S$96,000/year in OW), the AW ceiling is S$102,000 minus S$96,000 = S$6,000. CPF on any bonus is calculated only up to this remaining amount.

The increase from S$7,400 to S$8,000 in the OW ceiling is a significant change for employers. For every employee under 55 earning at least S$8,000/month, the employer’s maximum monthly CPF contribution rose from S$1,258 (17% of S$7,400) to S$1,360 (17% of S$8,000), an increase of S$102/month or S$1,224/year per employee.

💡 Employsome Insight: The OW Ceiling Increase Hits Mid-Level Salaries Hardest

The companies most affected by the S$8,000 OW ceiling are those with large numbers of employees earning between S$7,400 and S$8,000 per month. Before January 2026, CPF on an S$8,000 salary was capped at S$7,400. Now the full S$8,000 is subject to CPF. For a team of 20 such employees, the additional employer cost is S$2,040/month or S$24,480/year. If you are budgeting for Singapore hires through an EOR, make sure the payroll reflects the new ceiling.

Foreign Employees: No CPF, But Other Levies Apply

CPF does not apply to foreign employees. If your hire holds an Employment Pass, S Pass, or Work Permit, there is no CPF obligation for either the employer or the employee. This is one of the reasons Singapore is attractive for hiring foreign talent: the employer cost is the gross salary plus any benefits, with no mandatory social security contribution on top.

However, foreign employees may be subject to other levies depending on their pass type. S Pass and Work Permit holders require the employer to pay a Foreign Worker Levy (FWL), which varies by sector and can be significant (S$300 to S$950/month depending on the tier and industry). Employment Pass holders are not subject to the FWL.

All employers (for all employees, including foreign ones) must pay the Skills Development Levy (SDL) of 0.25% of monthly wages, with a minimum of S$2 and a maximum of S$11.25 per employee per month. This is a small cost but one that international companies sometimes overlook.

The practical implication: hiring a Singaporean citizen costs 17% more than the gross salary in CPF alone. Hiring a foreigner on an EP costs roughly S$11.25/month in SDL and nothing else in mandatory contributions. This creates a significant cost differential that affects hiring decisions, particularly for roles where both local and foreign candidates are available.

How CPF Works in Practice for Employers

The employer is responsible for the entire CPF process: calculating both the employer and employee shares, deducting the employee’s share from their monthly pay, adding the employer’s share, and remitting the combined amount to the CPF Board by the last day of each calendar month. Late payment attracts interest at 1.5% per month and potential composition amounts (fines) of up to S$1,000 per offence.

Payments are made through the CPF Board’s online portal using SingPass/CorpPass authentication. Employers submit a CPF PAL file (a standardised text file) generated from their payroll software. Most modern payroll systems in Singapore can generate this file automatically.

One detail that catches foreign companies: CPF contributions are calculated on gross wages including overtime, allowances, commissions, bonuses (up to the AW ceiling), and other regular payments. The only common exclusions are reimbursements of genuine business expenses and certain one-off ex-gratia payments. If in doubt, the CPF Board’s guidelines specify exactly which payment types are subject to CPF.

CPF and Employer of Record Arrangements

When you hire a Singaporean citizen or PR through an EOR, the EOR is the legal employer and handles all CPF obligations: calculation, deduction, remittance, and filing. The employer’s 17% CPF contribution (for employees under 55) is included in the total employment cost that the EOR invoices to the client.

Key questions to ask your EOR about CPF in Singapore: has the payroll been updated to reflect the S$8,000 OW ceiling from January 2026? Are the increased rates for employees aged 55 to 65 applied correctly? How does the EOR handle the AW ceiling calculation for bonuses? Is the SDL included in the invoice or charged separately? Does the EOR provide employees with access to their CPF contribution statements?

CPF compliance is generally straightforward in Singapore because the system is well-documented and the CPF Board provides clear guidelines and calculators. The main risk for EOR clients is not complexity but accuracy: the wrong age bracket, an outdated ceiling, or a miscalculated bonus can trigger penalties and erode employee trust. Singapore is Multiplier’s home market and a strength for most APAC-focused EOR providers, so CPF handling should be reliable, but verify the 2026 changes are reflected.

When Can Employees Access Their CPF?

specific conditions. The Ordinary Account can be used at any age for housing purchases (HDB flats and approved private properties), approved investments, education expenses, and insurance premiums. The MediSave Account can be used at any time for approved healthcare expenses and insurance.

The retirement-specific savings (Special Account and later Retirement Account) become accessible from age 55. At 55, the member can withdraw any amount above the Full Retirement Sum (FRS), which in 2026 is S$213,000. The FRS must remain in the Retirement Account to fund CPF LIFE payouts starting from age 65, which provide monthly income for life.

For employers, the withdrawal rules do not directly affect payroll or CPF contributions. But they are relevant context when discussing compensation with Singaporean employees, because CPF savings are a significant part of their total financial picture. A Singaporean employee earning S$6,000/month has S$2,220/month (37% combined) going into CPF, which over a career accumulates into substantial housing equity and retirement savings. This is why many Singaporeans view CPF as part of their compensation, not as a deduction.

Hiring in Singapore?

Singapore’s CPF system, combined with the Skills Development Levy and Foreign Worker Levy, adds significant employer costs that vary dramatically depending on whether you hire citizens, PRs, or foreigners. Compare the best EOR providers for Singapore on Employsome. We score each provider on CPF accuracy, payroll compliance, and local expertise. Visit our guide to see the full comparison.

Frequently Asked Questions

The Central Provident Fund is a mandatory savings scheme for Singaporean citizens and permanent residents. Both employer (17%) and employee (20%) contribute a percentage of wages to fund retirement, healthcare, housing, and insurance. Ranked 5th globally by the 2025 Mercer Pension Index.

17% of wages for employees aged 55 and below (2026 rates). The rate decreases for older employees: 16% for 55-60, 12.5% for 60-65, 9% for 65-70, and 7.5% for over 70. Contributions are capped at the Ordinary Wage ceiling of S$8,000/month.

No. CPF applies only to Singapore Citizens and Permanent Residents. Foreigners on Employment Passes, S Passes, and Work Permits do not contribute to or receive CPF. However, S Pass and Work Permit holders may require the employer to pay a Foreign Worker Levy.

The Ordinary Wage ceiling increased from S$7,400 to S$8,000/month. CPF contribution rates for employees aged 55 to 65 increased by 1.5 percentage points total (0.5% employer, 1% employee). The extra contributions for older workers go into the Retirement Account.

S$8,000/month for Ordinary Wages (from January 2026). The Additional Wage ceiling is S$102,000/year. Wages above these amounts are not subject to CPF contributions. For high earners, this means CPF is effectively a flat dollar amount rather than a percentage of total pay.

Late payment interest of 1.5% per month on the outstanding amount. The CPF Board may also impose composition amounts (fines) of up to S$1,000 per offence. Persistent non-compliance can lead to prosecution with fines of S$1,000 to S$5,000 and up to 6 months’ imprisonment for first offences.

Yes. CPF applies to all Singapore Citizens and PRs regardless of whether they are full-time or part-time. The rates and calculation method are the same. The only distinction is the wage threshold: no CPF is required below S$50/month, and reduced employee rates apply between S$500 and S$750/month.

Written by

Dane Cobain is a Copywriter at Employsome and an accomplished author whose work spans fiction, non-fiction, and professional writing. Over the past decade, he has built a strong track record creating straightforward content for the HR, payroll, and corporate sectors. Dane brings a storyteller’s eye to the evolving world of global employment, with a particular focus on Employer of Record and PEO models. His articles explore industry trends and dedicated Best Of Guides when managing an international workforce.

Our content is created for informational purposes only and is not intended to provide any legal, tax, accounting, or financial advice. Please obtain separate advice from industry-specific professionals who may better understand your business’s needs. Read our Editorial Guidelines for further information on how our content is created.

Other posts

Review other blog posts