Average Salary in the Netherlands 2026: By Sector, City & Role

The average salary in the Netherlands in 2026 is €53,436 gross per year (€4,453 per month including holiday allowance), with a modal income of €48,000. This complete guide breaks down Dutch salaries by sector, city, age, education, and role, covers tax brackets and the 30% ruling, and details the full employer cost of hiring a Dutch employee in 2026.

The average salary in the Netherlands is €53,436 gross per year in 2026, equivalent to €4,453 per month including the mandatory 8% holiday allowance, according to the latest figures from the Centraal Bureau voor de Statistiek (CBS) combined with estimated CAO wage growth. The modal income, set by the Centraal Planbureau (CPB), is €48,000 gross per year. Net take-home pay on the modal salary averages €3,100 to €3,200 per month after income tax, social insurance premiums, and pension contributions.

These national averages hide substantial variation. Software engineers in Amsterdam earn €65,000 to €130,000 per year, financial services professionals in Tier-1 cities average €72,000, while hospitality workers in rural regions earn closer to €32,000 annually. Total employer cost adds approximately 28% on top of gross salary once mandatory social contributions, pension premiums, and the statutory 8% holiday allowance are included.

This 2026 guide to the average salary in the Netherlands covers gross and net pay levels, salaries by sector and city, regional variations, how the mandatory holiday allowance and 13th month payment work, total employer cost calculations, the 2026 tax brackets, the 30% ruling for international hires, and what companies hiring through an Employer of Record (EOR) need to budget when expanding into the Netherlands.

Average Salary in the Netherlands 2026: The Headline Numbers

The Dutch labour market distinguishes between three different salary figures, and understanding the difference is critical when benchmarking compensation. Most job offers and salary surveys reference one of these three numbers without always clarifying which.

| Salary Metric (2026) | Amount (EUR) | Monthly Equivalent |

| Average gross annual salary | €53,436 | €4,453 (inc. holiday allowance) |

| Modal income 2026 (CPB) | €48,000 | €3,700-4,000 |

| Median annual income | €43,500 | €3,625 |

| Statutory minimum wage (21+) | €30,500 (40h/week) | €2,550 + holiday allowance |

| Minimum hourly wage | €14.71/hour | — |

| Average net monthly income | €37,300 (net annual) | €3,100-3,200 |

The average salary (€53,436) is total wages divided by workers, and is pulled upwards by high earners in finance, technology, and executive roles. It is the figure cited most often by CBS and in employer cost calculations, but it overstates what a typical Dutch worker actually earns.

The modal income (€48,000) is the most commonly earned salary, set annually by the CPB in the Macro Economische Verkenning. This is the best single figure for benchmarking what a typical full-time Dutch professional earns. The CPB raised the modal figure from €46,500 in 2025 to €48,000 in 2026 as part of standard inflation indexation.

The median income (€43,500, based on CBS 2023 data adjusted for CAO growth) is the exact middle value. It is lower than both average and modal because many Dutch workers are part-time or near the minimum wage, which pulls the midpoint down.

Dutch CAO (collective labour agreement) wages rose 4.8% in 2025 and are forecast to rise a further 4.1% in 2026 based on the Loonindex Q1 2026 from Van Spaendonck. These above-inflation increases reflect a tight labour market with unemployment at 3.9% and persistent skills shortages in technology, healthcare, and engineering.

💡 Employsome Insight: Modal Income Is a Better Benchmark Than Average Salary

For most compensation benchmarking in the Netherlands, the modal income of €48,000 is the most useful reference. It represents what a typical full-time Dutch worker earns without being inflated by executives or CEO pay. The headline “average” of €53,436 is technically accurate but consistently leads international companies to underpay, because they benchmark against the midpoint of a distribution their target candidate is likely below. For senior technology or finance roles, reference sector-specific data (see next section) rather than the national average.

Netherlands Salaries by Sector and Role

Sector has the largest single impact on salary in the Netherlands, larger than age, experience, or education once role is held constant. Mining, financial services, and technology pay roughly double what hospitality and retail pay. Here is how gross annual salaries break down across the major Dutch sectors in 2026:

| Sector | Average Gross Annual Salary | Relative to National Average |

| Mining and energy extraction | €78,000+ | +45% |

| Financial services and insurance | €72,000 | +35% |

| Information and communication (IT) | €65,000 | +22% |

| Utilities (gas, electricity, water) | €62,000 | +16% |

| Public administration and government | €58,000 | +9% |

| Education | €55,000 | +3% |

| Healthcare and social services | €48,000 | -10% |

| Manufacturing | €46,000 | -14% |

| Construction | €45,000 | -16% |

| Transport and logistics | €42,000 | -21% |

| Retail and wholesale | €38,000 | -29% |

| Hospitality and food service | €32,000 | -40% |

Dutch tech salaries have diverged significantly from the national average over the past three years, particularly at international firms with Amsterdam offices. Senior software engineers at scale-ups and multinationals routinely earn €95,000 to €130,000 per year plus equity, while Dutch-domestic software developers at SMEs earn closer to the €65,000 sector average. Specific role benchmarks:

| Role | Junior | Mid-level | Senior |

| Software engineer | €45,000 | €65,000 | €95,000 – €130,000+ |

| Data scientist | €48,000 | €70,000 | €100,000 – €140,000 |

| Product manager | €50,000 | €75,000 | €110,000+ |

| Marketing manager | €40,000 | €58,000 | €80,000 – €110,000 |

| Financial analyst | €42,000 | €62,000 | €90,000 – €120,000 |

| HR business partner | €38,000 | €56,000 | €75,000 – €95,000 |

| Mechanical engineer | €40,000 | €58,000 | €78,000 – €95,000 |

| Accountant | €36,000 | €52,000 | €72,000 – €90,000 |

| Registered nurse | €32,000 | €42,000 | €55,000 |

| Teacher (secondary, 1st grade) | €38,500 | €52,000 | €68,000 |

Sector is the single biggest determinant of salary in the Netherlands, with a roughly €46,000 gap between the highest-paying industry (mining and energy extraction at €78,000) and the lowest (hospitality and food service at €32,000). The chart below visualises how Dutch sectors rank on average gross annual salary in 2026, grouped into three tiers: the top-paying sectors dominated by mining, finance, and IT; a mid-range cluster covering utilities, government, education, and healthcare; and the lower-paying services and retail sectors.

Netherlands Salaries by City and Region

Geography has a material effect on Dutch salaries. Amsterdam, Eindhoven, and Utrecht pay meaningfully more than smaller cities and rural regions, reflecting concentrations of international companies, technology firms, and financial institutions. However, the Amsterdam premium is partially offset by the highest housing costs in the country.

| City | Average Gross Annual Salary | Key Industries |

| Amsterdam | €56,000 | Finance, technology, professional services |

| Eindhoven | €54,000 | Technology (Philips, ASML), semiconductors, R&D |

| The Hague (Den Haag) | €52,000 | Government, NGOs, international organisations |

| Utrecht | €51,000 | Professional services, healthcare, research |

| Rotterdam | €48,000 | Port, logistics, engineering, energy |

| Haarlem | €47,000 | Services, commuter hub for Amsterdam |

| Groningen | €42,000 | Energy, healthcare, education |

| Maastricht | €41,000 | Healthcare, international services |

| Arnhem | €40,000 | Energy, business services |

| Tilburg | €39,000 | Logistics, manufacturing, education |

The Amsterdam premium of roughly 20% above the national average reflects the city’s position as the economic centre of the Netherlands. Finance, technology, and professional services concentrate there, and international companies opening a Dutch office almost always pick Amsterdam or Utrecht. However, Amsterdam rent for a one-bedroom apartment averages €1,800 to €2,500 per month, which is 40-60% higher than equivalent housing in Utrecht or Eindhoven, meaningfully reducing the effective premium.

For international employers hiring Dutch talent remotely, the regional variation creates sourcing opportunities. A senior developer in Groningen or Maastricht will often accept 70-80% of an Amsterdam salary for a fully remote role while delivering identical output. This is why distributed engineering teams increasingly recruit beyond the Randstad.

Average Salary by Age and Education Level

Age is the second-largest predictor of Dutch salary after sector, reflecting experience, seniority, and Dutch collective labour agreements (CAOs) that often include age-based pay scales. Salary peaks in the 45-54 age range, with a slight decline afterwards as workers enter early retirement or reduce hours.

| Age Group | Average Gross Annual Income |

| 15 to 24 | €19,200 |

| 25 to 34 | €42,500 |

| 35 to 44 | €57,800 |

| 45 to 54 | €72,100 (peak) |

| 55 to 64 | €68,400 |

| 65+ | €41,200 |

Educational attainment is the other strong salary predictor. University graduates (HBO or WO) earn nearly double what vocational-track workers earn. The spread is particularly pronounced in technology, finance, and consulting where WO-level qualifications are often a hard requirement.

| Education Level | Average Gross Annual Salary |

| VMBO / HAVO-VWO lower / MBO level 1 | €27,100 |

| HAVO / VWO / MBO level 2-4 | €36,930 |

| HBO (applied sciences bachelor) | €51,800 |

| WO (research university bachelor) | €59,520 |

| Master’s degree (WO) | €65,000 – €72,000 |

Moving from MBO to HBO adds roughly 30% to expected lifetime earnings. A WO master’s degree adds around 60% compared to MBO. These differentials are among the highest in Europe, reflecting a Dutch labour market that formally credentials professional roles through specific educational pathways.

Holiday Allowance and 13th Month Explained

Dutch salaries quoted in job offers usually exclude the 8% holiday allowance and any 13th month payment, which means the total gross annual compensation is higher than the headline monthly figure suggests. This catches out many international employers and candidates.

| Annual Compensation Component | Example (€48,000 base salary) |

| 12 monthly salaries (base) | €48,000 |

| Holiday allowance (vakantiegeld, 8%) | €3,840 |

| 13th month (if applicable, ~40% of workers) | €4,000 |

| Total gross annual compensation | €51,840 to €55,840 |

Holiday allowance (vakantiegeld): Every Dutch employee is entitled by law to a holiday allowance of at least 8% of gross annual salary. It is paid in a lump sum in May in most sectors, though some employers spread it across monthly payments. A €48,000 base becomes €51,840 once holiday allowance is included.

13th month (dertiende maand): Approximately 40% of Dutch workers receive a 13th month payment, typically in November or December. Unlike holiday allowance, it is not statutory but is commonly written into CAOs for banking, utilities, and government. Where applicable, it equals one additional month of base salary, effectively an 8.33% annual bonus.

When negotiating a Dutch offer, always clarify whether the quoted annual figure includes both components. A job advertised at “€48,000 per year” means very different total compensation depending on whether holiday allowance and 13th month are included or excluded.

Netherlands Income Tax Brackets 2026

The Netherlands applies a progressive three-bracket income tax system in Box 1 (income from employment and home ownership). The brackets for 2026 are:

| Bracket | Annual income | Tax rate 2026 |

| Bracket 1 | Up to €38,883 | 35.75% |

| Bracket 2 | €38,883 to €78,426 | 37.56% |

| Bracket 3 | Above €78,426 | 49.50% |

The first bracket rate includes both income tax and national insurance premiums (volksverzekeringen) for old-age pension (AOW), surviving dependents (Anw), and long-term care (Wlz). Workers above the AOW state pension age pay only 17.85% in the first bracket because they no longer contribute to AOW premiums. The rates are progressive: someone earning €50,000 pays 35.75% on the first €38,883 and 37.56% only on the remaining €11,117.

For a modal-income worker earning €48,000, the tax and social premium burden is approximately €14,000 to €15,000 per year, leaving net annual income of around €33,500 to €34,500 before holiday allowance. Including holiday allowance, total net annual income rises to approximately €36,800 to €37,800 (€3,100 to €3,200 per month).

2026 changes: The Belastingdienst adjusted the bracket limits upward slightly and fine-tuned the rates (Bracket 1 decreased from 35.82% to 35.75%, Bracket 2 increased from 37.48% to 37.56%). The top rate of 49.50% remained unchanged. The general tax credit (algemene heffingskorting) was raised to €3,115 for 2026.

💡 Employsome Insight: The 30% Ruling Is the Most Valuable Tax Benefit for International Hires

The 30% ruling is the single most valuable tax benefit for international hires in the Netherlands. Foreign workers recruited from abroad for specialised roles can receive 30% of their gross salary tax-free to cover extraterritorial costs, effectively reducing taxable income. The 2026 minimum taxable salary threshold is €46,107 (€35,048 for workers under 30 with a Master’s degree). The ruling lasts up to 5 years from first employment. A €80,000 salary with the 30% ruling has a taxable income of €56,000, shifting the worker entirely into the lower two brackets and generating significant annual tax savings. For companies hiring international talent in the Netherlands, EOR providers routinely handle 30% ruling applications as part of onboarding.

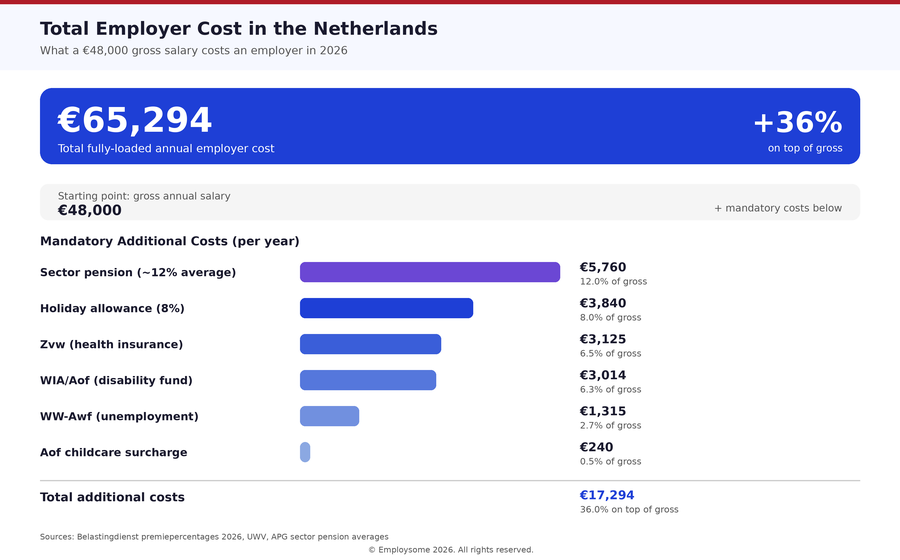

Total Employer Cost in the Netherlands 2026

For companies hiring in the Netherlands, gross salary is only the starting point. Mandatory employer social contributions, pension premiums, holiday allowance, and additional charges add approximately 28% on top of gross, reaching roughly 36% when pension at the higher end of the sector range is included.

| Employer Contribution | Rate | Annual cost on €48,000 gross |

| Holiday allowance (8%) | 8.00% | €3,840 |

| WW-Awf (unemployment insurance) | 2.74% | €1,315 |

| WIA/Aof (disability fund) | 6.28% | €3,014 |

| Aof childcare surcharge | 0.50% | €240 |

| Zvw (health insurance contribution) | 6.51% | €3,125 |

| Sector pension (average) | 10% to 15% | €4,800 to €7,200 |

| Total employer cost | ~28% to 36% | €64,300 to €66,700 |

For a €48,000 gross salary, the true fully-loaded cost to the employer is approximately €65,000 per year. This excludes additional common costs such as workspace, equipment, training, lease vehicles, meal vouchers (if applicable), and employer-provided benefits like phone allowances or commuting reimbursements.

Pension premium rates vary by sector. Some industries (banking, government, healthcare) have mandatory pension funds with higher contribution rates of 13-15%. Other sectors (retail, hospitality) often have lower rates of 8-10% or no mandatory sector fund at all. Check the relevant CAO or sector pension fund (such as ABP for government, PFZW for healthcare, PMT for metal) for the exact rate applicable to a new hire.

How International Companies Hire in the Netherlands

For international companies hiring in the Netherlands without a local entity, there are two practical options: set up a Dutch BV (private limited company) or use an Employer of Record (EOR).

Option 1: Dutch BV (Besloten Vennootschap)

Forming a Dutch BV requires notarial incorporation, KvK registration, a Dutch business bank account, tax registration with the Belastingdienst, and payroll registration. Minimum timeline is 6 to 12 weeks. Ongoing costs include Dutch accounting (€400 to €800 per month), corporate tax filings, mandatory annual accounts, and payroll administration (€80 to €150 per employee per month). This option is cost-effective for companies planning to hire five or more Dutch employees over several years.

Option 2: Employer of Record (EOR)

An EOR is a Dutch-registered entity that formally employs the worker on your behalf. The EOR handles Dutch employment contracts in the local language, payroll tax withholding, social security contributions, Zvw health insurance enrolment, pension registration, and the statutory holiday allowance. The worker reports to you day-to-day while the EOR is the legal employer. Typical setup: 2 to 4 weeks. Typical cost: €400 to €700 per employee per month on top of gross salary and employer contributions.

For hiring one to five Dutch employees, or for 6 to 24 month projects, an EOR is almost always the faster and cheaper option. For longer-term operations or larger teams, incorporating a BV eventually becomes more economical. Many companies use an EOR to start and transition to a BV once they have 5+ permanent Dutch employees.

What International Employers Need to Know

Benchmark against modal income, not average salary

The €53,436 headline average is pulled upward by a small number of high earners. For benchmarking mid-level professional roles, use the €48,000 modal income as the reference point. For senior technology or finance roles, reference sector-specific data and expect Amsterdam salaries to run 15-25% higher than the national average at international firms.

Always clarify whether salary figures include holiday allowance

Dutch salaries quoted in offers typically exclude the 8% holiday allowance. A €48,000 base becomes €51,840 total gross once holiday allowance is added, and potentially €55,840 if a 13th month payment applies. This 8-16% difference matters for compensation negotiations and compensation comparisons against other markets.

Use the 30% ruling to compete for international talent

For highly skilled migrants recruited from abroad, the 30% ruling can dramatically improve net take-home pay and strengthen Dutch offers against Berlin, Dublin, or London competitors. The €46,107 taxable threshold (€35,048 for under-30 Master’s holders) is the entry point. Most EOR providers handle the application as part of onboarding.

Budget 28-36% above gross for total employer cost

Employer social contributions (approximately 16% for WW-Awf, WIA/Aof, Zvw), mandatory 8% holiday allowance, and sector pension (10-15%) add 28-36% on top of gross salary. A €48,000 gross role costs the employer approximately €65,000 per year all-in, before workspace, equipment, and optional benefits.

Consider whether to incorporate a BV or use an EOR

For hiring one to five Dutch employees or projects under 24 months, an EOR is almost always faster and cheaper than forming a Dutch BV. Crossover point is typically 5-10 permanent Dutch employees, at which point BV incorporation becomes more cost-effective.

Monitor CAO wage growth and adjust budgets annually

Dutch CAO wages rose 4.8% in 2025 and are forecast to rise 4.1% in 2026. These above-inflation increases mean compensation budgets set more than 12 months ago are likely below market rate. Review benchmarks at least annually, and more frequently for competitive roles in technology and finance.

Hiring in the Netherlands?

The Dutch salary structure includes mandatory 8% holiday allowance and 28-36% employer contributions on top of gross wages. Navigating CAO wage tables, pension fund enrolment, and the 30% ruling for international hires requires local expertise. Compare the top Employer of Record providers for the Netherlands in 2026 – verified pricing, compliance scores, and expert rankings from Employsome’s independent research team.

Frequently Asked Questions

The average gross annual salary in the Netherlands in 2026 is €53,436 (€4,453 per month including the mandatory 8% holiday allowance), according to CBS figures combined with estimated CAO wage growth of 4.1% for 2026. The modal income, set by the CPB, is €48,000 gross per year. The median annual income is €43,500. Net take-home pay on the modal salary averages €3,100 to €3,200 per month after income tax, social insurance premiums, and pension contributions.

Average salary (€53,436) is total wages divided by workers, pulled upward by high earners. Modal income (€48,000) is the most commonly earned salary, set annually by the CPB, and the best benchmark for what a typical Dutch worker earns. Median income (€43,500) is the exact middle value, lower than both because many Dutch workers are part-time. For benchmarking mid-level professional roles, the €48,000 modal income is the most useful reference.

€3,500 net per month is above the Dutch average net income (€3,100-3,200) and comfortable for most regions outside Amsterdam. In Amsterdam, where housing costs are significantly higher, €3,500 net is adequate but not luxurious. €3,500 net roughly equates to a gross salary of €55,000 to €60,000 per year depending on tax credits and 30% ruling status. For a single professional in the Netherlands, this represents a good professional salary.

The 30% ruling is a Dutch tax benefit for highly skilled migrants recruited from abroad. Up to 30% of gross salary can be paid tax-free to cover extraterritorial costs, effectively reducing taxable income. The minimum taxable salary threshold in 2026 is €46,107 (€35,048 for workers under 30 with a Master’s degree). The ruling lasts up to 5 years from first employment date and shifts taxable income out of the highest tax brackets, generating significant annual savings.

The statutory minimum wage for workers aged 21 and over is €14.71 per hour as of 1 January 2026, one of the highest minimum wages in Europe. At full-time (40 hours per week), this equals approximately €2,550 gross per month before holiday allowance, or €2,755 including the 8% holiday allowance. For younger workers, reduced rates apply on a sliding scale down to €4.41 per hour at age 15. The rate is adjusted twice per year on 1 January and 1 July to reflect inflation.

On the €48,000 modal income, approximately €14,000 to €15,000 goes to income tax, national insurance premiums, and social contributions, leaving net annual income of roughly €33,500 to €34,500 before holiday allowance. Including the 8% holiday allowance, total net annual income rises to €36,800 to €37,800 (€3,100-3,200 per month). The exact figure depends on pension premiums, tax credits (algemene heffingskorting, arbeidskorting), and whether the 30% ruling applies.

Amsterdam has the highest average gross annual salary at approximately €56,000, followed by Eindhoven (€54,000), The Hague (€52,000), and Utrecht (€51,000). Amsterdam’s premium reflects concentrations of international companies, finance, and technology firms, though it is partially offset by the city’s significantly higher housing costs. One-bedroom apartment rent in Amsterdam averages €1,800-2,500 per month, compared to €1,200-1,600 in Utrecht or Eindhoven.

Total employer cost in the Netherlands adds approximately 28-36% on top of gross salary: 8% holiday allowance, 6.51% Zvw health insurance contribution, WW-Awf unemployment (2.74%), Aof disability fund (6.28%), Aof childcare surcharge (0.50%), and sector pension (typically 10-15%). For a €48,000 gross salary, total employer cost is approximately €64,300 to €66,700 per year. This excludes additional costs like workspace, equipment, and employer-provided benefits such as lease cars or meal vouchers.

Quoted annual salaries in the Netherlands usually exclude the 8% holiday allowance, which is paid separately as a lump sum in May. When comparing offers, always ask whether the figure is with or without holiday allowance. A €48,000 base salary becomes €51,840 total gross once holiday allowance is included. If the role also includes a 13th month payment (common in banking, utilities, and government), total gross annual compensation rises to approximately €55,840 on a €48,000 base.

Yes. An Employer of Record (EOR) with a Dutch-registered entity can formally employ workers in the Netherlands on behalf of an international client company. The EOR handles CLT-compliant employment contracts in Dutch, payroll tax withholding, Zvw health insurance enrolment, sector pension registration, the statutory 8% holiday allowance, and ongoing compliance with Dutch employment law. Typical setup takes 2-4 weeks, with costs of €400-700 per employee per month on top of gross salary and employer contributions. EORs routinely handle 30% ruling applications for international hires.

Copywriter

Christa is a Copywriter at Employsome with 17 years of professional writing experience across global brands, startups, and online publications. A native English-Finnish writer, she brings strong editorial skills and a versatile background in business, SaaS, and finance. At Employsome, Christa focuses on clear, practical content about HR, payroll, and Employer of Record topics.

Our content is created for informational purposes only and is not intended to provide any legal, tax, accounting, or financial advice. Please obtain separate advice from industry-specific professionals who may better understand your business’s needs. Read our Editorial Guidelines for further information on how our content is created.