Health Insurance in Hong Kong 2026: ECI, MPF, GMI & VHIS

Health insurance in Hong Kong combines a heavily-subsidised public system with one of the world’s most expensive private medical sectors. This 2026 guide covers mandatory Employees’ Compensation Insurance (ECI), MPF retirement contributions, optional but functionally-required group medical insurance (HK$11,078 average premium), the government-backed VHIS scheme with HK$8,000 tax deductions per insured person, and what international employers need to budget when hiring Hong Kong workers.

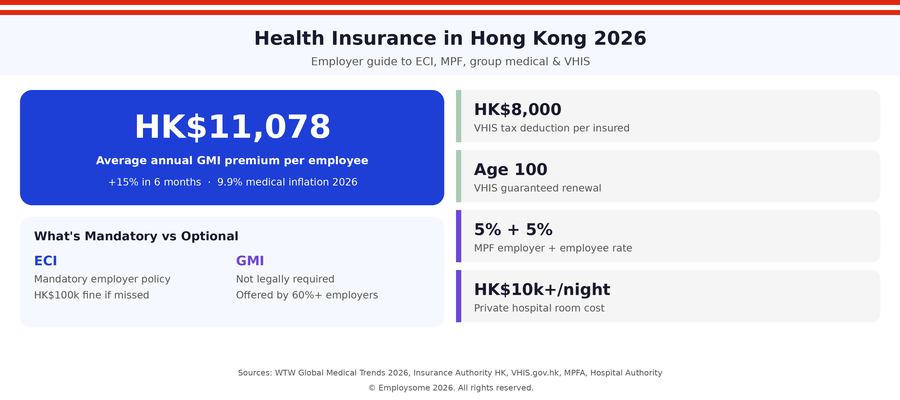

Health insurance in Hong Kong operates through a unique two-tier system that combines one of the world’s most heavily-subsidised public healthcare networks with the second most expensive private medical sector globally, behind only the United States. For employers, only Employees’ Compensation Insurance (ECI) is mandatory by law, but over 60% of Hong Kong companies provide group medical insurance as a market-standard employee benefit, with average annual premiums reaching HK$11,078 per insured employee in 2026, up nearly 15% in just six months.

Hong Kong employers face three distinct insurance considerations: the legally-mandatory ECI policy, optional but widely-expected group medical insurance (GMI), and the government-backed Voluntary Health Insurance Scheme (VHIS) which provides individual employees and their dependants with up to HK$8,000 in annual tax deductions per insured person. Medical inflation in Hong Kong is projected at 9.9% in 2026 according to WTW, with high-end plans rising as much as 30%, making thoughtful plan selection more important than ever.

This 2026 guide to health insurance in Hong Kong covers: the public Hospital Authority system and its limitations, mandatory ECI requirements and 2026 reimbursement updates, group medical insurance market norms and pricing, the VHIS scheme and its tax benefits, what employers must budget for benefits, the major insurance providers operating in Hong Kong, and what international companies need to know to remain compliant and competitive.

Hong Kong Healthcare System: Public vs Private

Hong Kong operates a two-tier healthcare system: a public sector managed by the Hospital Authority (HA) that provides heavily-subsidised care to all residents with a Hong Kong Identity Card, and a private sector dominated by international hospitals charging rates among the highest in Asia. Most working-age residents and expatriates rely on the private system through employer-provided group medical insurance.

The public HA system covers around 90% of inpatient bed-days in Hong Kong but is under significant strain. As of 2026, public hospitals operate at over 90% bed occupancy, waiting times for non-urgent specialist outpatient appointments routinely exceed 12 to 24 months, and public hospital fees rose in January 2026 to relieve some of the financial pressure. Around 22% of Hong Kong’s population is now aged 65 or above, projected to reach 36% by 2047, putting further structural pressure on both public and private capacity.

| Healthcare Tier | Cost (Approximate) | Wait Times |

| Public hospital ward (general) | HK$50 to HK$200 per day (subsidised) | Long for non-urgent |

| Public specialist outpatient | HK$100 to HK$200 per visit (subsidised) | 12 to 24+ months |

| Private hospital (semi-private) | HK$3,000 to HK$8,000 per night | Same-day to 1 week |

| Private hospital (private room) | HK$10,000+ per night | Same-day to 1 week |

| Top-tier private (Matilda, Hong Kong Sanatorium) | HK$12,000 to HK$25,000+ per night | Same-day |

| General private GP visit | HK$300 to HK$800 per consultation | Same-day |

| Private specialist consultation | HK$1,200 to HK$3,000 per consultation | 1 to 7 days |

Hong Kong’s private medical system is characterised by tight correlation between hospital room class and doctors’ fees: choosing a private room rather than semi-private not only increases the room rate but also raises the rates charged for surgery, consultations, and procedures. This is why room-class selection is a critical feature in any group medical insurance plan and why employers offering only basic plans see employees forced to top-up out-of-pocket or fall back to the overcrowded public system.

Mandatory Insurance: Employees’ Compensation Insurance (ECI)

The only legally-mandatory insurance for Hong Kong employers is Employees’ Compensation Insurance (ECI), required under the Employees’ Compensation Ordinance (Cap. 282). Every employer in Hong Kong must hold a valid ECI policy from the first day of employment, regardless of whether the worker is full-time, part-time, temporary, or an apprentice. Failure to maintain ECI carries a maximum fine of HK$100,000 plus 2 years of imprisonment.

ECI covers work-related injuries, occupational diseases, and death in the course of employment. Coverage includes medical expenses, statutory compensation for permanent incapacity or death, and reimbursement for periodical payments during temporary incapacity. Statutory minimum coverage scales with the number of employees:

| Number of Employees | Minimum ECI Coverage Per Event |

| 1 to 200 | HK$100 million |

| More than 200 | HK$200 million |

2026 ECI Medical Reimbursement Update: From 1 January 2026, the Hong Kong government raised the maximum daily medical reimbursement rates under ECI to reflect rising healthcare costs. Daily caps for hospitalisation, surgery, physiotherapy, and other approved medical treatments after work-related injuries have all increased. Employers should review existing ECI policies to ensure coverage limits remain aligned with the new statutory caps. In some cases, an endorsement or schedule adjustment is sufficient; older policies may need to be renewed at higher limits.

ECI premiums vary based on total annual salary, industry, occupational risk classification, and prior claims history. For office-based roles, annual premiums are typically 0.4% to 1% of total annual payroll. High-risk industries like construction or manufacturing pay 3% to 8% or more. ECI is purchased through licensed insurance brokers or directly from authorised insurers including Bupa Hong Kong, AIA, AXA, Generali, FWD, and Allianz.

💡 Employsome Insight: Group Medical Insurance Is Not Mandatory but Functionally Required

Many international employers entering Hong Kong assume that group medical insurance (GMI) is mandatory, like in many European countries. It is not. The only mandatory employer insurance in Hong Kong is Employees’ Compensation Insurance (ECI), which covers work-related injuries only. Group medical insurance (covering general illness and hospitalisation) is fully optional. However, in Hong Kong’s tight labour market, over 60% of employers offer GMI as part of their benefits package, and the figure is closer to 95% among large employers and competitive scaleups. Employees in finance, legal, technology, and professional services consider medical benefits the single most important non-cash benefit and will reject offers that lack adequate coverage. Treating GMI as optional will materially harm recruitment outcomes.

Group Medical Insurance (GMI) in Hong Kong

Group medical insurance (GMI) is the standard employer-provided health benefit in Hong Kong. It is not legally required but is offered by the vast majority of mid-sized and large employers, and is essentially expected in any professional or knowledge-worker role. According to industry research, over 60% of Hong Kong employers provide some form of group medical coverage in 2026, rising to 95%+ among larger companies and international firms.

2026 GMI premium benchmarks are as follows:

| Plan Tier | Monthly Cost per Employee | Annual Cost per Employee | Typical Coverage |

| Basic local plan | HK$800 to HK$1,500 | HK$9,600 to HK$18,000 | Hospitalisation, basic outpatient, semi-private room |

| Mid-tier plan (market average 2026) | HK$923 (HK$11,078/year) | HK$11,078 | Standard inpatient, outpatient, basic dental |

| Comprehensive local plan | HK$2,500 to HK$3,500 | HK$30,000 to HK$42,000 | Private room, full outpatient, dental, maternity |

| International / executive plan | HK$4,000 to HK$5,000+ | HK$48,000 to HK$60,000+ | Worldwide coverage, top-tier hospitals, no sub-limits |

The average annual premium per insured employee reached HK$11,078 in 2026 according to industry data, nearly 15% higher than just six months prior. The WTW 2026 Global Medical Trends report projects medical insurance costs in Hong Kong will rise by 9.9% across the year, with high-end and executive plans seeing increases of up to 30% as the Insurance Authority conducts a market-wide review of medical insurance pricing.

A typical Hong Kong group medical insurance plan covers:

- Hospitalisation: Room and board (with class restrictions), surgery, anaesthetist, ICU, hospital miscellaneous charges

- Outpatient care: GP consultations, specialist consultations, prescribed medication, diagnostic tests

- Maternity: Often subject to 10 to 12 month waiting periods; benefit limits typically HK$30,000 to HK$80,000 per pregnancy

- Dental: Basic preventive (cleaning, fillings) typically HK$1,500 to HK$3,000 annual limit; comprehensive plans cover crowns, root canals, orthodontics

- Mental health: Increasingly covered as standard, often with session limits and copayments

- Wellness: Annual physical examinations, vaccinations, health screenings

Most Hong Kong employers cover 70% to 100% of the employee premium, with employees often paying for dependant coverage. Large companies routinely cover dependants fully as a competitive benefit. Plans are typically tiered by seniority: junior staff receive a basic plan, mid-level staff receive an enhanced plan with higher limits and better room class, and senior executives receive comprehensive international plans.

Voluntary Health Insurance Scheme (VHIS) Explained

The Voluntary Health Insurance Scheme (VHIS) was launched by the Hong Kong Food and Health Bureau (now the Health Bureau) on 1 April 2019 as a government policy initiative to enhance the quality and protection level of individual hospital insurance products. Insurance companies participating in VHIS offer two types of certified plans: Standard Plans and Flexi Plans, both subject to government-mandated minimum standards.

VHIS is purchased by individuals, not employers, but it interacts with employer-provided group medical insurance in important ways. Employees can hold both a group plan and a VHIS policy, using VHIS to top-up their employer coverage and capture tax deductions unavailable through group plans.

| VHIS Feature | Standard Plan | Flexi Plan | Flexi Plan (Superior) |

| Annual benefit limit | HK$420,000 | HK$5 million+ | HK$30 million+ |

| Lifetime limit | None | None | None |

| Pre-existing conditions covered | Yes (with phased reimbursement) | Yes | Yes |

| Worldwide coverage | Yes (except psychiatric) | Yes (basic level) | Yes (Asia-only enhanced) |

| Renewal guaranteed to age | 100 | 100 | 100 |

| Tax deduction (per insured person) | Up to HK$8,000/year | Up to HK$8,000/year | Up to HK$8,000/year |

| Starting premium (age 30) | From HK$2,500/year | From HK$5,000/year | From HK$15,000/year |

A unique feature of VHIS is its coverage of unknown pre-existing conditions, which most traditional medical insurance specifically excludes. The reimbursement schedule is phased: 0% in the first policy year, 25% in the second year, 50% in the third, and 100% from the fourth year onwards. This provides genuine long-term security for workers who may have undiagnosed conditions at the time of policy issuance.

The VHIS tax deduction is one of its most attractive features for taxpayers. Hong Kong taxpayers can deduct qualifying VHIS premiums up to HK$8,000 per insured person per fiscal year, with no upper limit on the number of insured dependants. A taxpayer with a spouse, two children, and two parents covered under VHIS could deduct up to HK$48,000 (HK$8,000 × 6) annually. The deduction applies to the policyholder and their spouse if both are Hong Kong taxpayers, and dependants can include spouse, children, parents, grandparents, and siblings as defined under the Inland Revenue Ordinance (Cap. 112).

As of 2026, the major VHIS-certified providers in Hong Kong include AIA, AXA, HSBC Life, Cigna, Sun Life, Bupa, Bowtie, Manulife, Prudential, BOC Life, and FWD. All certified plans must meet the same minimum standards but vary in benefit ceilings, hospital network access, claim approval rates, and additional features such as cashless arrangements.

MPF and Other Mandatory Employer Benefits

In addition to ECI and group medical insurance, Hong Kong employers must enrol employees in the Mandatory Provident Fund (MPF), the country’s mandatory workplace retirement scheme. While MPF is technically a pension scheme rather than health insurance, it is part of the employer’s mandatory benefits package and worth understanding in context.

| MPF Component | 2026 Rate | Cap |

| Employer mandatory contribution | 5% of relevant income | HK$1,500/month (income above HK$30,000) |

| Employee mandatory contribution | 5% of relevant income | HK$1,500/month (income above HK$30,000) |

| Minimum income threshold | HK$7,100/month | Below this, employee contribution waived |

| Voluntary employer contribution | 2.5% to 15% of basic salary | No statutory cap |

In addition, the typical employee benefits package in Hong Kong includes:

- Life and disability insurance: Often provided as part of a group benefits package, typically 2x to 4x annual salary lump sum, with premiums of HK$30 to HK$100 per employee per month for basic cover

- Business travel insurance: Increasingly important given how many Hong Kong employees travel to Mainland China and across Asia for work; standard coverage HK$30 to HK$80 per employee per month

- Critical illness insurance: Lump-sum payouts for major conditions like cancer, heart attack, stroke; either employer-paid or available as voluntary employee top-up

- Annual physical examinations: Standard for senior staff and increasingly expected for junior staff at competitive employers

- Mental health and wellness benefits: Employee Assistance Programs (EAPs), counselling sessions, and wellness stipends are growing rapidly post-pandemic

A competitive Hong Kong total benefits package for a knowledge worker therefore typically includes: ECI (mandatory), MPF (mandatory, often supplemented with voluntary contributions), comprehensive group medical with dependant coverage, group life insurance, business travel insurance, mental health support, and an annual health check.

Total Employer Cost in Hong Kong 2026

For companies hiring in Hong Kong, the gross salary is only part of the cost. Mandatory MPF contributions, ECI premiums, group medical insurance (functionally required for recruitment), and statutory severance/long service payment reserves add a meaningful overhead. Below is an indicative breakdown for a worker on a HK$50,000 monthly gross salary (approximately HK$600,000 annually), a typical mid-level professional in Hong Kong:

| Cost Component (2026) | Rate | Annual Cost (HK$) |

| Gross salary | — | 600,000 |

| MPF employer contribution | 5% (capped at HK$30,000/month) | 18,000 |

| Employees’ Compensation Insurance (ECI) | ~0.5% of payroll (office) | 3,000 |

| Group medical insurance (employee + dependants) | HK$11,078 to HK$30,000+ | 11,078 to 30,000 |

| Group life and disability insurance | ~0.5% to 1% of salary | 3,000 to 6,000 |

| Severance/long service reserve | Effective ~3% to 4% of salary | 18,000 to 24,000 |

| Voluntary MPF top-up (competitive employers) | 5% to 10% | 30,000 to 60,000 |

| Total fully-loaded annual cost | ~12% to 25% uplift | ~683,000 to 741,000 |

For a HK$600,000 gross salary, the true fully-loaded annual employer cost in 2026 is approximately HK$683,000 to HK$741,000, a 14% to 24% uplift. This excludes additional costs such as office space, equipment, training budgets, performance bonuses (commonly 1 to 2 months of salary at year-end), and discretionary employer-provided benefits like gym memberships or transport allowances.

The largest employer cost variable is group medical insurance plan tier. A basic local plan at HK$11,078 per employee adds roughly 1.8% to total cost; an executive international plan at HK$60,000 adds 10%. For senior hires and roles competing against finance or technology multinationals, premium plans are essentially required.

Major Health Insurance Providers in Hong Kong

Hong Kong’s health insurance market is highly competitive, with both international and local insurers operating in the group medical and VHIS spaces. The major providers in 2026 include:

- AIA Hong Kong: One of the largest insurers in Asia and a market leader in individual VHIS plans. Strong brand presence and broad hospital network access.

- Bupa Hong Kong: Specialist health insurance brand with strong group medical expertise and extensive direct-billing hospital partnerships.

- AXA Hong Kong: Major group medical and VHIS provider, particularly strong in mid-market and SME group plans.

- Cigna Healthcare Hong Kong: Offers VHIS Flexi (Superior) with HK$30 million+ annual benefit limits and strong international coverage.

- HSBC Life: Strong VHIS portfolio with claim approval rates around 98.8% and a Care+ Medical Network covering Hong Kong and Mainland China.

- Allianz Hong Kong: Strong international group plan coverage, especially for expatriates and multinational employers.

- Manulife Hong Kong: Major VHIS and life insurance provider with broad distribution.

- Sun Life Hong Kong: VHIS provider with strong distribution through banks and financial advisors.

- Prudential Hong Kong: Major life and medical insurer with strong VHIS product portfolio.

- FWD Hong Kong: Modern, digital-first insurer with competitive VHIS pricing and increasingly strong group medical offering.

- Bowtie: Hong Kong’s first virtual insurer, offering fully-digital group medical and VHIS plans with rapid onboarding (5 minutes for new employees) and high transparency.

- Generali Hong Kong: International insurer with employee benefits expertise.

- Blue Cross (Asia-Pacific): Major group medical provider with strong direct-billing network.

- April International: Specialist provider for SMEs and international employers, with tailored expat plans.

For employers, the choice of insurer depends on company size, employee mix (local vs expatriate), budget, and strategic priorities. Most Hong Kong employers work through specialist health insurance brokers (Alea, Pacific Prime, Navigator Insurance, Asinta, Ximco) who manage the procurement process, negotiate terms, and provide ongoing claims support. Brokers are particularly valuable for groups under 100 employees where direct insurer relationships are less efficient.

How International Companies Hire in Hong Kong

For international companies hiring in Hong Kong without a local entity, there are two practical options: establish a Hong Kong limited company or use an Employer of Record (EOR).

Option 1: Establish a Hong Kong limited company

Setting up a Hong Kong limited company requires incorporation through the Companies Registry, business registration with the Inland Revenue Department, opening a Hong Kong corporate bank account (the longest step, often 4 to 12 weeks given enhanced KYC requirements), MPF scheme enrolment with an approved trustee, ECI policy procurement, and optional GMI procurement. Total timeline is typically 6 to 16 weeks. Ongoing costs include accounting (HK$1,500 to HK$5,000 per month), annual audit, profits tax filings, company secretary services, and payroll administration.

Option 2: Employer of Record (EOR)

An EOR is a Hong Kong-registered entity that formally employs the worker on your behalf. The EOR handles Hong Kong employment contracts in compliant English (or bilingual English/Chinese), monthly payroll with MPF withholding, ECI policy maintenance, group medical insurance enrolment, severance and long service payment reserves, and ongoing compliance with the Employment Ordinance. Typical setup: 1 to 3 weeks. Typical cost: USD 500 to USD 900 per employee per month on top of gross salary, mandatory contributions, and any group medical premiums.

For hiring one to five Hong Kong employees, or for 6 to 24 month projects, an EOR is almost always the faster and lower-risk option. For longer-term operations with 5+ Hong Kong employees, incorporating a local entity eventually becomes more cost-effective. Most EOR providers in Hong Kong offer at least one tier of group medical insurance as a standard add-on, with premium options available for senior hires.

What International Employers Need to Know

ECI is mandatory; group medical insurance is functionally required

Hong Kong law requires only Employees’ Compensation Insurance (ECI). Group medical insurance (GMI) is not mandatory but is offered by 60%+ of employers and 95%+ of competitive employers. For knowledge worker roles, treating GMI as optional will materially harm recruitment outcomes. Plan to budget for at least a basic GMI plan from day one.

Budget for HK$11,000 to HK$30,000 per employee per year for medical

The 2026 average GMI premium is HK$11,078 per insured employee for a mid-tier plan. Comprehensive plans range from HK$30,000 to HK$60,000+. Medical inflation in Hong Kong is projected at 9.9% in 2026, so multi-year compensation budgets should include progressive cost increases. High-end and executive plans are seeing inflation up to 30%.

Account for the new 2026 ECI medical reimbursement limits

From 1 January 2026, the maximum daily medical reimbursement rates under ECI increased to reflect rising healthcare costs. Review existing ECI policies to ensure coverage limits remain aligned. In some cases an endorsement is sufficient; older policies may need renewal at higher limits.

Communicate VHIS as a top-up benefit to employees

VHIS is purchased by individuals, not employers, but it offers up to HK$8,000 in annual tax deductions per insured person. Inform employees about VHIS so they understand they can supplement employer coverage and capture tax benefits. Highlighting this in onboarding materials adds value at no cost to the employer.

Tier benefits by seniority

Standard market practice in Hong Kong is to tier medical benefits by employee level: junior staff on basic plans, mid-level staff on enhanced plans, senior staff on comprehensive or international plans. This controls cost while remaining competitive at the roles where competition for talent is most intense.

Use a specialist Hong Kong broker for groups under 100

Hong Kong’s health insurance market is dense and broker-driven. Specialist brokers (Alea, Pacific Prime, Navigator Insurance) negotiate better rates, provide claim support, and handle annual renewals. For SMEs and scaleups, broker fees are recovered many times over through better pricing and reduced administrative burden.

Consider an EOR for compliant Hong Kong hiring

For international companies without a Hong Kong entity, an Employer of Record handles ECI, MPF, employment contracts, payroll, and group medical procurement automatically. See our Best EOR in Hong Kong guide for verified provider rankings.

Hiring in Hong Kong?

Hong Kong employment requires mandatory ECI, MPF enrolment, and competitive group medical insurance to attract talent in one of Asia’s tightest labour markets. Navigating local insurance brokers, the 2026 ECI reimbursement updates, and VHIS tax deduction communication requires local expertise. Compare the top Employer of Record providers for Hong Kong in 2026 – verified pricing, compliance scores, and expert rankings from Employsome’s independent research team.

Frequently Asked Questions

No, group medical insurance (covering general illness and hospitalisation) is not legally mandatory in Hong Kong. The only mandatory employer-provided insurance is Employees’ Compensation Insurance (ECI), which covers work-related injuries and occupational diseases. Failure to maintain ECI carries a maximum fine of HK$100,000 plus 2 years of imprisonment. However, over 60% of Hong Kong employers offer group medical insurance as a market-standard benefit, rising to 95%+ among large companies, so it is functionally required for competitive recruitment.

Hong Kong group medical insurance costs range from HK$800 to HK$5,000+ per employee per month depending on plan tier. The 2026 average premium per insured employee is HK$11,078 per year (approximately HK$923 per month), up nearly 15% in the past six months. Basic local plans cost HK$9,600 to HK$18,000 per year; comprehensive local plans HK$30,000 to HK$42,000; international or executive plans HK$48,000 to HK$60,000+ per year. Medical inflation in Hong Kong is projected at 9.9% in 2026.

The Voluntary Health Insurance Scheme (VHIS) is a Hong Kong government-backed individual health insurance scheme launched on 1 April 2019 by the Health Bureau. VHIS-certified plans must meet minimum standards including coverage of unknown pre-existing conditions, guaranteed renewal up to age 100, and worldwide coverage. There are two types: Standard Plans with HK$420,000 annual benefit limits and Flexi Plans with HK$5 million to HK$30 million+ limits. VHIS premiums qualify for tax deductions of up to HK$8,000 per insured person per year.

Hong Kong taxpayers can deduct qualifying VHIS premiums up to HK$8,000 per insured person per fiscal year from their salaries tax. There is no upper limit on the number of insured dependants. A taxpayer with a spouse, two children, and two parents covered under VHIS could deduct up to HK$48,000 (HK$8,000 × 6) per year. The deduction is claimed on the salaries tax return and dependants must include spouse, children, parents, grandparents, or siblings as defined under the Inland Revenue Ordinance (Cap. 112).

Employees’ Compensation Insurance (ECI) is the only mandatory employer-provided insurance in Hong Kong. Required under the Employees’ Compensation Ordinance (Cap. 282), ECI covers work-related injuries, occupational diseases, and death in the course of employment. Statutory minimum coverage is HK$100 million per event for employers with 1-200 employees, rising to HK$200 million for larger employers. From 1 January 2026, the maximum daily medical reimbursement rates under ECI have increased. ECI premiums are typically 0.4% to 1% of total annual payroll for office-based work, rising to 3-8% for high-risk industries like construction.

The Mandatory Provident Fund (MPF) is Hong Kong’s mandatory workplace retirement scheme. Employers and employees each contribute 5% of relevant income, capped at HK$1,500 per month for monthly incomes above HK$30,000. Employees earning below HK$7,100 per month are exempt from making employee contributions, but employers must still contribute. Many competitive employers offer voluntary MPF top-ups of 2.5% to 15% of basic salary as an additional retirement benefit. MPF is administered by approved trustees including HSBC, Manulife, AIA, and Sun Life.

Coverage of pre-existing conditions varies by plan type. Most traditional group medical insurance plans exclude pre-existing conditions entirely or apply waiting periods of 6 to 12 months. VHIS-certified plans are unique in covering unknown pre-existing conditions on a phased basis: 0% reimbursement in the first policy year, 25% in the second year, 50% in the third year, and 100% from the fourth year onwards. This makes VHIS particularly valuable for employees who may have undiagnosed conditions at the time of policy issuance.

Expatriates in Hong Kong typically receive enhanced or international group medical plans with higher benefit limits, broader hospital network access, worldwide coverage, and dependant inclusion. International plans cost HK$4,000 to HK$5,000+ per employee per month, compared to HK$800 to HK$1,500 for basic local plans. Major insurers offering expat plans include AXA, Allianz, AIA, Bupa, Cigna, and Generali. Expats should also consider VHIS for tax benefits if they qualify as Hong Kong taxpayers.

Practice varies. Many large Hong Kong employers cover dependants (spouse and children) fully or partially as a competitive benefit, particularly in finance, professional services, and technology sectors. SMEs and budget-conscious employers typically offer dependant coverage as an optional employee-paid benefit, often at preferential group rates. Where employers cover dependants, costs typically double or triple per employee. Competitive Hong Kong employers cover dependants as a standard benefit for senior staff and offer it optionally for junior staff.

An Employer of Record (EOR) handles all Hong Kong employer insurance and benefits compliance on behalf of international clients. The EOR maintains a valid ECI policy from day one of employment, enrols employees in MPF with an approved trustee, procures group medical insurance (typically with multiple plan tiers available), manages monthly payroll deductions, and ensures compliance with the Employment Ordinance. For companies hiring 1-5 Hong Kong employees without a local entity, an EOR is almost always faster and more cost-effective than incorporating a local company. See our Best EOR in Hong Kong guide for provider rankings.

Dane Cobain is a Copywriter at Employsome and an accomplished author whose work spans fiction, non-fiction, and professional writing. Over the past decade, he has built a strong track record creating straightforward content for the HR, payroll, and corporate sectors. Dane brings a storyteller’s eye to the evolving world of global employment, with a particular focus on Employer of Record and PEO models. His articles explore industry trends and dedicated Best Of Guides when managing an international workforce.

Our content is created for informational purposes only and is not intended to provide any legal, tax, accounting, or financial advice. Please obtain separate advice from industry-specific professionals who may better understand your business’s needs. Read our Editorial Guidelines for further information on how our content is created.