Minimum Wage in Hong Kong: The Complete 2026 Guide

Hong Kong’s minimum wage rises to HK$43.1/hour from May 1, 2026: the first increase under a new annual review mechanism. With 5% MPF contributions (capped at HK$1,500/month) and no social security tax, Hong Kong has the lowest employer-side statutory costs in Asia. But two major changes hit in 2025-26: the “468” continuous contract rule expands part-time worker protections, and the MPF offset abolition means you can no longer reduce severance payments with pension contributions.

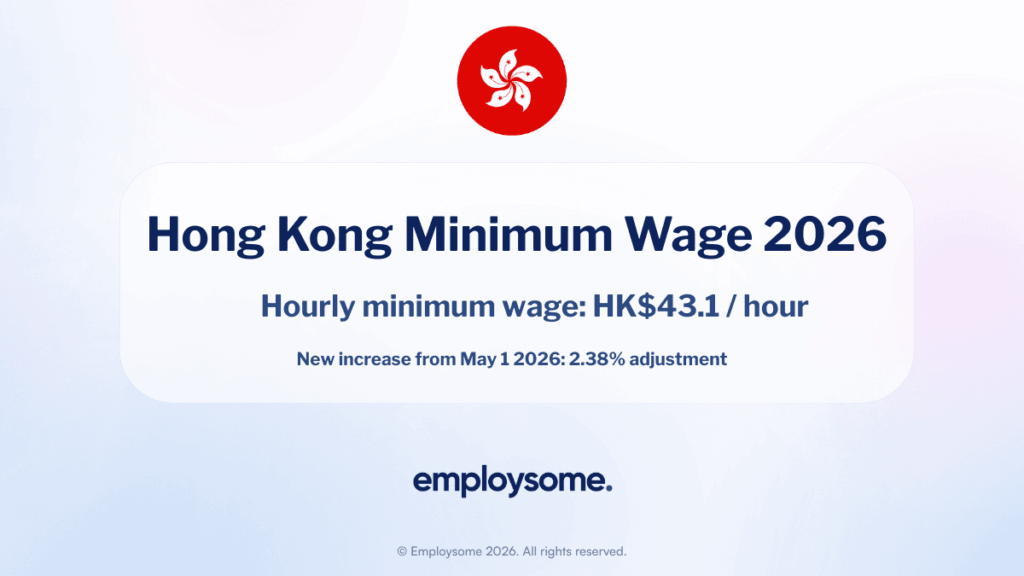

The minimum wage in Hong Kong is rising to HK$43.1 per hour from 1 May 2026, up from HK$42.1 per hour. This is the first increase under a new annual review mechanism adopted by the government, replacing the previous biennial review cycle. The HK$1 per hour increase represents a 2.38% adjustment.

Hong Kong’s statutory minimum wage (SMW) applies universally to all employees regardless of age, contract type, or pay frequency, making it one of the few jurisdictions in the world without age-based wage tiers. Unlike many countries, Hong Kong does not have a separate social security tax system. Instead, retirement savings are handled through the Mandatory Provident Fund (MPF), where both employer and employee contribute 5% of relevant income, capped at HK$1,500 per month each.

For employers hiring in Hong Kong, whether through a local company or an Employer of Record, understanding the minimum wage, MPF obligations, and recent legislative changes (including the 2026 “468” continuous contract rule and the May 2025 MPF offset abolition) is essential for compliance and accurate cost planning.

💡 Employsome Insight: Hong Kong’s Employer Costs Are Low by Global Standards

Unlike most countries covered in our hiring guides, Hong Kong has no employer social security tax, no payroll tax, and no mandatory health insurance contribution. The only mandatory employer contribution is 5% MPF, capped at HK$1,500/month. This makes Hong Kong one of the cheapest places in Asia for employer-side statutory costs. However, the high cost of living means competitive salaries are significantly above the minimum wage for most professional roles.

Minimum Wage in Hong Kong: Current and Upcoming Rate

|

Detail |

Value |

|

Current SMW rate (until 30 April 2026) |

HK$42.1 per hour |

|

New SMW rate (from 1 May 2026) |

HK$43.1 per hour |

|

Increase |

HK$1.00 per hour (+2.38%) |

|

Approximate USD equivalent |

~US$5.51 per hour |

|

Monthly equivalent (full-time, 40hrs/week) |

~HK$7,469 (at 173.3 hours/month) |

|

Monthly equivalent (48hrs/week) |

~HK$8,966 |

|

Record-keeping threshold (from 1 May 2026) |

HK$17,600/month (up from HK$17,200) |

|

Legal basis |

Minimum Wage Ordinance (Cap. 608), Amendment Notice 2026 |

The minimum wage in Hong Kong applies uniformly across all districts, all age groups, and all industries. There are no regional variations, sector-specific rates, or youth rates. When dividing an employee’s total wages by their total working hours in any wage period, the resulting average must not fall below the SMW rate.

The New Annual Review Mechanism

In a significant policy shift, the Hong Kong government has adopted an annual review mechanism for the statutory minimum wage, replacing the previous biennial (every two years) review cycle. The May 2026 adjustment is the first increase under this new formula.

The Minimum Wage Commission (MWC) now uses a formula-based approach that considers two key indicators: inflation (to ensure the SMW keeps pace with the cost of living) and economic growth (to allow wage increases that reflect Hong Kong’s economic performance). The Chief Executive in Council reviews the MWC’s recommendation and adopts the new rate.

The shift to annual reviews means employers should expect more frequent, smaller adjustments rather than larger biennial jumps. This creates greater predictability but requires annual payroll system updates.

💡 Employsome Insight: Annual Reviews Mean Annual Payroll Updates

With the shift from biennial to annual minimum wage reviews, employers in Hong Kong now need to update payroll systems and employment contracts every May. If you are using an EOR, confirm that your provider automatically applies SMW changes on the effective date. Some providers require manual contract amendments, which can delay compliance if not actioned promptly.

Who Is Covered by the Minimum Wage

The statutory minimum wage covers virtually all employees in Hong Kong, including full-time, part-time, and casual workers, regardless of whether they are paid hourly, daily, monthly, or by piece rate. It also applies to overtime hours.

Exemptions

Foreign domestic helpers: Live-in foreign domestic helpers are not covered by the SMW. Instead, they are entitled to the Minimum Allowable Wage (MAW), currently set at HK$4,990 per month, which is a separate framework under Immigration Department regulations.

Student interns: Students undertaking exempt student employment (internships arranged or endorsed by their educational institution as part of an accredited programme) are exempt from the SMW during the internship period.

Employees with disabilities: Employees with disabilities are covered by the SMW but may opt for a productivity assessment. If the assessment shows productivity below 100%, a pro-rata wage can be applied based on the assessed productivity level.

How to Calculate Minimum Wage Compliance

The minimum wage in Hong Kong is calculated by comparing total wages against total hours worked in each wage period:

Minimum wage = Total hours worked in the wage period × SMW rate

If an employee works 176 hours in a month and the SMW is HK$43.1, the minimum wage for that period is 176 × HK$43.1 = HK$7,585.60. If the employee’s total wages for that period are below this amount, the employer must pay the difference.

Hours that count as “worked” include time spent travelling to a workplace other than the usual one, time on standby or on-call at a location required by the employer, and meal breaks where the employee must remain on duty or at the workplace.

Record-Keeping Requirement

Employers must maintain records of the total hours worked by any employee earning less than HK$17,600 per month (from 1 May 2026, up from HK$17,200). For employees earning above this threshold, record-keeping of hours is not mandatory but remains recommended for compliance evidence.a

Mandatory Provident Fund (MPF) Employer Contributions

Hong Kong does not have a social security tax or employer payroll tax. Instead, retirement savings are handled through the Mandatory Provident Fund (MPF), the territory’s compulsory pension scheme.

|

MPF Detail |

2026 Rate |

|

Employer contribution rate |

5% of relevant income |

|

Employee contribution rate |

5% of relevant income |

|

Minimum relevant income (no employee contribution below this) |

HK$7,100/month |

|

Maximum relevant income (contributions capped) |

HK$30,000/month |

|

Maximum employer contribution |

HK$1,500/month |

|

Maximum employee contribution |

HK$1,500/month |

|

Enrolment deadline |

Within 60 days of employment start |

|

Employee contribution holiday |

First 30 days of employment (employee only) |

If an employee earns less than HK$7,100 per month, the employee does not contribute but the employer must still pay 5%. If the employee earns more than HK$30,000, both contributions are capped at HK$1,500 each.

MPF Offset Abolition (Effective 1 May 2025)

From 1 May 2025, employers can no longer use their mandatory MPF contributions to offset statutory severance payments (SP) or long service payments (LSP). This means employers must now fund SP and LSP entirely from their own resources for service accrued after the transition date. The government provides a 25-year subsidy scheme (2025 to 2050) with annual subsidies capped at HK$500,000 per employer to help businesses transition.

💡 Employsome Insight: MPF Offset Abolition Increases Your True Termination Cost

Before May 2025, employers could reduce severance payments by deducting their MPF contributions. This is no longer possible for post-transition service. For employers hiring through an EOR in Hong Kong, this means termination costs are now higher than they were historically. Ask your EOR provider how they handle SP/LSP calculations and whether the cost is included in the monthly fee or billed separately at termination.

Statutory Leave Entitlements

Employees in Hong Kong under a continuous contract are entitled to several categories of statutory leave:

|

Leave Type |

Entitlement |

Notes |

|

Annual leave |

7 days (1st year) up to 14 days (9+ years) |

Increases by 1 day per year of service. Paid at average daily wage. |

|

Statutory holidays |

15 days per year (2026) |

Gradually increasing to 17 days by 2030. Paid if employed for 3+ months. |

|

Sick leave |

2 paid days per month (first year), 4 days/month thereafter |

Accumulates up to 120 days. Paid at 4/5 of average daily wage. Medical certificate required for 4+ consecutive days. |

|

Maternity leave |

14 weeks |

Paid at 4/5 of average daily wage. Government reimburses the additional 4 weeks (capped at HK$36,822). |

|

Paternity leave |

5 days |

Paid at 4/5 of average daily wage. Must be taken within 8 weeks of birth. |

|

Rest days |

1 day per 7-day period |

Can be unpaid unless CBA or contract specifies otherwise. |

The New “468” Continuous Contract Rule (Effective 18 January 2026)

The Employment (Amendment) Ordinance 2025 came into effect on 18 January 2026, lowering the threshold for a “continuous contract” from 18 hours per week over 4 consecutive weeks to either 68 hours over 4 consecutive weeks or 17 hours in any week over 4 consecutive weeks. This means more part-time and casual workers now qualify for statutory benefits including annual leave, sick leave, severance, and long service payments. Employers must review their current rostering and hiring practices to ensure compliance.

💡 Employsome Insight: The 468 Rule Expands Your Obligations to Part-Time Staff

If you employ part-time workers in Hong Kong who previously fell below the 18-hour weekly threshold, they may now qualify for full statutory benefits under the new 468 rule. This is particularly relevant for retail, hospitality, and food service employers. Review all part-time contracts and working hour records to determine which employees are now eligible for annual leave, sick leave, and termination protections.

Penalties for Non-Compliance

Hong Kong takes minimum wage enforcement seriously. Penalties for non-compliance include:

Intentional underpayment: Fines of up to HK$350,000 and imprisonment for up to 3 years for wilfully and without reasonable excuse failing to pay the minimum wage.

Late payment of wages: Interest charges accrue on any wages paid late. Wages must be paid as soon as practicable but no later than 7 days after the end of the wage period.

MPF non-compliance: Failure to enrol eligible employees or make MPF contributions on time results in a mandatory 5% surcharge on outstanding amounts. Serious or repeated breaches can lead to fines of up to HK$450,000 and imprisonment for up to 4 years.

Personal liability: Directors, managers, company secretaries, or similar officers may be personally liable if the offence was committed with their consent, knowledge, or neglect.

Historical Minimum Wage Trend

|

Effective Date |

Hourly Rate (HK$) |

Increase (%) |

Review Cycle |

|

May 2011 (first SMW) |

28.0 |

N/A |

N/A |

|

May 2013 |

30.0 |

7.1% |

Biennial |

|

May 2015 |

32.5 |

8.3% |

Biennial |

|

May 2017 |

34.5 |

6.2% |

Biennial |

|

May 2019 |

37.5 |

8.7% |

Biennial |

|

May 2023 |

40.0 |

6.7% |

Biennial (delayed from 2021 due to COVID) |

|

May 2025 |

42.1 |

5.25% |

Biennial (last under old cycle) |

|

May 2026 |

43.1 |

2.38% |

Annual (first under new cycle) |

Since its introduction in 2011, Hong Kong’s minimum wage has increased by 54% from HK$28 to HK$43.1. The shift to annual reviews from 2026 is expected to produce smaller but more frequent adjustments, giving businesses more predictability in their cost planning.

How Does Hong Kong Compare Regionally?

|

Jurisdiction |

Min. Wage (USD/hour equiv.) |

Employer Pension/SI Rate |

Notes |

|

Hong Kong |

~$5.51 |

5% MPF (capped HK$1,500/month) |

No social security tax, no payroll tax |

|

Singapore |

No national min. wage |

~17% CPF (varies by age) |

Sector-specific PWM only |

|

Mainland China (Beijing) |

~$3.53 |

~30-40% (varies by city) |

Regional variation |

|

Mainland China (Shenzhen) |

~$3.60 |

~30-40% |

Adjacent to Hong Kong |

|

Macau |

~$4.20 |

~5% (Social Security Fund) |

Separate jurisdiction |

|

Taiwan |

~$6.12 |

~17-20% |

NHI + Labor Insurance + Pension |

|

South Korea |

~$6.80 |

~19-20% |

National Pension + Health + Employment Insurance |

Hong Kong’s minimum wage sits in the middle of the regional range on an hourly basis, but its total employer cost is among the lowest due to the absence of social security taxes. The 5% MPF contribution capped at HK$1,500/month is significantly cheaper than the 20 to 40% employer social insurance burden in mainland China or the 17 to 20% rates in Taiwan and South Korea.

💡 Hiring in Hong Kong?

Compare the best EOR providers for Hong Kong on Employsome. We score each provider on entity ownership, local compliance expertise, MPF handling, and payroll accuracy so you can hire compliantly without setting up a Hong Kong entity. Visit our Hong Kong EOR Guide to see the full comparison.

Frequently Asked Questions

The statutory minimum wage in Hong Kong is HK$42.1 per hour until 30 April 2026. From 1 May 2026, it increases to HK$43.1 per hour (approximately US$5.51), subject to Legislative Council approval.

The statutory minimum wage is set as an hourly rate. There is no separate monthly minimum wage. For monthly-paid employees, compliance is checked by dividing total wages by total hours worked in the wage period.

Yes. The minimum wage applies to all employees in Hong Kong regardless of whether they work full-time, part-time, or on a casual basis. Under the new 468 rule effective 18 January 2026, more part-time workers now also qualify for statutory benefits.

No. Foreign domestic helpers are exempt from the statutory minimum wage and instead receive the Minimum Allowable Wage (currently HK$4,990/month), which is a separate framework administered by the Immigration Department.

Both employer and employee contribute 5% of the employee’s relevant income, capped at a maximum contribution of HK$1,500 per month each (based on a maximum relevant income of HK$30,000). If the employee earns below HK$7,100/month, only the employer contributes.

Intentional non-payment carries fines of up to HK$350,000 and imprisonment for up to 3 years. Directors and officers can be held personally liable. MPF non-compliance can result in a 5% surcharge, fines up to HK$450,000, and imprisonment for up to 4 years.

Yes. An Employer of Record becomes the legal employer in Hong Kong and handles employment contracts, payroll, MPF enrolment and contributions, statutory holiday pay, and compliance with the Employment Ordinance. This allows foreign companies to hire in Hong Kong without incorporating a local entity.

Written by

Courtney Pocock is a Copywriter & EOR/PEO Researcher at Employsome with 15+ years of experience writing for the HR, corporate, and financial sectors. She has a strong interest in global business expansion and Employer of Record / PEO topics, focusing on news that matters to business owners and decision-makers. Courtney covers industry updates, regulatory changes, and practical guides to help leaders navigate international hiring with confidence.

Our content is created for informational purposes only and is not intended to provide any legal, tax, accounting, or financial advice. Please obtain separate advice from industry-specific professionals who may better understand your business’s needs. Read our Editorial Guidelines for further information on how our content is created

Other posts

Along with our standard maps we offer highly customizable maps.