Insurance for Expats in Germany: What You Need (2026)

Every person living in Germany must have health insurance from day one. There are no exceptions for expats. Beyond health insurance, Germany has a comprehensive system of mandatory and recommended insurance types that expats need to understand. This guide covers the full landscape: public vs. private health insurance, long-term care insurance, personal liability, household contents, car insurance, pension contributions, and the optional policies that most financial advisors recommend for expats settling in Germany.

Table of Contents

- Long-Term Care Insurance (Pflegeversicherung)

- Pension Insurance (Rentenversicherung)

- Personal Liability Insurance (Privathaftpflichtversicherung)

- Household Contents Insurance (Hausratversicherung)

- Car Insurance for Expats in Germany (Kfz-Versicherung)

- Other Insurance Expats in Germany Should Consider

- What Insurance Means for EOR

- Insurance Checklist for Expats Moving to Germany

- Final Takeaway

Insurance in Germany: Why It Matters for Expats

Germany has one of the most comprehensive insurance systems in the world. The country’s insurance culture goes far beyond health coverage: Germans routinely carry personal liability, household contents, legal protection, and occupational disability insurance alongside their mandatory health, pension, and long-term care policies.

For expats, understanding this system is not optional. Proof of health insurance is required for your residence permit (Aufenthaltserlaubnis). You cannot register your address (Anmeldung) or complete your work permit application without it. And if you plan to drive, you cannot register a vehicle without valid third-party car insurance.

Germany’s insurance landscape divides into two categories:

- Mandatory insurance (Pflichtversicherung): Health insurance, long-term care insurance, pension contributions, unemployment insurance, and car insurance (if you drive). These are required by law.

- Recommended insurance (Freiwillige Versicherung): Personal liability, household contents, legal protection, dental supplementary, occupational disability, and life insurance. These are not legally required but are considered essential by most financial advisors in Germany.

|

Insurance Type |

Status |

Approximate Monthly Cost |

|

Health insurance (GKV/PKV) |

Mandatory |

€400–€1,000+ (employee pays half) |

|

Long-term care insurance |

Mandatory |

3.4–4.0% of gross salary (bundled with health) |

|

Pension insurance |

Mandatory (employees) |

18.6% of gross salary (half employer-paid) |

|

Unemployment insurance |

Mandatory (employees) |

2.6% of gross salary (half employer-paid) |

|

Car insurance (third-party) |

Mandatory (if driving) |

€100–€1,000+/year |

|

Personal liability insurance |

Highly recommended |

€3–€15/month |

|

Household contents insurance |

Recommended |

€2.50–€15/month |

|

Dental supplementary insurance |

Recommended |

€10–€50/month |

|

Legal protection insurance |

Optional |

€10–€40/month |

|

Occupational disability insurance |

Highly recommended |

€50–€200/month |

|

Life insurance |

Optional |

Varies widely |

💡 Employsome Insight: Germany’s Insurance Culture Is Different from Most Countries

Expats from the US, UK, or Asia are often surprised by how insurance-heavy German culture is. Personal liability insurance alone is carried by approximately 80% of German households, even though it’s not legally required. The reason is Germany’s strict civil liability laws: you are personally liable for all damages you cause to other people or their property, with no cap. A single accident while cycling could make you liable for millions in lifetime earnings compensation. For €3–15/month, liability insurance is considered non-negotiable by virtually every financial advisor in Germany.

Health Insurance in Germany (Krankenversicherung)

Health insurance is the single most important insurance decision for any expat moving to Germany. It has been legally mandatory for all residents since 2009 under the Fifth Book of the Social Code (SGB V). There are two systems:

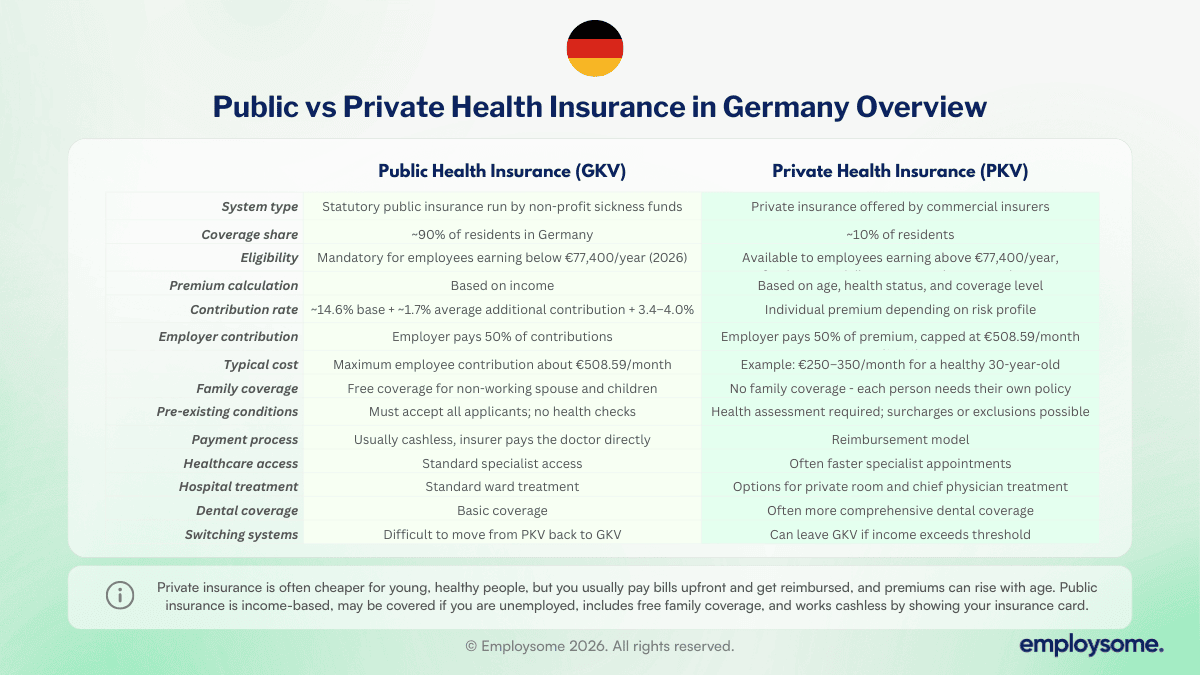

Public Health Insurance (Gesetzliche Krankenversicherung, GKV)

Approximately 90% of people in Germany are covered by public health insurance. The system is administered by non-profit sickness funds (Krankenkassen) such as TK (Techniker Krankenkasse), Barmer, AOK, and DAK.

Key features of GKV for expats:

- Who must join: Employees earning below the compulsory insurance threshold of €77,400/year (2026) are automatically enrolled. This covers the vast majority of employed expats.

- Contribution rate: 14.6% of gross salary as the base rate, plus an average additional contribution of approximately 1.7% (varies by insurer), plus long-term care insurance of 3.4–4.0%. The employer pays half of all contributions.

- Maximum contribution: Contributions are capped at the income ceiling (Beitragsbemessungsgrenze) of approximately €5,512.50/month (2026). The maximum employee health insurance contribution is approximately €508.59/month.

- Family coverage: Non-working spouses and children are covered at no additional cost under family insurance (Familienversicherung). This is one of GKV’s biggest advantages for expats with families.

- Pre-existing conditions: GKV must accept all applicants and covers all pre-existing conditions. There are no health assessments or exclusions.

- Coverage: Doctor visits, hospital stays, prescription medications, maternity care, preventive checkups, and rehabilitation. Co-payments are minimal (typically €5–10 for prescriptions).

Private Health Insurance (Private Krankenversicherung, PKV)

Private health insurance is available to expats who meet specific eligibility criteria:

- Who can join: Employees earning above €77,400/year (2026), self-employed individuals and freelancers (regardless of income), civil servants, and students who opt out of GKV at the start of their studies.

- Contribution basis: Premiums are based on individual risk (age, health status, coverage level) rather than income. A healthy 30-year-old may pay €250–350/month; premiums increase with age and health conditions.

- Employer contribution: Employers pay half of the PKV premium, up to the maximum GKV employer contribution (€508.59/month in 2026).

- Coverage: Generally broader than GKV. Includes faster specialist access, private hospital rooms, chief physician treatment, and full dental coverage depending on the tariff chosen.

- No family coverage: Each family member requires their own policy. This makes PKV significantly more expensive for families than GKV.

- Pre-existing conditions: PKV conducts health assessments. Pre-existing conditions may result in surcharges, exclusions, or rejection. Applicants who are rejected can access a basic tariff (Basistarif) at regulated rates.

💡 Employsome Insight: Switching from PKV Back to GKV Is Extremely Difficult

This is the most consequential health insurance decision an expat will make in Germany. Once you switch to private insurance, returning to public insurance is very difficult, especially after age 55. If your income drops below the threshold or you become unemployed, you may be trapped in PKV with premiums you can no longer afford. For expats who are uncertain about their long-term plans in Germany, staying in GKV is almost always the safer choice. The free family coverage alone can save a family with a non-working spouse and two children €500–800/month compared to PKV.

Expat Health Insurance (Temporary Coverage)

For expats who have just arrived and are not yet eligible for GKV or PKV (visa applicants, job seekers, language students), temporary expat health insurance provides coverage for up to 5 years. Providers like Feather, DR-WALTER, and Care Concept offer plans starting from approximately €72/month. These plans meet the minimum requirements for residence permit applications but are not a substitute for long-term GKV or PKV coverage.

Long-Term Care Insurance (Pflegeversicherung)

Long-term care insurance is mandatory for all residents in Germany and is automatically bundled with your health insurance. It was introduced in 1995 to ensure everyone is covered for eventual nursing care needs due to illness, disability, or old age.

Key details for expats:

- Contribution rate: 3.4% of gross salary for employees with children; 4.0% for childless employees over 23. The employer pays half (1.7%).

- Coverage: Home care allowances, outpatient care services, inpatient nursing home subsidies, and support for family caregivers. Benefits vary by care grade (Pflegegrad 1–5).

- Important limitation: Long-term care insurance does not cover the full cost of nursing home accommodation. Residents typically pay €2,000+/month out of pocket for room, board, and facility costs beyond what insurance covers.

Pension Insurance (Rentenversicherung)

All employees in Germany are required to contribute to the statutory pension system (Deutsche Rentenversicherung). This is a pay-as-you-go system funded by current contributions.

- Contribution rate: 18.6% of gross salary, split equally between employer (9.3%) and employee (9.3%).

- Contribution ceiling: West Germany: approximately €7,550/month (2026); East Germany: approximately €7,450/month.

- Eligibility for benefits: A minimum of 5 years of contributions (60 months) is required to qualify for a German pension. This is important for expats who may leave before reaching this threshold.

- Social security agreements: Germany has bilateral social security agreements with many countries (US, UK, Canada, Australia, and others) that allow contribution periods to be combined across countries. EU/EEA coordination rules also apply.

- Freelancers: Self-employed individuals are generally not required to contribute to the statutory pension system but may opt in voluntarily or arrange private pension plans.

💡 Employsome Insight: The 5-Year Minimum Matters for Expats Who May Not Stay

If you leave Germany before completing 60 months of pension contributions, you can apply for a refund of your employee contributions (but not the employer’s share) after a 24-month waiting period. However, if your home country has a social security agreement with Germany, it may be possible to combine contribution periods rather than requesting a refund. This decision has long-term financial implications and should be reviewed with a pension advisor before leaving Germany.

Personal Liability Insurance (Privathaftpflichtversicherung)

Personal liability insurance is not legally required but is considered the single most important voluntary insurance in Germany. Approximately 80% of German households carry it.

Under German civil law, you are personally liable for all damages you cause to other people or their property, with no statutory cap. A cycling accident that permanently disables someone could make you liable for millions of euros in medical costs, lost earnings, and lifetime pension payments.

What personal liability insurance covers:

- Property damage you cause to others (e.g., water damage from a leaking washing machine)

- Personal injury you cause to others (medical costs, rehabilitation, lost earnings, lifetime pension)

- Financial losses caused to others

- Defence against baseless claims made against you

Cost: €3–15 per month for coverage of €5–10 million or more. Family policies cover all household members. At this price point, it is considered non-negotiable by every financial advisor in Germany.

What it does NOT cover: damage caused by motor vehicles (requires separate car insurance), damage caused by dogs in some states (requires separate dog liability insurance), and professional liability (requires separate Berufshaftpflicht).

Household Contents Insurance (Hausratversicherung)

Household contents insurance covers the value of your personal belongings inside your home against fire, water damage, storms, theft, and vandalism. It is not legally required but is highly recommended, especially for renters.

- Coverage: Furniture, electronics, clothing, appliances, bicycles (with add-on), and other personal possessions.

- Cost: Typically €2.50–€15/month depending on the value insured and your postcode. Digital insurers like Feather and Getsafe offer expat-friendly policies in English.

- Important for renters: In Germany, most rental apartments are unfurnished. Once you invest in furniture and electronics, household contents insurance protects that investment at minimal cost.

Car Insurance for Expats in Germany (Kfz-Versicherung)

If you own or drive a car in Germany, third-party liability car insurance (Kfz-Haftpflichtversicherung) is mandatory. You cannot register a vehicle without providing proof of insurance (an eVB number from your insurer).

Three levels of car insurance exist in Germany:

- Third-party liability (Haftpflicht): Mandatory. Covers damage you cause to other people, vehicles, and property. Does not cover your own vehicle.

- Partial comprehensive (Teilkasko): Covers theft, fire, storm damage, glass breakage, and animal collisions. Recommended for newer vehicles.

- Fully comprehensive (Vollkasko): Covers everything in Teilkasko plus damage to your own vehicle in accidents you cause, including vandalism. Recommended for new or high-value vehicles.

Cost: Ranges from approximately €100 to €1,000+ per year depending on the coverage level, your age, no-claims history (Schadenfreiheitsklasse), vehicle type, and region. Expats arriving without a German driving history typically start at a higher rate.

💡 Employsome Insight: Your No-Claims History from Home May Not Transfer

Germany uses a no-claims bonus system (Schadenfreiheitsklasse) that significantly affects premiums. New drivers and expats without German driving history start at a high rate (SF 0 or SF 1/2). Some insurers accept no-claims certificates from other countries, but this varies. Ask your insurer about transferring your driving history before signing up, as the difference can be hundreds of euros per year.

Other Insurance Expats in Germany Should Consider

Other Insurance Expats in Germany Should Consider

Dental Supplementary Insurance (Zahnzusatzversicherung)

Public health insurance covers basic dental care but provides limited coverage for crowns, bridges, implants, and professional cleaning. Dental supplementary insurance fills this gap, typically costing €10–50/month. This is one of the most popular supplementary policies among expats because out-of-pocket dental costs in Germany can be substantial.

Legal Protection Insurance (Rechtsschutzversicherung)

Covers legal fees, court costs, and attorney fees in disputes related to employment, tenancy, traffic, or contract law. Useful for expats who may face landlord disputes or employment disagreements. Cost: approximately €10–40/month.

Occupational Disability Insurance (Berufsunfähigkeitsversicherung, BU)

Provides a monthly pension if you are unable to work for 6+ months due to illness, injury, or mental health conditions (including burnout and chronic back pain). Germany’s state disability pension (Erwerbsminderungsrente) pays only a fraction of your salary. BU insurance supplements this. Cost: €50–200/month depending on age, profession, and coverage amount. Financial advisors consistently rank BU as one of the most important voluntary insurances in Germany.

Life Insurance (Lebensversicherung)

Term life insurance pays a lump sum to your named beneficiaries if you die. Recommended for expats with dependants. Costs vary widely based on coverage amount, age, and health status.

What Insurance Means for EOR Arrangements in Germany

For international companies hiring in Germany through an Employer of Record (EOR), the mandatory insurance framework creates specific obligations:

- Health insurance: The EOR must register the employee with a public health insurer (if earning below €77,400/year) or verify that the employee has valid private coverage. The employer pays half of GKV contributions or up to €508.59/month toward PKV premiums.

- Long-term care insurance: Automatically bundled with health insurance. The employer pays the 1.7% employer share.

- Pension insurance: The employer contributes 9.3% of gross salary to the statutory pension system.

- Unemployment insurance: The employer contributes 1.3% of gross salary.

- Accident insurance (Berufsgenossenschaft): The employer must register with the relevant professional association and pay the full contribution for workplace accident insurance. This is an employer-only cost that varies by industry.

In total, mandatory employer insurance contributions in Germany add approximately 20–21% on top of gross salary. This is one of the higher employer contribution rates in Europe, though lower than France or Spain.

For a detailed comparison of EOR providers in Germany and how they handle insurance and social security obligations, see our Best Employer of Record in Germany guide. For current minimum wage rates and full payroll contribution breakdowns, see our Minimum Wage in Germany 2026 guide.

💡 Employsome Insight: Not All EOR Providers Handle Insurance Onboarding Equally

Some EOR providers automatically enrol employees in a default public health insurer without giving them a choice. Since GKV contribution rates vary by insurer (the additional contribution ranges from approximately 0.9% to 2.5%), this can cost employees hundreds of euros per year in unnecessary premiums. A good EOR should present health insurance options and allow the employee to select their preferred Krankenkasse. If your EOR does not offer this choice, raise it during onboarding.

Insurance Checklist for Expats Moving to Germany

Use this checklist to ensure you have the right coverage before and after arriving in Germany:

Before Arrival

- Arrange temporary expat health insurance if you do not yet have a German employment contract (required for visa/residence permit applications)

- Obtain a certificate of no-claims history from your current car insurer if you plan to drive in Germany

- Research whether your home country has a social security agreement with Germany (affects pension and health insurance coordination)

First Week in Germany

- Register with a public health insurer (if employed below the €77,400 threshold) or arrange private health insurance

- Provide your health insurance confirmation to your employer or EOR for payroll registration

- Take out personal liability insurance (Haftpflichtversicherung) immediately. Cost: €3–15/month

First Month

- Set up household contents insurance once you have moved into your apartment

- If driving, arrange car insurance and obtain your eVB number for vehicle registration

- Consider dental supplementary insurance, especially if you have a history of dental work

- Register with a general practitioner (Hausarzt) in your neighbourhood

First Three Months

- Review occupational disability insurance (BU) with an advisor, especially if you have a high-salary or specialist role

- Consider legal protection insurance if you are renting (landlord disputes) or in a complex employment situation

- Review your pension situation: are you building toward the 60-month minimum? Does a social security agreement apply?

Final Takeaway – Insurance for Expats in Germany

Germany’s insurance system is comprehensive, well-regulated, and taken seriously by both residents and authorities. For expats, health insurance is the immediate priority since it is required for your residence permit and must be arranged from day one. The choice between public (GKV) and private (PKV) health insurance is the most consequential financial decision you will make as an expat in Germany, with long-term implications for family coverage, premiums in old age, and the ability to switch back.

Beyond health insurance, personal liability insurance (€3–15/month) is universally recommended and should be taken out immediately upon arrival. Household contents insurance, dental supplementary insurance, and occupational disability insurance are the next priorities for most expats. Car insurance is mandatory if you drive. Pension contributions are automatically deducted from your salary if you are employed, and the 5-year minimum for benefit eligibility should factor into your long-term planning.

For international companies hiring in Germany through an EOR, mandatory employer insurance contributions (health, pension, long-term care, unemployment, accident) add approximately 20–21% on top of gross salary. Understanding these costs is essential for accurate budgeting, and ensuring your EOR handles health insurance onboarding properly can save your employees meaningful money over time.

Written by

Dane Cobain is a Copywriter at Employsome and an accomplished author whose work spans fiction, non-fiction, and professional writing. Over the past decade, he has built a strong track record creating straightforward content for the HR, payroll, and corporate sectors. Dane brings a storyteller’s eye to the evolving world of global employment, with a particular focus on Employer of Record and PEO models. His articles explore industry trends and dedicated Best Of Guides when managing an international workforce.

Our content is created for informational purposes only and is not intended to provide any legal, tax, accounting, or financial advice. Please obtain separate advice from industry-specific professionals who may better understand your business’s needs. Read our Editorial Guidelines for further information on how our content is created.