Health Insurance in China 2026: UEBMI & Employer Costs

Health insurance in China operates under the mandatory “5+1” social insurance framework with employer contributions of 9.8-10% of gross salary and employee contributions of 2% plus medical savings. The main scheme, Urban Employee Basic Medical Insurance (UEBMI), is compulsory for all formally employed workers including foreign nationals. This 2026 guide covers UEBMI coverage and reimbursement, contribution rates by city, foreign worker rules, hospital tiers, and commercial supplementary insurance like Shanghai’s Huhuibao.

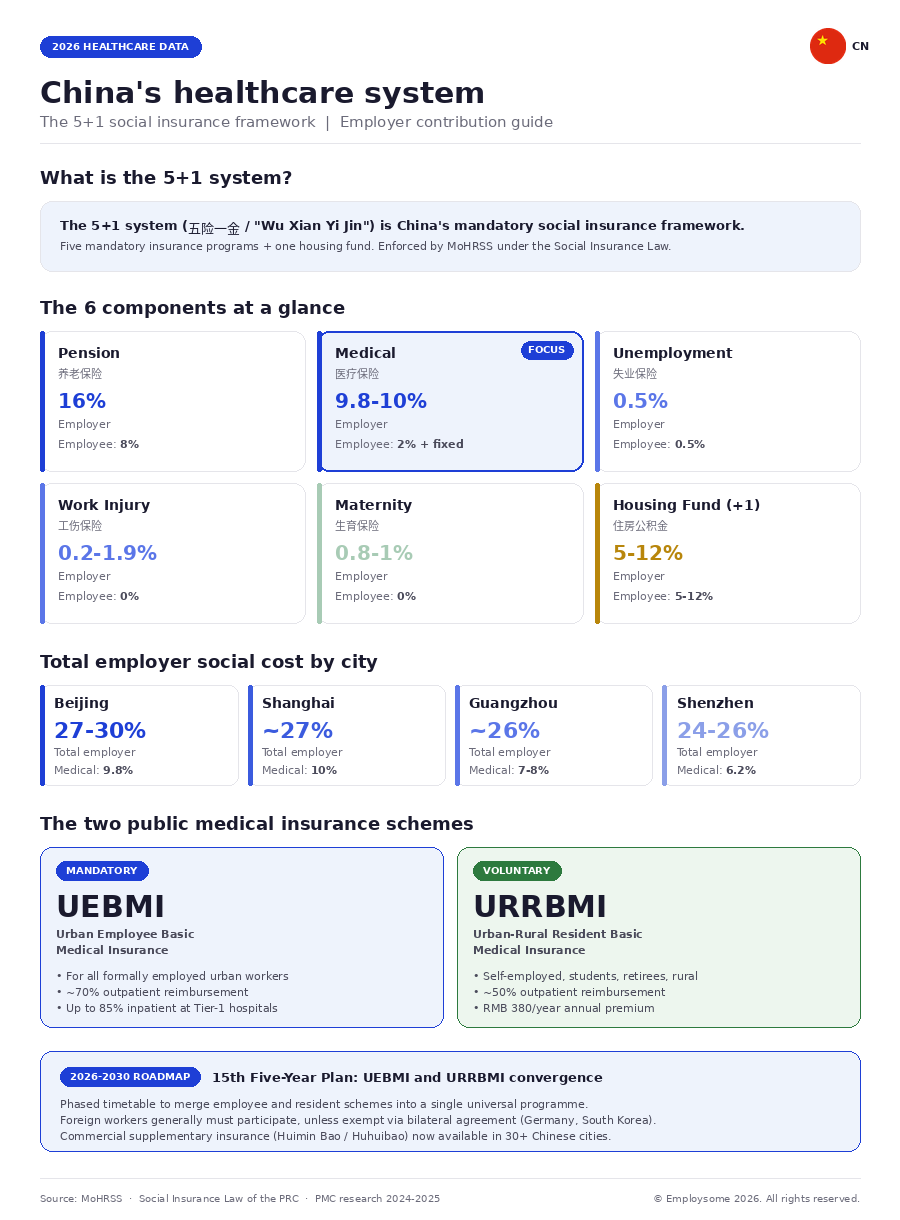

Health insurance in China operates under a mandatory public system run through the “5+1” social insurance framework: Pension, Medical, Unemployment, Work Injury, Maternity, plus the Housing Fund. Medical insurance is administered by the Ministry of Human Resources and Social Security (MoHRSS) and enforced under the Social Insurance Law, with employer contributions averaging 9.8% to 10% of gross salary and employee contributions of 2% plus a fixed medical savings amount.

China’s public health insurance system is built around two main schemes. The Urban Employee Basic Medical Insurance (UEBMI) is mandatory for all formally employed urban workers, including foreign nationals unless covered by a bilateral social security agreement. The Urban and Rural Resident Basic Medical Insurance (URRBMI) is a voluntary scheme that covers the unemployed, children, students, retirees without UEBMI coverage, and rural residents. UEBMI reimbursement rates average 70% for outpatient treatment, while URRBMI covers approximately 50%.

This 2026 guide covers how health insurance works in China for employers and employees, the structure of UEBMI and URRBMI, detailed contribution rates for Beijing and Shanghai, rules for foreign workers, reimbursement levels by hospital tier, commercial supplementary insurance schemes like Shanghai’s Huhuibao (Huimin Bao), and what international companies hiring through an Employer of Record (EOR) need to understand about medical insurance obligations in China.

China’s Healthcare System: The 5+1 Framework

China’s national healthcare system is organised around the “5+1” social insurance system (五险一金), which combines five mandatory insurance programs with a housing savings fund. All enterprises operating in China must enrol their employees in this framework.

| Insurance Type | Employer Contribution | Employee Contribution |

| Pension Insurance (养老保险) | ~16% (varies by region) | 8% |

| Medical Insurance (医疗保险) | ~9.8%-10% | 2% + fixed medical savings |

| Unemployment Insurance (失业保险) | ~0.5% | ~0.5% |

| Work Injury Insurance (工伤保险) | 0.2%-1.9% (by industry risk) | 0% (fully employer-funded) |

| Maternity Insurance (生育保险) | ~0.8%-1% (merged with medical in some regions) | 0% |

| Housing Fund (住房公积金) (+1) | 5%-12% (matched by employee) | 5%-12% |

Medical insurance (医疗保险) is the largest employer contribution after pension, and it is the category that directly pays for healthcare services. It splits into two main public schemes:

- UEBMI (Urban Employee Basic Medical Insurance): Mandatory for all formally employed urban workers. Covers hospitalisation, outpatient services, prescription drugs, critical illness, and maternity (in many cities). Reimbursement rate ~70% for outpatient, up to 85% for inpatient at designated hospitals.

- URRBMI (Urban-Rural Resident Basic Medical Insurance): Voluntary scheme for the self-employed, students, children, retirees without UEBMI coverage, and rural residents. Annual premium RMB 380 (2024 figure, subject to annual revision). Reimbursement rate ~50% for outpatient, 60-75% for inpatient.

The URRBMI replaced two earlier schemes (URBMI and NRCMS) via a 2016 State Council integration policy. China’s 15th Five-Year Plan (2026-2030) sets out a timetable to progressively converge UEBMI and URRBMI into a single universal programme, although full unification is not expected before 2030.

Medical Insurance Contribution Rates by City (2026)

The specific medical insurance contribution rates in China vary by region, with Tier-1 cities (Beijing, Shanghai, Guangzhou, Shenzhen) setting their own rates within the national framework. Employers are required to contribute based on the employee’s gross monthly salary, subject to both floor and ceiling caps tied to the local average wage.

| City | Employer Medical | Employee Medical | Total Employer Social Cost |

| Beijing | 9.8% | 2% + RMB 3 | ~27-30% of gross |

| Shanghai | 10% | 2% | ~27% of gross |

| Guangzhou | ~7-8% | 2% | ~26% of gross |

| Shenzhen | ~6.2% | 2% | ~24-26% of gross |

The total employer social cost in China includes medical plus pension, unemployment, work injury, maternity, and the housing fund. In Beijing, the total employer burden reaches 27-30% of gross salary, with employees paying approximately 10-12%. In Shanghai, employers contribute around 27% and employees approximately 11%.

Contribution base caps: Each city sets a minimum contribution base (typically 60% of the prior year’s average wage) and a ceiling (typically 300% of the average wage). Very high earners do not pay medical insurance on the full salary – contributions are capped at the city ceiling. Very low earners contribute on the floor rather than actual wages.

Medical savings component: In addition to the pooled contributions used for shared medical costs, Chinese medical insurance includes a personal medical savings account. A portion of the employer’s contribution plus the full 2% employee contribution is deposited into this personal account, which the employee can use for outpatient visits, pharmacy purchases, and deductibles.

💡 Employsome Insight: True Employer Cost in China Is 27-30% Above Gross Salary

Total employer cost in China is often underestimated by international companies. Gross salary is only the starting point – medical insurance, pension, housing fund, and other contributions add roughly 27-30% on top in Beijing and 27% in Shanghai. For a RMB 30,000 per month employee in Beijing, the true employer cost is approximately RMB 38,000-39,000 monthly when all contributions are included. Budget accordingly when comparing China compensation packages to other markets.

How UEBMI Works: Coverage, Reimbursement, and Hospital Tiers

UEBMI is China’s most comprehensive public insurance scheme and forms the backbone of employer-sponsored healthcare coverage. It is mandatory for all formally employed urban workers, enforced under the Social Insurance Law by MoHRSS.

UEBMI covers:

- Inpatient hospitalisation at designated public hospitals

- Outpatient services including specialist consultations and diagnostics

- Prescription drugs on the National Reimbursement Drug List

- Critical illness treatment including chronic conditions and cancer

- Maternity expenses in cities where maternity and medical insurance are merged

- Traditional Chinese Medicine (TCM) at designated providers

Reimbursement structure: UEBMI reimbursement is tiered by hospital grade and service type. Primary care and lower-tier hospitals have lower co-payment percentages than tertiary-grade hospitals, which is deliberate policy to direct demand toward community-level care.

| Service Type | UEBMI Reimbursement | URRBMI Reimbursement |

| Outpatient (Tier 1 hospital / community) | ~80% | ~55% |

| Outpatient (Tier 2 hospital) | ~70% | ~50% |

| Outpatient (Tier 3 hospital) | ~60% | ~45% |

| Inpatient (Tier 1 hospital) | ~85% | ~75% |

| Inpatient (Tier 2 hospital) | ~80% | ~65% |

| Inpatient (Tier 3 hospital) | ~70% | ~55% |

| Prescription drugs (on list) | ~70-85% | ~50-65% |

Deductibles and caps: UEBMI operates with deductibles (roughly 3% of the employee’s annual salary) and an annual coverage ceiling of approximately six times the employee’s annual salary. Costs above the ceiling fall outside UEBMI coverage, which is why commercial supplementary insurance has become increasingly common for high-earning urban employees and foreign workers.

Retiree coverage: UEBMI continues to provide coverage after retirement for workers who have contributed for a minimum qualifying period (typically 15-25 years of contributions, with local variations). Retiree co-payments are approximately half those of currently-employed workers, significantly reducing the financial burden on older residents.

Health Insurance for Foreign Workers in China

Enrolment rules for foreign workers have tightened significantly in recent years. Under current MoHRSS guidance, foreign employees working legally in China are generally required to participate in the full 5+1 social insurance system, including UEBMI medical insurance, unless they qualify for an exemption under a bilateral social security agreement.

Bilateral exemption countries: Workers from certain countries benefit from social security agreements with China that may exempt them from specific contribution categories. Confirmed exemption arrangements include:

- Germany: Exemption covering pension and unemployment insurance contributions

- South Korea: Exemption covering pension contributions

- Selected other countries: Various partial exemption arrangements

Even in exemption countries, medical insurance contributions are typically still required. Foreign workers with exemptions should obtain a formal certificate from their home country social security authority and submit it to their Chinese employer for registration with the local social insurance bureau.

Digital social insurance cards: Foreign workers registered in the Chinese system now access their social insurance records through an electronic social insurance card on a mobile app, which displays work permit information and allows direct billing at participating hospitals. Physical cards have been phased out in most major cities.

Practical limitations for foreigners:

- Language barriers at many public hospitals (English typically only available at VIP wings of top Tier-1 city hospitals)

- Visa status is usually tied to the sponsoring employer, which complicates claiming unemployment benefits after job loss

- Pension entitlement requires 15+ years of aggregate contributions before retirement age, which many foreign workers never reach

- Public hospital wait times in major cities can be substantial, driving demand for private international clinics

💡 Employsome Insight: Commercial Supplementary Insurance Is Market Standard for Expats in Tier-1 Cities

For expat-heavy international companies hiring in Tier-1 Chinese cities, commercial supplementary insurance is effectively market standard, not optional. Public UEBMI coverage fully satisfies the legal contribution requirement, but practical access to English-speaking doctors, VIP wings, and international clinics like Beijing United Family Hospital or Shanghai’s Parkway Health requires either substantial out-of-pocket spending or a commercial expat plan. Most multinational employers in Beijing and Shanghai budget RMB 20,000-60,000 per employee per year for supplementary coverage on top of the statutory social insurance contribution.

Hospital Tiers and Costs in China

Chinese hospitals are organised into a three-tier grading system, and understanding it is essential for anyone using the public insurance system. The tier determines reimbursement rates, quality of care, cost, and the likely availability of English-speaking staff.

| Hospital Tier | Description | Typical Use | English Availability |

| Tier 1 (Primary / Community) | Local community health centres, township hospitals | Basic primary care, minor conditions, prescription refills | Very rare |

| Tier 2 (Secondary) | Mid-size district or city hospitals | Specialist consultations, mid-complexity inpatient care | Occasional |

| Tier 3 (Tertiary) | Major provincial and teaching hospitals | Advanced surgery, specialist treatment, critical care | VIP wings only, mostly in Tier-1 cities |

| Private International Hospitals | Beijing United Family, Parkway Health, Jiahui, etc. | International-standard care for expats and wealthy residents | Standard English |

Cost differences by hospital type and city:

- Public hospital, general ward: Covered heavily by UEBMI; out-of-pocket varies by tier and service

- Public hospital, VIP wing: UEBMI partial coverage (10-30%); remainder paid privately or by commercial insurance

- Private international hospital: UEBMI rarely applies; a general consultation at Parkway Health in Shanghai costs approximately USD 225. Emergency room care at Beijing United Family Hospital ranges from USD 276 to USD 591. Inpatient surgery can range from USD 765 to USD 22,500 depending on complexity.

- Tier-1 city premium: Medical costs in Beijing, Shanghai, Guangzhou, and Shenzhen are 30-50% higher than the national average. Tier-2 cities (Hangzhou, Suzhou, Nanjing) are 10-30% lower than Tier-1 but above national average.

The national emergency medical services number in China is 120, equivalent to 999 or 911, and it is available nationwide. Non-emergency consular assistance for foreign residents should be obtained through the relevant embassy or consulate, which maintain lists of recommended hospitals in major cities.

Commercial Supplementary Insurance: Huimin Bao and Private Plans

Commercial supplementary insurance has expanded rapidly in China as public insurance ceilings prove insufficient for many urban employees, especially those using private or Tier-3 hospitals. Supplementary options fall into two main categories.

Government-backed city schemes (Huimin Bao / Huhuibao): City-level supplementary commercial insurance schemes designed to cover catastrophic medical costs exceeding the public insurance ceiling. Launched in Shanghai as Huhuibao (沪惠保) in 2021, the model has since spread to dozens of Chinese cities. Key features:

- Premiums very low, typically RMB 100-200 per year

- Available to all residents enrolled in the local basic medical insurance (including eligible foreign residents)

- Focuses on hospitalisation expenses, specific high-priced drugs, and proton/heavy-ion cancer treatments

- Reimburses costs above the UEBMI ceiling not covered by the public scheme

- Does not screen pre-existing conditions

Private commercial health insurance for expats and executives: Full private plans from international and domestic insurers, providing broader access to private hospitals, English-speaking doctors, and international-standard care. Common providers in China include AXA, Cigna, Bupa, APRIL International, and domestic insurers like PICC Health and Ping An. Typical features:

- Annual premiums range from RMB 15,000 (basic local plan) to RMB 60,000+ (comprehensive international plan with overseas coverage)

- Direct billing at network hospitals (Beijing United Family, Parkway Health, Jiahui, Vista SK, etc.)

- Coverage for outpatient, inpatient, maternity, dental, vision, and mental health (plan-dependent)

- Emergency evacuation and repatriation for serious cases

- Pre-existing condition coverage typically requires underwriting

For international employers, commercial supplementary insurance is typically offered as a benefit for executive-level roles and for expat employees in Tier-1 cities. Chinese national hires in Tier-2 or Tier-3 cities often rely primarily on UEBMI with only the government-backed Huimin Bao top-up, which keeps benefits cost manageable.

Hiring in China Through an Employer of Record

For international companies hiring in China without a local entity, an Employer of Record (EOR) handles all aspects of international hiring compliance including health insurance enrolment as part of the standard 5+1 social insurance administration. The EOR serves as the formal employer, which means it is responsible for all statutory contributions and must maintain local social insurance registrations.

A China EOR handles:

- Registration of each employee with the local social insurance bureau (covering UEBMI, pension, unemployment, work injury, maternity)

- Monthly calculation and remittance of medical insurance contributions within city-specific base/ceiling rules

- Housing fund deposits (varies 5-12% matched)

- Payroll tax withholding and reporting via the local tax authority

- Issuance of digital social insurance cards to employees

- Management of any bilateral exemption certificates for foreign employees

- Optional commercial supplementary insurance coordination for executive or expat hires

Regional considerations: Chinese EORs must be registered in each specific city or province where they hire, because social insurance rates and caps vary by jurisdiction. A single national-level EOR licence does not automatically cover all cities. When evaluating a China EOR, confirm:

- Registered presence and active social insurance account in each Tier-1 city where you plan to hire

- Published contribution rates for each city, showing medical, pension, housing fund, and other components separately

- Written policy on commercial supplementary insurance options (Huimin Bao coordination or private plan procurement)

- Track record with foreign employee registrations, including bilateral exemption handling

- Reporting cadence for social insurance clearance certificates

What International Employers Need to Know

Budget for total employer cost, not gross salary

Chinese employer social contributions add approximately 27-30% on top of gross salary in Beijing and 27% in Shanghai. Medical insurance alone is roughly 9.8-10% in Tier-1 cities, plus pension (~16%), housing fund (5-12%), and smaller amounts for unemployment, work injury, and maternity.

Factor in commercial supplementary insurance for expat hires

For expat employees and executive-level roles in Tier-1 cities, commercial supplementary health insurance is effectively market standard. Budget RMB 20,000-60,000 per employee per year depending on plan level, with comprehensive international plans at the higher end.

Understand bilateral exemption rules carefully

Only workers from certain countries (Germany, South Korea, and others with specific agreements) qualify for partial exemptions, and medical insurance is typically still required even when other categories are exempted. Always obtain formal exemption certificates from the home country authority before registration.

Use the hospital tier system strategically

UEBMI reimbursement rates are higher at Tier-1 and Tier-2 hospitals than at Tier-3 facilities, reflecting China’s policy to direct demand toward community-level care. Routine care at Tier-1 community hospitals is heavily subsidised; specialist care and Tier-3 treatment costs more out-of-pocket.

Watch for the 15th Five-Year Plan reforms (2026-2030)

China’s central policy plan sets out convergence of UEBMI and URRBMI into a single universal programme by 2030. Expect gradual adjustments to contribution rates, reimbursement structures, and coverage catalogues during this period. Employers should monitor MoHRSS and local bureau announcements for annual rate updates.

Engage a specialist for Tier-1 city tax and insurance setup

Beijing, Shanghai, Guangzhou, and Shenzhen each have different social insurance bases, ceilings, and local rules. Use an EOR with direct registration in each target city, or engage a local Chinese payroll specialist for each jurisdiction rather than attempting to run a single centralised payroll.

Hiring in China?

China’s 5+1 social insurance system adds roughly 27-30% to gross salary across medical, pension, and housing fund contributions, with city-level variations and mandatory coverage for most foreign workers. Navigating Tier-1 city rates and commercial supplementary insurance requires local expertise. Compare the top Employer of Record providers for China in 2026 – verified pricing, compliance scores, and expert rankings from Employsome’s independent research team.

Frequently Asked Questions

Health insurance in China is a mandatory social insurance programme administered by the Ministry of Human Resources and Social Security (MoHRSS). The main scheme is Urban Employee Basic Medical Insurance (UEBMI), with employer contributions averaging 9.8-10% of gross salary and employee contributions of 2% plus a fixed medical savings amount. A separate voluntary scheme, Urban-Rural Resident Basic Medical Insurance (URRBMI), covers the unemployed, students, children, and rural residents. UEBMI is part of China’s broader “5+1 system” alongside pension, unemployment, work injury, maternity insurance, and the housing fund.

Employer medical insurance contributions in China range from approximately 6% to 10% of the employee’s gross salary, depending on the city. Beijing employers contribute 9.8%, Shanghai employers 10%, Guangzhou 7-8%, and Shenzhen approximately 6.2%. These rates apply to the employee’s contribution base, which is subject to city-specific floor (typically 60% of local average wage) and ceiling (typically 300% of local average wage) caps. Total employer social cost including all 5+1 contributions averages 27-30% of gross salary in Tier-1 cities.

UEBMI (Urban Employee Basic Medical Insurance) is China’s primary mandatory health insurance scheme for formally employed urban workers. Established in 1998, it is administered through local social insurance bureaus under MoHRSS oversight. UEBMI covers inpatient hospitalisation, outpatient services, prescription drugs on the National Reimbursement List, critical illness treatment, and traditional Chinese medicine at designated providers. Reimbursement rates average around 70-85% for outpatient care and 70-85% for inpatient care, varying by hospital tier, with higher reimbursement at lower-tier community hospitals.

Yes. Foreign employees working legally in China are generally required to participate in the full 5+1 social insurance system, including UEBMI medical insurance, unless they qualify for an exemption under a bilateral social security agreement. Workers from Germany and South Korea benefit from partial exemptions (typically covering pension and, for Germany, unemployment insurance), but medical insurance contributions are usually still required. Foreign workers receive a digital social insurance card accessed through a mobile app, which provides the same coverage as Chinese national workers.

Huimin Bao (惠民保) is a city-level, government-backed supplementary commercial insurance programme designed to cover catastrophic medical costs that exceed the public insurance ceiling. Shanghai’s version, called Huhuibao (沪惠保), was launched in 2021 and the model has since spread to dozens of cities. Premiums are very low (typically RMB 100-200 per year) and the scheme is available to all residents enrolled in the local basic medical insurance, including eligible foreign residents. It focuses on hospitalisation expenses, high-priced drugs, and proton or heavy-ion cancer treatments.

UEBMI reimbursement rates vary by hospital tier and service type. Outpatient reimbursement averages approximately 70%, with higher rates at community or Tier-1 hospitals (around 80%) and lower rates at Tier-3 tertiary hospitals (around 60%). Inpatient reimbursement ranges from approximately 70% at Tier-3 hospitals to 85% at Tier-1 hospitals. Prescription drugs on the National Reimbursement Drug List are covered at 70-85%. UEBMI operates with deductibles averaging 3% of annual salary and an annual ceiling of approximately six times the employee’s annual salary.

Private health insurance is not legally required in China – UEBMI enrolment satisfies the mandatory social insurance obligation. However, commercial supplementary insurance is effectively market standard for expat employees and executive-level roles in Tier-1 cities. This is because public hospitals often have long wait times, English is rarely available outside VIP wings of major Tier-1 city hospitals, and international clinics like Parkway Health or Beijing United Family Hospital are not covered by UEBMI. Typical annual premiums range from RMB 15,000 to RMB 60,000+ depending on plan comprehensiveness.

Yes. An Employer of Record (EOR) with registered social insurance accounts in the relevant Chinese cities can fully administer health insurance contributions and the broader 5+1 social insurance obligations on behalf of an international client company. The EOR serves as the formal legal employer, handles monthly contributions to UEBMI and all other statutory insurances, manages housing fund deposits, and coordinates commercial supplementary insurance where required. Because rates and rules vary by city, the EOR must have specific registrations in each Tier-1 city (Beijing, Shanghai, Guangzhou, Shenzhen) where hiring occurs.

Written by

Dane Cobain is a Copywriter at Employsome and an accomplished author whose work spans fiction, non-fiction, and professional writing. Over the past decade, he has built a strong track record creating straightforward content for the HR, payroll, and corporate sectors. Dane brings a storyteller’s eye to the evolving world of global employment, with a particular focus on Employer of Record and PEO models. His articles explore industry trends and dedicated Best Of Guides when managing an international workforce.

Our content is created for informational purposes only and is not intended to provide any legal, tax, accounting, or financial advice. Please obtain separate advice from industry-specific professionals who may better understand your business’s needs. Read our Editorial Guidelines for further information on how our content is created.