EOR Funding & M&A Report 2026: $3.5B Invested and 7 Deals That Reshaped the Industry

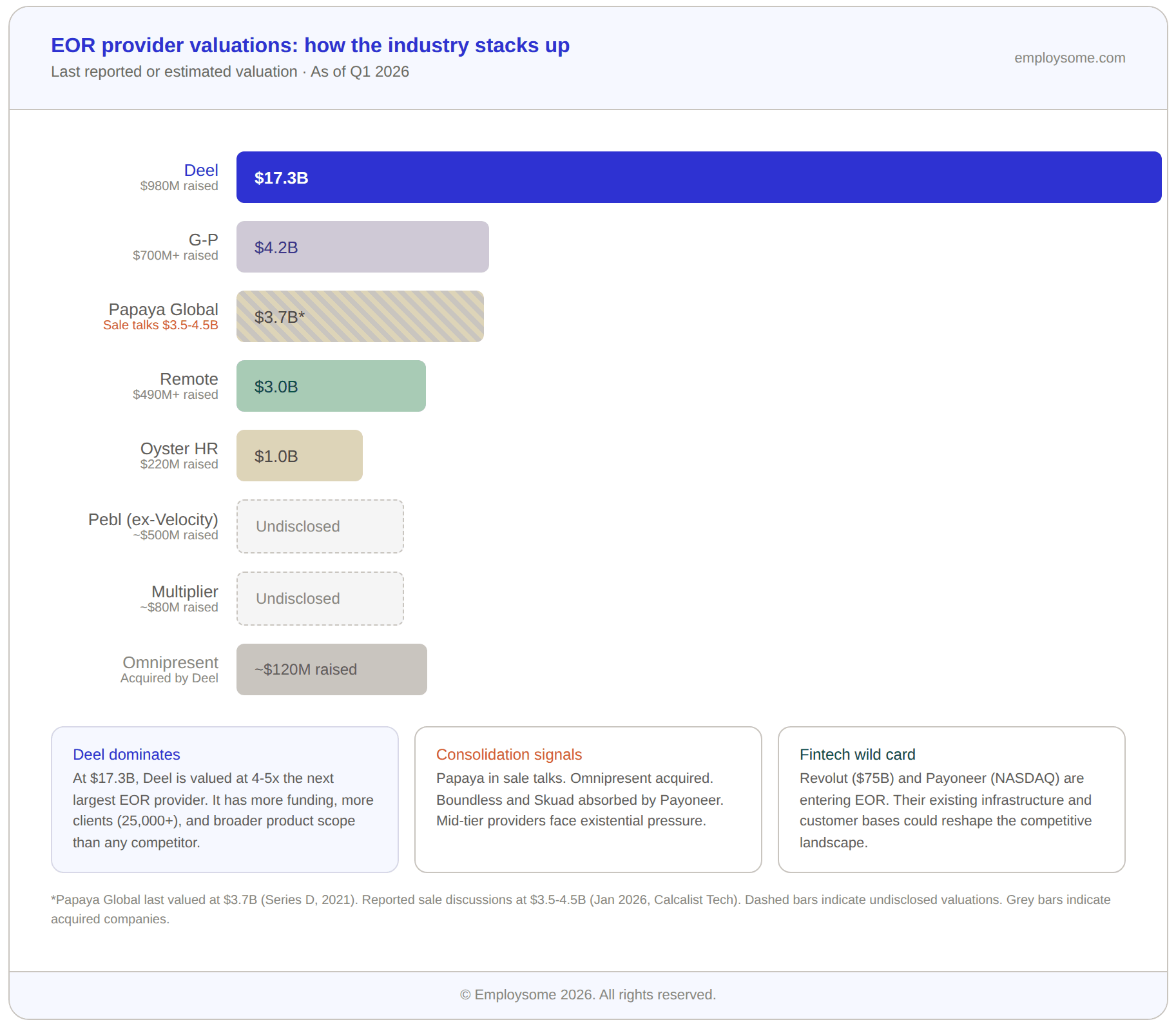

The Employer of Record industry has entered a phase of rapid consolidation. Between 2024 and 2026, the EOR space saw more M&A activity than in the entire previous decade combined. Deel reached a $17.3 billion valuation on over $980 million in total funding and acquired Omnipresent. Payoneer made two back-to-back EOR acquisitions: Skuad for $61 million in 2024 and Boundless in January 2026. Velocity Global rebranded as Pebl. Revolut announced its EOR entry with GlobalHire. Remote acquired Atlas expense management. Hightekers acquired Eos Global Expansion. And Papaya Global entered sale discussions at a reported $3.5-4.5 billion valuation. This tracker maps every major funding round, acquisition, rebrand, and market entry in the EOR industry from 2019 to 2026, and analyses what the consolidation wave means for employers choosing an EOR provider.

Table of Contents

- The Complete EOR Funding & M&A Timeline

- 2019-2021: The Foundation Phase

- 2022-2023: The Correction

- 2024: Fintech Enters the EOR Space

- 2025: The Consolidation Accelerates

- January 2026: Two Deals in One Week

- Cumulative Funding: The EOR Industry by the Numbers

- The Key Themes Driving EOR Consolidation

- What This Means for Companies Choosing an EOR

- What Comes Next: Five Predictions for the EOR Industry

- FAQs

The Employer of Record industry is consolidating faster than almost anyone predicted. What began as a fragmented market of small compliance providers has, in the space of five years, transformed into a multi-billion dollar industry dominated by a handful of heavily funded platforms, with fintech giants and publicly listed companies now entering the space.

Between 2024 and 2026, the EOR market saw more M&A activity than in the entire previous decade combined. Deel acquired a struggling competitor. Payoneer made two consecutive EOR acquisitions. Revolut, valued at $75 billion, announced its entry into the market. Velocity Global underwent a complete rebrand. And one of the industry’s most valuable players entered sale discussions at a valuation nearly 10x its last funding round.

This article tracks every significant funding round, acquisition, merger, rebrand, and market entry in the Employer of Record space from the industry’s modern formation in 2019 through to April 2026. It is designed as a living reference for HR leaders, investors, analysts, and EOR buyers who need to understand how the competitive landscape is shifting and what it means for the providers they work with.

For context on the overall market opportunity driving this activity, the global EOR market was valued at approximately $5.0 billion in 2026 and is projected to reach $15-20 billion by the mid-2030s, depending on the source. For a deeper analysis of market sizing, growth drivers, and regional breakdowns, see our EOR market size and trends report.

![]()

The Complete EOR Funding & M&A Timeline

EOR Industry Funding by Year: The Boom and Correction

Based on publicly reported funding rounds across all major EOR providers, total annual investment in the Employer of Record industry followed a dramatic arc:

|

Year |

Estimated Total EOR Funding |

Key Deals |

Deal Count |

|

2019 |

~$50M |

Deel seed/Series A, Remote seed, Boundless seed |

5+ |

|

2020 |

~$250M |

Deel Series B+C ($186M), Remote Series A, Oyster seed, Multiplier seed |

8+ |

|

2021 |

~$2,000M |

Deel Series D+extension ($581M), Remote Series B+C ($450M), Papaya Series C+D ($350M), Velocity Global ($400M), Oyster Series B+C ($200M) |

15+ |

|

2022 |

~$300M |

Multiplier Series B ($60M), Oyster extension, smaller rounds across mid-tier providers |

10+ |

|

2023 |

~$150M |

Smaller rounds, bridge financing, early M&A signals |

8+ |

|

2024 |

~$100M + M&A |

Payoneer/Skuad ($61M acquisition), RemoFirst rounds, product-led growth phase |

5+ |

|

2025 |

M&A dominated |

Deel/Omnipresent acquisition, Hightekers/Eos acquisition, Pebl rebrand, Revolut GlobalHire announced |

4+ major deals |

|

2026 YTD |

M&A dominated |

Payoneer/Boundless acquisition, Remote/Atlas acquisition, Papaya sale talks |

3+ major deals |

The pattern is clear. 2021 was the peak, with approximately $2 billion flowing into EOR providers in a single year, driven by the remote work boom and abundant venture capital. By 2022-2023, new funding had dropped by 85-90% as interest rates rose and investors demanded profitability over growth. From 2024 onward, capital entered the EOR space primarily through M&A rather than venture rounds, as established companies (Payoneer, Revolut) acquired EOR capabilities rather than EOR startups raising independent funding.

The total capital invested in the EOR industry since 2019 exceeds $3.5 billion in venture and growth funding, plus an undisclosed amount in M&A deal value.

![]()

2019-2021: The Foundation Phase

The modern EOR industry was born during this period. Remote work was already growing before COVID-19, but the pandemic accelerated adoption by years. Venture capital flooded into the space as investors recognised that distributed work was a permanent shift, not a temporary trend.

Deel was founded in 2019 by Alex Bouaziz, Shuo Wang, and Ofer Simon. The company raised aggressively from the start, completing its Series A ($14M) in 2020 and quickly following with a Series B ($30M) and Series C ($156M) in the same year. By April 2021, Deel had raised a $156M Series D at a $1.25 billion valuation, reaching unicorn status in under two years. Just five months later, in October 2021, Deel closed a $425M Series D extension that pushed its valuation to $5.5 billion. Total funding by end of 2021: approximately $630 million.

Remote was founded in 2019 by Job van der Voort and Marcelo Lebre. The company raised a $150M Series B in July 2021 at a $1 billion valuation, followed rapidly by a $300M Series C in October 2021 at a $3 billion valuation. Remote’s approach emphasised owned entities over partner models, positioning it as the compliance-first alternative to Deel’s speed-first model.

Papaya Global raised its $250M Series D in September 2021 at a $3.7 billion valuation, the largest single round in the EOR/global payroll space at that time. Founded in 2016 by Eynat Guez, Ruben Drong, and Ofer Herman, Papaya had previously raised a $100M Series C in March 2021. Total funding exceeded $440 million by end of 2021. Papaya used this capital to acquire NickNack (workplace connectivity) and Azimo (global payments), expanding its infrastructure beyond pure EOR.

Velocity Global raised $400M in a growth round led by General Atlantic in 2021, building on earlier funding that brought total investment to approximately $500 million. Founded in 2014 by Ben Wright in Denver, Velocity Global positioned itself as the enterprise-grade EOR with the widest country coverage.

Oyster HR raised a $150M Series C in April 2022 at a $1 billion valuation, following a $50M Series B in June 2021. Founded in 2020, Oyster positioned itself as the mission-driven EOR focused on distributed employment.

Multiplier raised a $60M Series B in early 2022, building on previous rounds totalling approximately $20M. Founded in 2020 in Singapore, Multiplier focused on the Asia-Pacific market before expanding globally.

RemoFirst raised $39M across multiple rounds. Founded in 2021, the company positioned itself as the budget alternative to Deel and Remote with pricing starting at $199/month per employee.

The 2019-2021 period represented the peak of EOR venture funding. Over $2 billion in venture capital flowed into the top EOR providers in approximately 24 months. This capital funded rapid entity expansion, platform development, and aggressive customer acquisition.

2022-2023: The Correction

The venture funding boom of 2021 was followed by a sharp correction. Rising interest rates, tech layoffs, and a broader pullback in SaaS spending created headwinds for EOR providers that had grown headcount and burned cash aggressively.

Deel continued to grow through this period, adding product lines (HRIS, IT equipment, immigration), expanding its entity footprint, and reaching over 25,000 corporate clients by mid-2023. The company reportedly reached profitability or near-profitability during this period, a rarity in the space.

Papaya Global acquired Azimo, a global payments company, to strengthen its cross-border payment infrastructure. This was a strategic pivot from pure EOR toward becoming an integrated payments and payroll platform.

Omnipresent, a London-based EOR provider that had raised approximately $120M in total funding (including a $100M Series B in 2021), began experiencing financial pressure. Industry sources later confirmed that the company’s burn rate was unsustainable in the post-2021 funding environment.

G-P (Globalization Partners), one of the EOR industry’s pioneers, went through leadership changes and strategic repositioning. The company had raised over $700M in total funding at a reported $4.2 billion valuation but faced increasing competitive pressure from faster-growing, lower-priced providers.

The key dynamic of 2022-2023 was the divergence between well-capitalised leaders and struggling mid-tier players. Deel and Remote continued growing. Papaya pivoted toward payments infrastructure. But several providers that had raised large rounds in 2021 found themselves unable to sustain growth without additional funding that was no longer available on favourable terms.

2024: Fintech Enters the EOR Space

2024 marked a turning point: the EOR industry moved from venture-funded growth to strategic M&A driven by large, established fintech and payments companies.

Payoneer acquires Skuad ($61M, August 2024)

Payoneer (NASDAQ: PAYO), the publicly listed fintech company with a global payments platform serving millions of customers, acquired Singapore-based EOR provider Skuad for $61 million in cash. Skuad, founded in 2019, had raised approximately $20M in venture funding and offered EOR services across 85+ countries.

This was the first time a publicly listed fintech company acquired an EOR provider. It signalled that EOR was moving from a standalone HR tech category into a component of broader financial infrastructure for cross-border businesses. Payoneer rebranded Skuad as Payoneer Workforce Management (WFM) and began integrating it into its existing payments and financial services platform. For a detailed analysis of how Payoneer’s acquisition strategy is reshaping the EOR market, see our coverage of the Payoneer Boundless acquisition.

Deel continues product expansion

Deel expanded beyond EOR into a full HR operating system, launching Deel HR (free HRIS), Deel IT (equipment provisioning), Deel Engage (performance management), and Deel Immigration. By end of 2024, Deel’s total funding exceeded $980 million across seven rounds, with a valuation of $17.3 billion. The company operated in 150+ countries through predominantly owned entities.

Remote raises additional funding

Remote continued building its owned-entity model and expanded product lines to include global payroll for companies with their own entities, contractor management, and equity administration. Total funding exceeded $490 million.

2025: The Consolidation Accelerates

2025 was the year the EOR industry definitively shifted from a growth-at-all-costs market to a consolidation market. Multiple acquisitions, a major rebrand, and a landmark fintech entry reshaped the competitive landscape.

Deel acquires Omnipresent (October 2025)

Deel acquired Omnipresent, the London-based EOR provider that had raised approximately $120M in total funding. Industry sources indicate this was not a traditional strategic acquisition. Omnipresent was facing severe financial pressure, and the acquisition was effectively a rescue deal. The company had been unable to sustain its burn rate in the post-2021 funding environment and was running out of options.

This deal removed a significant mid-tier competitor from the market and added Omnipresent’s customer base and European entity infrastructure to Deel’s portfolio. It also sent a clear signal to the industry: EOR providers that raised large rounds in 2021 but failed to reach sustainable economics were now vulnerable to acquisition or closure.

Velocity Global rebrands as Pebl (September 2025)

Velocity Global, which had raised approximately $500 million in total funding and operated in 185+ countries, underwent a complete rebrand to Pebl. The rebrand was more than cosmetic. It represented a strategic repositioning from a service-led enterprise EOR toward an AI-powered hiring platform, with a new AI assistant called Alfie operating in 50+ languages.

The rebrand signalled that Velocity Global’s leadership believed the company needed a fundamentally different market position to compete against Deel, Remote, and the incoming fintech players. Whether the repositioning succeeds remains to be seen. The company retains one of the broadest entity footprints in the industry.

Hightekers acquires Eos Global Expansion (April 2025)

Hightekers, a French-headquartered European EOR and consulting company, acquired Eos Global Expansion, an APAC-focused EOR provider with over 20 years of operating history. The combined entity brings together Hightekers’ European strength with Eos’s Asia-Pacific expertise, creating a 25-country footprint with approximately 140 professionals.

This deal illustrates a different type of consolidation: regional specialists merging to create broader geographic coverage rather than massive platforms absorbing smaller competitors. For a detailed breakdown, see our Hightekers-Eos acquisition.

Revolut announces GlobalHire EOR entry (2025)

Perhaps the most significant market entry in EOR history: Revolut, the $75 billion fintech with 65 million customers and legal entities in 39 countries, announced its EOR product GlobalHire, set to launch covering 160 countries.

Revolut’s entry is fundamentally different from any previous EOR market entry. The company already has global payments infrastructure, established legal entities, regulatory licences, and a massive existing customer base of businesses that could become EOR clients through cross-selling. It also has the capital to price aggressively and subsidise EOR with revenue from other financial services.

The companies most threatened by Revolut’s entry are not the market leaders (Deel, Remote, and Rippling have sufficient scale and differentiation to compete) but rather small to medium EOR providers already struggling with margin compression and limited differentiation. For a deep analysis of what GlobalHire means for the industry, see our Revolut GlobalHire analysis.

Papaya Global enters sale discussions ($3.5-4.5B valuation)

In January 2026, Calcalist Tech reported that Papaya Global had entered sale discussions at a reported valuation of $3.5 to $4.5 billion. The company, which had raised over $440 million and was last valued at $3.7 billion in its 2021 Series D, had pivoted from pure EOR toward an integrated workforce payments platform.

The reported sale discussions suggest that Papaya’s leadership and investors may have concluded that remaining independent in an increasingly consolidated market dominated by Deel and challenged by fintech entrants is not the optimal path forward. The outcome of these discussions has not been publicly confirmed.

January 2026: Two Deals in One Week

The first month of 2026 saw two significant EOR acquisitions announced within days of each other, underscoring the pace of consolidation.

Payoneer acquires Boundless (January 20, 2026)

Payoneer made its second EOR acquisition in 18 months, acquiring Dublin-based Boundless, an EOR platform supporting employment in 25+ countries. Boundless was founded in 2019 by Dee Coakley and Emily Castles and had raised €2.5 million in a 2021 seed round led by Ada Ventures and Fyrfly Venture Partners.

The acquisition gave Payoneer deeper European EOR capabilities to complement Skuad’s Asia-Pacific strength. Payoneer’s CEO John Caplan described it as part of building a “comprehensive financial stack” for international SMBs. The deal confirmed Payoneer’s strategy of acquiring rather than building its EOR capabilities, assembling a workforce management division through targeted M&A.

Remote acquires Atlas expense management (January 20, 2026)

On the same day as the Payoneer-Boundless deal, Remote announced the acquisition of Atlas, an AI-native expense management platform for global teams. Note: this is Atlas the expense management company, not Atlas HXM the EOR provider. Atlas offered the Atlas Card (a global employee expense card), AI-powered expense tracking, and health benefits management for distributed teams.

This acquisition expanded Remote’s product beyond employment and payroll into financial operations for distributed teams. It signalled Remote’s ambition to become a complete “global employment operating system” rather than just an EOR provider.

Cumulative Funding: The EOR Industry by the Numbers

|

Provider |

Total Funding |

Last Valuation |

Key Investors |

|

$980M+ |

$17.3B |

Andreessen Horowitz, Coatue, General Catalyst |

|

|

$700M+ |

$4.2B (reported) |

Blackstone, Leeds Equity, TCV |

|

|

~$500M |

Undisclosed |

General Atlantic, Eldridge |

|

|

$490M+ |

$3.0B |

Accel, SoftBank, General Catalyst |

|

|

$440M+ |

$3.7B (sale talks $3.5-4.5B) |

Insight Partners, Tiger Global, IVP |

|

|

Omnipresent |

~$120M |

Undisclosed (acquired by Deel) |

Kinnevik, Teles Ventures |

|

~$220M |

$1.0B |

Georgian, Tiger Global |

|

|

~$80M |

Undisclosed |

Sequoia India, Tiger Global |

|

|

~$39M |

Undisclosed |

QED Investors |

|

|

Boundless |

€2.5M |

Undisclosed (acquired by Payoneer) |

Ada Ventures, Fyrfly |

Total venture and growth capital invested in the EOR industry: over $3.5 billion.

The valuation gap in the EOR industry tells the consolidation story more clearly than any other metric. Deel’s $17.3 billion valuation is approximately 4-5x the next largest provider, and the distance between the top tier and everyone else continues to widen.

The Key Themes Driving EOR Consolidation

1. Fintech convergence

The most important trend in the EOR industry is the convergence with fintech. Payoneer’s acquisitions and Revolut’s entry demonstrate that EOR is increasingly viewed as a feature of cross-border financial infrastructure, not a standalone HR tech category. Companies that move money across borders (payments platforms, neobanks, payroll processors) are natural acquirers of EOR capabilities because EOR solves a problem their existing customers already have.

2. Winner-take-most dynamics

The EOR industry is exhibiting classic winner-take-most dynamics. Deel controls the largest market share with 25,000+ clients and $17.3B valuation. Remote is a clear second. The gap between the top two and everyone else is widening. Mid-tier providers that raised $50-200M in 2021 but did not achieve sustainable unit economics are now acquisition targets (Omnipresent) or entering sale discussions (Papaya Global, reportedly).

3. Platform bundling

Pure-play EOR is no longer sufficient for market leadership. The winning strategy is platform bundling: EOR + global payroll + HRIS + contractor management + IT equipment + immigration + expense management. Deel pioneered this approach, and Remote’s Atlas acquisition shows it is following the same playbook. Standalone EOR providers that do not bundle additional services face increasing margin pressure.

4. Owned entity vs partner model

The M&A activity reveals a clear market preference for owned-entity EOR models over partner-dependent ones. Providers with owned entities in key markets (Deel, Remote, Multiplier, Atlas HXM) are acquiring or outcompeting partner-dependent providers. This is because owned entities provide stronger compliance control, better margins, and more defensible competitive positions.

5. Regional consolidation

Not all consolidation is happening at the top. The Hightekers-Eos deal shows that regional EOR specialists are merging to create broader geographic coverage. This trend is likely to continue as smaller providers in specific regions combine to compete with global platforms.

What This Means for Companies Choosing an EOR

The consolidation wave has direct implications for companies currently using or evaluating EOR providers.

Provider stability matters more than ever. If your EOR provider is acquired, merged, or shuts down, there is real operational disruption: re-contracting employees, benefit gaps, payroll interruption, and compliance exposure during the transition. Before choosing a provider, assess their financial sustainability, not just their feature list. Providers with strong revenue, clear paths to profitability, or backing from financially stable parent companies (like Payoneer) carry less counterparty risk than those burning through venture capital without a clear path to sustainability.

The market is bifurcating. There are now effectively two tiers of EOR providers. The first tier (Deel, Remote, and potentially Revolut) has the scale, funding, and product breadth to dominate the global market. The second tier includes strong regional specialists, enterprise-focused providers (G-P, Atlas HXM, Safeguard Global), and niche players with specific country or industry depth. Mid-tier generalist EOR providers without clear differentiation face the highest risk of acquisition, decline, or irrelevance.

Switching costs are real. Moving between EOR providers involves re-contracting every employee, potential benefit disruption, new payroll registration, and compliance gaps during transition. The consolidation environment makes it more important than ever to choose your initial provider carefully, because the cost of switching later is higher than most companies expect.

💡 Employsome Insight: The biggest risk in the current EOR market is not choosing the wrong features. It is choosing a provider that does not survive the consolidation wave. Before signing with any EOR, ask yourself: does this company have the financial stability to exist in 3 years? If not, you may find yourself re-contracting your entire workforce mid-employment, which is exactly the disruption you hired an EOR to avoid.

What Comes Next: Five Predictions for the EOR Industry

The M&A wave of 2024-2026 is not the end of the story. It is the setup for a fundamentally different EOR industry. Here is what we believe is coming next.

1. AI replaces the service layer, not the entity layer

The most overhyped narrative in EOR right now is “AI will replace EOR providers.” It will not. What AI will replace is the human service layer that sits between the client and the compliance infrastructure. Contract generation, payroll calculations, compliance monitoring, onboarding workflows, and employee queries are all being automated at speed. Borderless AI has already built an agentic system (HRGPT) that generates compliant employment contracts in seconds and processes payroll across 170+ countries in approximately 20 minutes. Pebl launched its AI assistant Alfie across 50+ languages. Deel’s AI handles compliance alerts and document generation at scale.

But the legal entity, the actual registered company that employs the worker, pays the taxes, and holds the liability, cannot be replaced by AI. You still need a real company in a real country with real regulatory registrations. The winners in the next phase will be providers that combine owned entities with AI-powered service delivery: maximum compliance control with minimum human overhead. Providers still relying on large manual operations teams will see their margins crushed.

2. Revolut forces a pricing reset across the industry

Revolut’s GlobalHire entry is not just another competitor. It is a pricing event. Revolut can afford to price EOR services at or below cost because it makes money from payments, FX, banking, and lending. Every EOR client is also a potential customer for Revolut’s broader financial services ecosystem. This is the same playbook that destroyed margins in consumer banking, travel insurance, and foreign exchange.

We expect EOR pricing to drop by 15-25% across the mid-market within 18 months of GlobalHire’s full launch. The providers most exposed are those charging $500-700/month per employee with no significant product differentiation beyond basic payroll and compliance. Deel and Remote have enough scale and product breadth to absorb the pressure. Smaller providers do not.

3. The “Big 3” becomes the “Big 2 + Fintech”

By end of 2027, we expect the EOR market to be dominated by three types of players. Deel as the clear market leader with the broadest product suite and largest client base. Remote as the compliance-first alternative with strong owned-entity coverage. And a fintech layer (Revolut, Payoneer, and potentially others) that bundles EOR into broader cross-border financial infrastructure. G-P, Pebl, and Papaya Global will either find defensible niches, be acquired, or fade. The mid-tier generalist EOR provider, the company with 50-100 countries, $400-700/month pricing, and no unique differentiation, effectively ceases to exist as a viable independent business.

The exception is regional and country-level specialists with genuine local depth. Providers with physical offices, local HR teams, and deep in-country compliance expertise in specific markets will survive and potentially thrive because they offer something the global platforms cannot: hands-on advisory for complex employment situations, real escalation capacity for terminations and disputes, and relationships with local authorities that matter when things go wrong. The global platforms will increasingly rely on these specialists as in-country partners even as they compete with them for clients.

4. Governments start regulating EOR directly

The EOR model currently operates in a legal grey zone in many countries. It is not explicitly authorised by most employment law frameworks; it simply is not explicitly prohibited. That is changing. Germany already requires EOR providers to hold an AUG (employee leasing) licence. Singapore restricts EOR providers from sponsoring work passes. Several EU countries are examining whether EOR arrangements constitute disguised employee leasing.

We expect at least 3-5 major jurisdictions to introduce EOR-specific regulation by 2028, clarifying when EOR is permitted, what obligations the EOR must fulfil, and what rights the employed worker has. This will benefit providers with owned entities and transparent operating structures. It will hurt providers using opaque partner chains where compliance accountability is unclear.

5. EOR becomes invisible infrastructure

The ultimate trajectory of EOR is to become invisible. Just as payment processing became invisible (you do not think about Stripe when you buy something online), EOR will become embedded infrastructure that companies use without thinking about it. You will not “choose an EOR provider.” You will use a platform that happens to include compliant global employment as one feature among many: payments, banking, payroll, HR, IT, expense management, and benefits, all in one.

Deel is already building this. Remote’s Atlas acquisition moves in this direction. Revolut’s GlobalHire is designed this way from scratch. The standalone “EOR company” that does nothing but employ people in other countries is a transitional business model. The end state is integrated global workforce infrastructure where EOR is one component, not the whole product.

💡 Employsome Insight: If you are evaluating EOR providers today, the most important question is not “which provider has the best features right now?” It is “which provider will still be here, and still be relevant, in three years?” The industry is moving toward a world where 2-3 platforms dominate global EOR alongside a network of regional specialists. Choose accordingly. Pick a provider that is either clearly in the top tier or clearly the best in your specific country. Anything in between is a bet on a company that may not survive the consolidation.

Frequently Asked Questions

Over $3.5 billion in total venture and growth capital has been invested across the major EOR providers since 2019. Deel alone accounts for nearly $1 billion.

Deel at $17.3 billion, based on its most recent funding round. This is approximately 4-5x the valuation of the next largest provider.

By reported deal value, Payoneer’s acquisition of Skuad for $61 million in August 2024. However, Deel’s acquisition of Omnipresent (October 2025) was likely larger in terms of the acquired company’s previous fundraising ($120M+), though deal terms were not publicly disclosed.

Yes. The global EOR market is valued at approximately $5 billion in 2026 and is projected to grow at 6.5-9.5% CAGR depending on the source, reaching $8-20 billion by the mid-2030s. For detailed projections, see our EOR market size report.

Revolut’s entry is the most significant new market entrant in EOR history, given its $75B valuation, 65M customers, and existing global financial infrastructure. It is most likely to impact smaller EOR providers through aggressive pricing and cross-selling to its existing customer base. Deel and Remote have sufficient scale and product depth to compete. For our full analysis, see the Revolut GlobalHire deep dive.

Potentially. Acquisitions can lead to service changes, price increases, platform migrations, or changes in local execution quality. However, acquisitions by well-capitalised acquirers (like Payoneer) can also strengthen a provider’s financial stability and product offering. The key is to monitor communication from your provider and have contingency plans.

Written by

Courtney Pocock is a Copywriter & EOR/PEO Researcher at Employsome with 15+ years of experience writing for the HR, corporate, and financial sectors. She has a strong interest in global business expansion and Employer of Record / PEO topics, focusing on news that matters to business owners and decision-makers. Courtney covers industry updates, regulatory changes, and practical guides to help leaders navigate international hiring with confidence.

Our content is created for informational purposes only and is not intended to provide any legal, tax, accounting, or financial advice. Please obtain separate advice from industry-specific professionals who may better understand your business’s needs. Read our Editorial Guidelines for further information on how our content is created.

Other posts

Review other blog posts